Last Update 10 Jul 26

Fair value Decreased 3.25%RNO: Diesel Ruling And Margin Guidance Will Support 2026 Earnings Visibility

Analysts have trimmed their fair value estimate for Renault to about €38.74 from roughly €40.04, reflecting recent price target cuts around €34 and more cautious assumptions on profit margin and discount rate, despite slightly higher revenue growth and future P/E inputs.

Analyst Commentary

Recent research on Renault offers a mixed picture, with valuation targets adjusted to around €34 and ratings that highlight both potential and execution risk. For you as an investor, the key takeaway is that analysts see room for the stock to perform in line with their refreshed assumptions, but they are also flagging several areas to watch closely.

Bullish Takeaways

- Bullish analysts see the current fair value estimate near €38.74 as still above some of the latest price targets around €34, which suggests they view the recent reassessment as a recalibration rather than a collapse in the investment case.

- The use of slightly higher revenue growth and future P/E inputs in fair value work indicates that some analysts still factor in the potential for Renault to support its valuation through future earnings power, provided execution holds up.

- Maintaining neutral ratings, rather than moving decisively to an Underperform stance, points to the view that Renault can justify its current pricing if it delivers on profitability and capital allocation plans.

- The relatively modest cut in target prices, instead of a more drastic reset, suggests that bullish analysts see the adjustments as fine tuning their models to reflect updated margin and risk assumptions.

Bearish Takeaways

- Bearish analysts cutting targets to around €34 and downgrading their stance highlight concern that previous expectations for Renault may have been too optimistic given current visibility on earnings quality and balance sheet risk.

- More cautious assumptions on profit margins imply that some analysts question the company’s ability to sustain prior profitability expectations, which in turn limits how much they are prepared to pay for the stock in their models.

- An increased focus on a higher discount rate signals that analysts are assigning more risk to Renault’s future cash flows, which directly weighs on valuation even when revenue assumptions are held or slightly uplifted.

- The downgrade referenced in recent research underscores worries around execution, suggesting that any slip in cost control, pricing, or investment discipline could make it harder for Renault to meet the earnings levels implied by previous targets.

What’s in the News for Renault

- The High Court of Justice in England & Wales ruled in favor of Renault Group in the “Prohibited Defeat Devices” diesel emissions litigation, rejecting all claims after extensive proceedings and a long trial, according to the company.

- Renault stated that it welcomes the High Court decision and reiterated its position that its vehicles comply with all regulatory requirements, which may ease some legal and reputational overhang for the company.

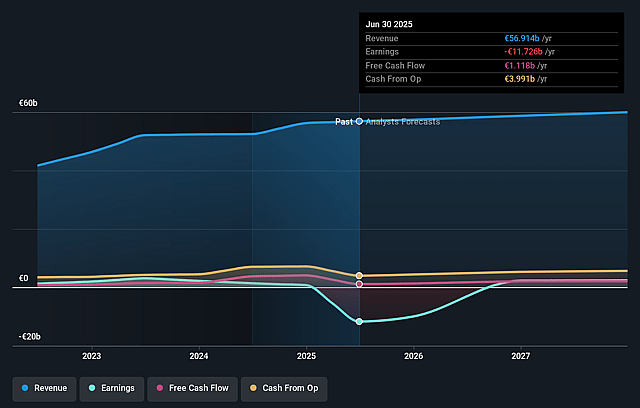

- Renault SA issued earnings guidance for the second half of the year, indicating that H2 operating margin is expected to be higher than H1, in line with its usual seasonal pattern. (Source: company guidance)

- The company also confirmed its guidance for 2026, targeting a group operating margin around 5.5% of group revenue. (Source: company guidance)

Valuation Changes for Renault

- Fair Value, trimmed from about €40.04 to roughly €38.74, a modest reduction of around 3%.

- Discount Rate, edged up from about 12.3% to roughly 12.48%, indicating a slightly higher required return in the updated model.

- Revenue Growth, adjusted from about 2.32% to roughly 2.64%, reflecting a small uplift in long term top line expectations in euro terms (€).

- Net Profit Margin, revised from about 3.46% to roughly 3.20%, a slight reduction that lowers projected earnings power on each euro (€) of revenue.

- Future P/E, moved from about 7.26x to roughly 7.57x, implying a modestly higher valuation multiple applied to Renault’s expected earnings.

Key Takeaways

- Strategic brand realignment and product innovation drive Renault's competitiveness in the EV and hybrid market, potentially boosting revenue and improving net margins.

- Operational efficiency, strategic partnerships, and model expansions aim to enhance market penetration and financial health through cost synergies and increased market reach.

- Renault faces revenue unpredictability from volatile markets, regulatory cost pressures on margins, and strategic risks from joint ventures and negative associate contributions.

Catalysts

About Renault- Engages in the design, manufacture, sale, repair, maintenance, and leasing of motor vehicles in Europe, Eurasia, Africa, the Middle East, the Asia Pacific, and the Americas.

- Renault is leveraging its brand realignment and product innovation to capture market share in the EV and hybrid market, with a focus on making these vehicles more affordable and appealing to consumers. This strategy is expected to boost revenue and potentially improve net margins through enhanced product mix.

- The significant reduction in development time and costs due to the Ampere initiative allows Renault to bring competitive EVs to market more rapidly. This operational efficiency should contribute positively to earnings by decreasing production costs while maintaining high product quality.

- Renault's strategic partnerships, such as those with Geely and Aramco, are designed to enhance scale and competitiveness, particularly in regions where Renault seeks greater market penetration. These alliances are expected to enhance earnings through cost synergies and expanded market reach.

- The introduction of new models, such as the Renault 5 and Twingo, and the expansion into segments like C-segment SUVs and smaller urban vehicles are positioned to tap into unmet consumer demand, which should drive revenue growth.

- Renault is positioning itself for operational agility in a volatile market, with plans for cost reductions and productivity enhancements, such as shrinking fixed costs in collaboration with partners. This will likely support net margins and bolster free cash flow, ensuring robust financial health.

Renault Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Renault's revenue will grow by 2.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from -18.9% today to 3.2% in 3 years time.

- Analysts expect earnings to reach €2.0 billion (and earnings per share of €7.3) by about July 2029, up from -€10.9 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 7.6x on those 2029 earnings, up from -0.6x today. This future PE is lower than the current PE for the GB Auto industry at 10.9x.

- Analysts expect the number of shares outstanding to grow by 0.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.48%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Renault's reliance on volatile markets such as Argentina and Turkey, with negative currency impacts from the Argentinian peso and Turkish lira devaluations, could affect revenue unpredictably, impacting the company's financial results.

- The company's need to incentivize EV sales to meet the strict CAFE (Corporate Average Fuel Economy) regulations in 2025 may lead to lower profit margins due to potential price cuts, thereby impacting net margins.

- Renault's joint ventures and partnerships, especially the reliance on Geely for certain platforms, may expose it to strategic risks, including integration challenges and potential for disagreements, which could affect earnings.

- The necessity to meet stringent regulatory requirements like CAFE within a short timeline could lead to increased costs, affecting Renault's ability to maintain robust net margins.

- Negative contributions from associated companies, like Nissan, and impairments, such as those on Nissan shares, might continue to impact Renault's net earnings if this does not stabilize.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €38.73 for Renault based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €64.8, and the most bearish reporting a price target of just €28.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €62.6 billion, earnings will come to €2.0 billion, and it would be trading on a PE ratio of 7.6x, assuming you use a discount rate of 12.5%.

- Given the current share price of €25.81, the analyst price target of €38.73 is 33.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Renault?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.