Last Update 17 Jun 26

NYAX: EV Charging And AI Expansion Will Test Recurring Revenue Premium

Analysts have raised their price target on Nayax stock to ₪150.15, citing updated total addressable market work, ongoing share gains across unattended payment verticals and expectations for resilient recurring revenue streams.

Analyst Commentary

Recent Street research on Nayax stock centers on how well the company can keep expanding its footprint in unattended payments while translating that into profitable, recurring revenue growth. Analysts are updating their models and targets based on fresh total addressable market work, Q1 results and early contributions from newer areas like EV charging.

Bullish Takeaways

- Bullish analysts see Nayax gaining share across several unattended payment verticals, including vending, ticketing, EV, amusement, laundromats and parking. They view this as support for higher long term growth assumptions and valuation targets.

- Updated total addressable market analysis and higher price targets suggest confidence in Nayax’s ability to keep scaling its platform and recurring revenue base, rather than relying solely on one time hardware sales.

- Q1 results, where strong hardware sales offset weaker payment processing, are cited as evidence that Nayax can execute across multiple revenue levers. Bullish analysts argue this supports more constructive long term margin and cash generation views.

- Exposure to EV charging, including the Lynkwell acquisition, is framed as an additional growth vector. Some analysts point to oil price moves as a potential support for long term EV related transaction volumes and, by extension, Nayax’s processing and services opportunity.

Bearish Takeaways

- Bearish analysts, including those maintaining Neutral or Market Perform ratings, appear cautious about how much of the updated growth and margin outlook is already reflected in current Nayax valuation levels, despite higher price targets.

- The Q1 mix, where payment processing lagged while hardware was stronger, raises questions for more cautious analysts about how consistent processing growth and transaction related economics will be across cycles.

- Some analysts prefer to wait for a longer track record of execution in newer segments such as EV charging and for clearer evidence that acquisitions like Lynkwell can be integrated efficiently without pressuring profitability metrics.

- Macro volatility and currency assumptions are treated carefully by more conservative analysts, who see currency benefits and geographic diversification as supportive but not guaranteed inputs into Nayax’s medium term growth and valuation case.

What’s in the News for Nayax

- Nayax rolled out proprietary AI powered discovery and personalization tools for retailers, adding AI driven visual and text search, product recommendations and cross platform solutions to its retail platform, source: Nayax AI Rollout Tests Rich Valuation And Strong Share Price Momentum.

- The new AI engine is integrated into the Nayax platform and uses real time data and machine learning to enrich product catalogs with granular tags and attributes, aiming to help merchants increase customer lifetime value through more tailored discovery and purchasing journeys, source: company event disclosure.

- Nayax reaffirmed earnings guidance for the year ending December 31, 2026, with revenue expected in a range of $510 million to $520 million, and reiterated a mid term 2028 framework that includes revenue of $1.0b, source: company guidance update.

- The company called an AGM for April 29, 2026, where shareholders are being asked to approve amendments to the Articles of Association that would classify the Board of Directors, excluding external directors, into three classes with staggered three year terms, source: company corporate governance proposal.

Valuation Changes for Nayax Stock

- Fair Value: Estimated fair value remains unchanged at ₪150.15, indicating no shift in the core valuation output of the model.

- Discount Rate: The discount rate has risen slightly from 11.35% to 11.49%, reflecting a modestly higher required return in the updated analysis.

- Revenue Growth: The forecast revenue growth assumption is effectively unchanged at 22.99%, with only a minor rounding difference in the updated figure.

- Net Profit Margin: The assumed net profit margin stays broadly stable at 11.61%, with the updated model keeping the same profitability profile for Nayax.

- Future P/E: The future P/E multiple has fallen slightly from 30.42x to 29.42x, indicating a modestly lower valuation multiple applied to Nayax’s projected earnings.

Key Takeaways

- Diversification into high-growth sectors and international markets, along with deep OEM integration, is driving predictable, scalable, and higher-margin recurring revenues.

- Operational efficiencies and ecosystem lock-in are boosting profitability, supporting sustainable margin expansion and long-term earnings growth.

- Intensifying regulation, commoditization of digital payments, and high investment needs may constrain Nayax's revenue growth, profitability, and ability to expand its self-service device market.

