Last Update 08 Jul 26

Fair value Increased 17%ART: Dividend And Equity Raise Will Sustain Rich P/E With Limited Upside

Analysts have raised their price target for Arteche Lantegi Elkartea from €29.17 to €34.25, citing updated assumptions about revenue growth, profit margins, and a higher future P/E multiple.

What's in the News

- Arteche Lantegi Elkartea completed a follow on equity offering of €100.000032 million, issuing 3,030,304 common shares at €33 per share under Regulation S and Rule 144A. Source: Key Developments

- Certain shares of Arteche Lantegi Elkartea are subject to a lock up agreement from June 24, 2026 to September 22, 2026, covering a 90 day period during which the company and shareholders agreed not to issue or sell shares, with customary exceptions. Source: Key Developments

- Arteche Lantegi Elkartea announced an annual dividend of €0.3215 per share, payable on May 12, 2026, with an ex dividend date of May 8, 2026 and a record date of May 11, 2026. Source: Key Developments

Valuation Changes for Arteche Lantegi Elkartea

- Fair Value: increased from €29.17 to €34.25, indicating a higher assessed equity value per share in the updated assumptions.

- Discount Rate: decreased from 10.66% to 10.39%, reflecting a slightly lower required return used in the valuation model.

- Revenue Growth: raised from 12.78% to 14.31%, with higher projected € revenue growth embedded in the new assumptions.

- Net Profit Margin: adjusted from 12.09% to 11.68%, with a modestly lower expected € earnings margin on future revenue.

- Future P/E: increased from 25.12x to 29.12x, pointing to a higher valuation multiple applied to Arteche Lantegi Elkartea’s projected earnings.

Key Takeaways

- Lagging R&D investment and slow innovation could cause market share loss, reduced pricing power, and margin compression amid rapid industry digitalization.

- Rising supply chain, labor, and compliance costs from global risks and regulations threaten profitability and strain resources needed for growth.

- Strong secular demand, robust financial health, and ongoing innovation drive Arteche's resilient international growth, supporting sustained margin expansion and revenue gains, regardless of cyclical volatility.

Catalysts

About Arteche Lantegi Elkartea- Engages in the design, manufacture, integration, and supply of electrical equipment and solutions focusing on renewable energies and smart grids in Spain and internationally.

- There are increasing expectations that rapid global electrification and the integration of renewables will disproportionately benefit larger, more innovative competitors with advanced digital grid solutions-raising concerns that Arteche's R&D (at just 3.5% of revenue) may be insufficient to keep pace, potentially leading to future erosion of market share and stagnant revenue growth.

- The accelerated decentralization and digitalization of energy infrastructure is expected to require more cutting-edge digital products and software integration; if Arteche cannot innovate at the speed of these industry shifts, it risks losing pricing power and being relegated to commoditized segments, putting downward pressure on future net margins.

- Heightening trade tensions and potential tariff barriers-especially between the US, Mexico, and China-may increase Arteche's supply chain costs and disrupt sales in key regions, resulting in higher input costs and volatility that could compress margins and earnings.

- Global labor shortages in STEM and digital fields are expected to drive talent migration toward leading technology firms, creating structural hiring challenges for Arteche and possibly leading to elevated wage costs or operational inefficiencies that negatively impact net margins.

- The proliferation of stricter ESG regulations and reporting standards worldwide may drive up compliance and capex requirements for smaller and mid-sized industrial players like Arteche, leading to higher operating costs and diverting resources from growth, ultimately weighing on future profitability and capital allocation.

Arteche Lantegi Elkartea Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

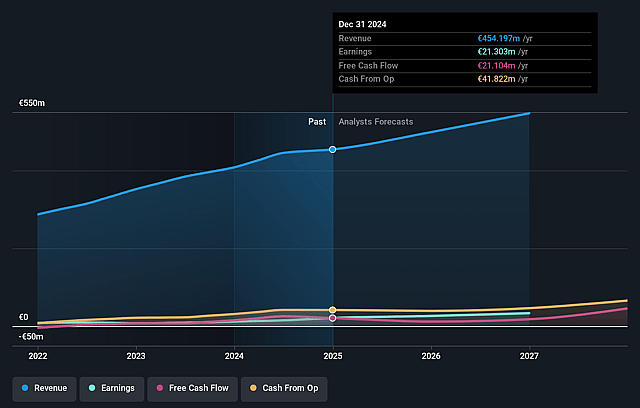

- Analysts are assuming Arteche Lantegi Elkartea's revenue will grow by 14.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.9% today to 11.7% in 3 years time.

- Analysts expect earnings to reach €90.2 million (and earnings per share of €1.56) by about July 2029, up from €45.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 29.2x on those 2029 earnings, down from 40.1x today. This future PE is lower than the current PE for the ES Electrical industry at 40.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.39%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Arteche continues to outpace its own strategic plan targets, with double-digit revenue, order intake, and profitability growth; combined with a robust order backlog and a 1.2 book-to-bill ratio, this indicates a healthy outlook for future revenues and suggests an underlying secular demand strength that could sustain or grow earnings.

- Sustained investment in R&D (over 3.5% of revenue) and consistent product innovation (notably in digital platforms, sustainable transformers, and grid reliability solutions) point to a long-term trend of expanding the company's capabilities and addressable markets, likely supporting future margin expansion and revenue growth.

- Arteche's aggressive international expansion and geographic diversification-especially growth in EMEA and Asia-Pacific, and capacity increases in China and Mexico-mitigate regional risks and currency volatility, enhancing revenue and earnings resilience to localized downturns.

- Strong cash generation, low leverage (0.5x EBITDA), and a free operating cash flow conversion rate of 78% afford Arteche the flexibility to pursue opportunistic inorganic growth (acquisitions) and capacity expansion, supporting topline growth, while improving capital efficiency and potential for earnings growth.

- Secular global trends in electrification, renewable energy integration, and grid modernization continue to drive high demand for Arteche's core solutions across utility, industrial, and infrastructure clients, suggesting robust tailwinds that could underpin continued revenue and margin improvement despite cyclical or political challenges.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €34.25 for Arteche Lantegi Elkartea based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €772.5 million, earnings will come to €90.2 million, and it would be trading on a PE ratio of 29.2x, assuming you use a discount rate of 10.4%.

- Given the current share price of €32.3, the analyst price target of €34.25 is 5.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Arteche Lantegi Elkartea?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.