Last Update 05 Jun 26

IDIA: Pediatric Sleep And Vaccine Pipeline Will Support Future Upside Despite Higher Costs

Analysts have lowered their price target on Idorsia to CHF 5, down from CHF 6. They cite reduced forward visibility and higher operating expenses as the main reasons for this adjustment.

What's in the News

- Idorsia reported positive Phase 1 results for its C. difficile vaccine candidate IDOR-1134-2831, showing a favorable safety profile and a dose dependent immune response against both bacteria and spores, according to company announcements dated 1 June 2026.

- The company shared new analyses from the Phase 3 PRECISION study indicating that aprocitentan, already approved in the US and Europe for systemic and resistant hypertension, is associated with sustained reductions in albuminuria and shifts to lower albuminuria risk categories in patients with uncontrolled or resistant hypertension, presented at the 35th Congress of the European Society of Hypertension on 1 June 2026.

- Idorsia announced positive top line Phase 2 results for daridorexant in pediatric insomnia, reporting a statistically significant, dose dependent improvement in total sleep time and additional sleep parameters, with a safety profile similar to placebo even at the 50 mg dose, as per the company’s product related update.

- The company provided full year 2026 guidance for QUVIVIQ, indicating expected sales of CHF 200 million.

- Idorsia disclosed a CEO transition, with Dr. Srishti Gupta stepping down and Chairman Jean Paul Clozel taking on day to day operational responsibilities as interim CEO while the Board searches for a successor.

Valuation Changes

- Fair Value: CHF 4.5 is unchanged, with no adjustment to the underlying estimate.

- Discount Rate: has fallen significantly from 6.56% to 3.94%, pointing to a lower required return in the model.

- Revenue Growth: has risen significantly from 21.57% to 42.00%, indicating higher assumed top line expansion in CHF terms.

- Net Profit Margin: has risen from 15.08% to 21.53%, reflecting higher expected profitability on future CHF earnings.

- Future P/E: has fallen significantly from 28.0x to 11.64x, implying a lower valuation multiple applied to projected earnings.

Key Takeaways

- Market optimism for rapid revenue growth may be premature, with unvalidated access, uncertain drug uptake, and regulatory outcomes adding risk to earnings expectations.

- Longer-term valuation appears inflated by pipeline commercialization hopes, while rising costs and increasing pricing scrutiny threaten future margins and profitability.

- Expanding global market access, product launches, and strategic partnerships are set to drive sustained growth, improved profitability, and reduced financial risk for Idorsia.

Catalysts

About Idorsia- A biopharmaceutical company, engages in the discovery, development, and commercialization of drugs for unmet medical needs in Switzerland, the United States, Japan, Europe, and Canada.

- The prospect of QUVIVIQ achieving widespread public reimbursement and rapid market uptake in Europe, combined with ongoing expansion to China, Latin America, and MENA, may be encouraging expectations of continued steep sales growth, leading investors to price in accelerating top-line revenue before access or demand is fully validated.

- Anticipation around the potential U.S. descheduling of the DORA class is driving enthusiasm that QUVIVIQ's U.S. prescriptions and gross margins will significantly increase; however, this outcome, its timing, and the extent of benefit remain uncertain, which injects risk around near-term and medium-term earnings.

- The assumption that the new drug TRYVIO will quickly capture a large share of the resistant hypertension market-based on recent approval, label updates, and payer receptiveness-could be leading the market to overestimate addressable revenue growth before partnership, real-world uptake, or payer access are proven.

- Optimism regarding the accelerated advancement and eventual commercialization of a broad pipeline (including Fabry disease, chemokine antagonists, and the C. diff vaccine) may be inflating valuation through expectations of long-term multi-asset revenue streams, even though increased cost controls and funding needs persist until 2027 profitability.

- Expectations that growing healthcare spending and rising chronic disease prevalence will provide "automatic" tailwinds for prescription volumes and pricing power may be overstated, especially in the context of intensifying global scrutiny over drug pricing and tightening payer controls, potentially squeezing future net margins and overall earnings.

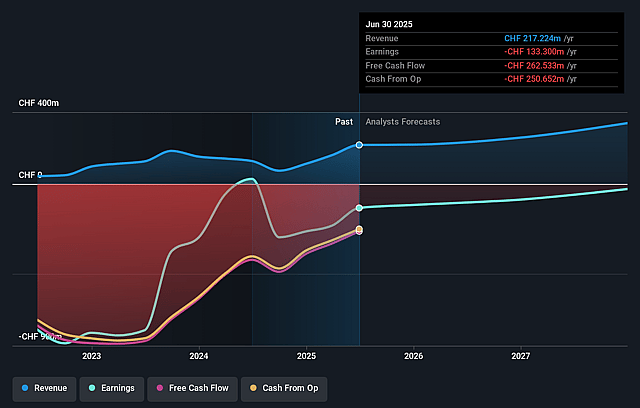

Idorsia Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Idorsia's revenue will grow by 42.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -100.6% today to 21.5% in 3 years time.

- Analysts expect earnings to reach CHF 135.0 million (and earnings per share of CHF 0.69) by about June 2029, up from -CHF 220.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting CHF453.6 million in earnings, and the most bearish expecting CHF-24.3 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 11.6x on those 2029 earnings, up from -5.1x today. This future PE is lower than the current PE for the GB Biotechs industry at 197.1x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 3.94%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Rapid commercial momentum and more than doubling of QUVIVIQ sales (CHF 23 million to CHF 56 million YoY), coupled with improved operating results and expanding global access (including imminent entry into China and ongoing reimbursement gains in Europe), could drive sustained top-line revenue growth and profitability.

- Multiple major upcoming catalysts-including the potential FDA descheduling of the DORA class in the U.S. (currently not included in company guidance), expansion into untapped international markets, and positive real-world and clinical data-could unlock significant upside in revenues and margins.

- Approval and launch readiness of TRYVIO (aprocitentan) in resistant hypertension, with broadened label and key differentiation in high-need populations (e.g., chronic kidney disease), positions Idorsia to capitalize on a >$12 billion market with strong payer and prescriber receptivity-potentially boosting future revenue and cash flow.

- Strategic partnerships and out-licensing deals (e.g., with Viatris, Simcere, and Menarini), as well as a robust pipeline (including Fabry disease, synthetic glycan vaccine, and multiple chemokine antagonists), provide diversified sources for new milestones, contract revenues, and reduced financial risk, supporting net margin improvement and earnings quality.

- The company's demonstrated operational turnaround-evidenced by extensive cost rationalization (CHF 50 million in savings YoY), extension of cash runway to end-2026, and a clear trajectory to commercial profitability (2026) and overall profitability (2027)-signals an improving financial profile and may attract investor interest, thereby supporting the share price.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CHF4.5 for Idorsia based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF5.0, and the most bearish reporting a price target of just CHF4.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CHF627.3 million, earnings will come to CHF135.0 million, and it would be trading on a PE ratio of 11.6x, assuming you use a discount rate of 3.9%.

- Given the current share price of CHF4.45, the analyst price target of CHF4.5 is 1.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Idorsia?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.