Catalysts

About Nayax- A fintech company, develops a complete solution for automated self-service retailers, commerce, and other merchants in the United States, Europe, the United Kingdom, Australia, Israel, and rest of the world.

- Nayax's expansion into high-growth verticals like EV charging-with partnerships locking in OEM integrations and first-mover advantages-positions the company to capture outsized recurring SaaS and processing revenues in emerging markets where payment digitalization is rapidly accelerating, supporting both topline revenue and long-term gross margin expansion.

- The accelerating shift from cash to contactless payments globally is driving increased transaction volumes and recurring revenue growth-now representing 74% of revenue and expanding at >30% YoY-indicating continued predictable, higher-margin earnings as the broader adoption of digital payment infrastructure continues to play out.

- Strategic M&A and international expansion, particularly the integration of recent acquisitions and entry into underpenetrated regions like Brazil and Benelux, are providing operational leverage, scale, and synergies that boost both revenue growth rates and profitability, evidenced by annualized gross margin improvements and operating margin gains.

- Growth in ecosystem lock-in, driven by the embedding of Nayax's payment platforms inside OEM devices and diversification of value-added services (including SaaS, embedded banking, and business management), is likely to lift ARPU, reduce customer churn, and drive scalable operating leverage, supporting sustainable margin expansion and earnings growth.

- Ongoing operational optimization-such as renegotiated bank acquirer contracts, improved smart-routing, and supply chain efficiencies-is already driving higher processing and hardware margins, and continued efforts in this area should further boost net margins, free cash flow, and bottom-line earnings in future periods.

Nayax Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

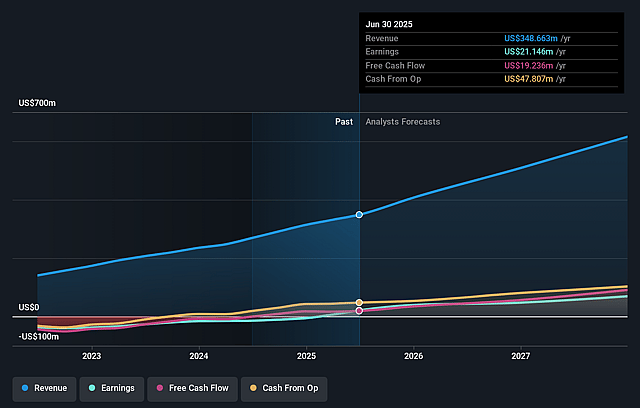

- Analysts are assuming Nayax's revenue will grow by 23.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.0% today to 11.6% in 3 years time.

- Analysts expect earnings to reach $92.1 million (and earnings per share of $1.75) by about June 2029, up from $29.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 30.0x on those 2029 earnings, down from 84.1x today. This future PE is greater than the current PE for the IL Electronic industry at 27.5x.

- Analysts expect the number of shares outstanding to grow by 1.2% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.49%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying privacy regulation and rising global data security scrutiny may reduce Nayax's ability to leverage customer transaction data across jurisdictions (such as in embedded banking or analytics-driven SaaS upsells), negatively impacting recurring revenue growth and cross-selling opportunities.

- The increasing commoditization of digital payments and broadening competition from large, well-capitalized payment and fintech providers-especially as Nayax moves into verticals like EV charging and retail-could pressure transaction margins, hardware and SaaS pricing, ultimately limiting future net margin expansion.

- Heavy reliance on continued R&D, acquisitions, and the buildout of new divisions (such as embedded banking) requires sustained, significant capital investment; missteps in integration or execution, or the need for further equity offerings, could erode earnings per share and impact both net income and free cash flow.

- The trend towards direct-to-consumer, mobile-first retail and declining growth in retrofitting of legacy vending may limit the expansion of Nayax's core unattended/self-service device market, risking slower device deployment growth and restraining total addressable market revenue expansion.

- Escalating regulatory and compliance costs-particularly for embedded financial products across multiple international markets-could disproportionately impact medium-sized players like Nayax, straining operational agility and putting further pressure on profitability and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₪150.15 for Nayax based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₪214.73, and the most bearish reporting a price target of just ₪85.56.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $793.0 million, earnings will come to $92.1 million, and it would be trading on a PE ratio of 30.0x, assuming you use a discount rate of 11.5%.

- Given the current share price of ₪195.0, the analyst price target of ₪150.15 is 29.9% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Nayax?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.