Last Update 09 Apr 26

Fair value Increased 3.16%TIMA: Higher Revenue Outlook And Solid Margins Will Support Future Upside

Analysts have adjusted the ZEAL Network price target from €68.58 to €70.75, reflecting updated views on revenue growth assumptions, profit margins, and the P/E multiple applied to future earnings.

What's in the News

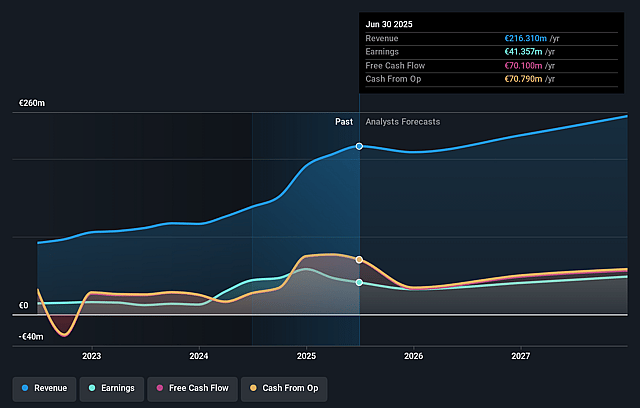

- ZEAL Network SE issued earnings guidance for fiscal year 2026, with expected revenues in the range of €250 million to €260 million (Key Developments).

Valuation Changes

- Fair Value: updated from €68.58 to €70.75, representing a modest uplift in the estimated worth per share.

- Discount Rate: adjusted slightly from 6.44% to 6.54%, indicating a marginally higher required return in the model.

- Revenue Growth: revised from 8.95% to 12.78%, indicating higher projected top line expansion in future forecasts.

- Net Profit Margin: moved slightly from 19.14% to 18.92%, indicating a small reduction in expected profitability on each € of revenue.

- Future P/E: kept broadly stable, shifting only marginally from 30.16x to 30.13x in the earnings multiple applied.

Key Takeaways

- Expansion of proprietary products and successful online migration are driving user growth, product differentiation, and increased market share.

- Investments in technology and targeted marketing enhance operational efficiency and margins, while strategic focus and new initiatives support sustainable long-term profitability.

- Reliance on jackpot-driven growth, high marketing costs, regulatory risks, and limited cross-selling restrict revenue stability, margin expansion, and diversification potential for ZEAL Network.

Catalysts

About ZEAL Network- Engages in the online lottery brokerage business in Germany.

- The continued expansion and success of ZEAL's proprietary product verticals, such as Traumhausverlosung and the rapidly growing Games segment (up 49% YoY), demonstrate strong product differentiation and new user acquisition potential, driving revenue growth and higher customer lifetime value.

- Sustained migration of lottery and gaming activity from offline to online channels, as evidenced by a record 1.5 million active monthly users and resilience even in a weak jackpot environment, positions ZEAL to further expand its addressable market, supporting long-term revenue and market share gains.

- Investment in technology, automation, and targeted marketing initiatives (including performance and brand marketing for Traumhausverlosung) is enabling operational efficiencies and more effective customer segmentation, with early signs of improving margin (lottery gross margin above 17% and steady CPLs), thus supporting future net margin and EBITDA expansion.

- ZEAL's ability to retain and grow its user base even during periods with fewer high-value jackpots, combined with ongoing improvements in product-market mix and pricing, suggests that the business is becoming structurally less dependent on jackpot volatility, de-risking earnings and supporting long-term profitability.

- Management's reaffirmation of full-year guidance, ongoing exploration of further investment opportunities, and strategic focus on scaling new business areas indicate clear visibility into future growth initiatives likely to have a positive impact on revenue and earnings trajectory.

ZEAL Network Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming ZEAL Network's revenue will grow by 12.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 19.0% today to 18.9% in 3 years time.

- Analysts expect earnings to reach €59.6 million (and earnings per share of €2.83) by about April 2029, up from €41.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 30.3x on those 2029 earnings, up from 24.7x today. This future PE is greater than the current PE for the GB Hospitality industry at 24.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.54%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- ZEAL Network's continued dependence on jackpot-driven customer acquisition creates revenue cyclicality and volatility, meaning periods with fewer or smaller jackpots could depress new customer growth and transactional activity, leading to unpredictable or declining revenues and EBITDA in the long run.

- Heavy marketing investment and rising customer acquisition costs-particularly highlighted by the higher cost per lead (CPL) for Traumhausverlosung versus the core lottery business-may suppress net margins, especially if efficiency gains from scaling new products or improving marketing effectiveness do not materialize.

- Concentration risk in the core German lottery brokerage business exposes ZEAL to adverse regulatory, tax, or competitive changes in its primary market; any unfavorable developments could have an outsized negative impact on revenue and earnings.

- Regulatory and licensing constraints in cross-selling and gaming remain a structural challenge: current restrictions prevent ZEAL from marketing Games to its established lottery customer base, limiting upselling potential, slowing growth of new verticals, and potentially capping revenue diversification and scalability.

- As ZEAL scales new offerings like Traumhausverlosung and Games, there is ongoing risk that sustained higher acquisition costs, slower-than-expected margin improvement, or inability to increase average revenue per user in these new segments will erode overall profitability and impact long-term net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €70.75 for ZEAL Network based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €80.0, and the most bearish reporting a price target of just €63.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €315.2 million, earnings will come to €59.6 million, and it would be trading on a PE ratio of 30.3x, assuming you use a discount rate of 6.5%.

- Given the current share price of €48.9, the analyst price target of €70.75 is 30.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on ZEAL Network?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.