Last Update 04 Jun 26

Fair value Decreased 6.14%ANTIN: Share Buyback And Cash Distributions Will Support Future Upside

Analysts have trimmed their price target for Antin Infrastructure Partners SAS from €12.63 to €11.85, citing updated assumptions around the discount rate, revenue growth, profit margins and future P/E expectations.

What's in the News

- Sapphire Gas Solutions entered into a partnership with Antin Infrastructure Partners SAS, with the deal intended to support development of on-site natural gas infrastructure for energy intensive sectors in the United States. Source: Key Developments

- Antin Infrastructure Partners SAS plans to start a share repurchase program on March 16, 2026, with authorization to buy back up to 10% of its share capital at a maximum outlay of €430.06 million and a purchase price of €24 per share, subject to the terms approved at the June 11, 2025 Annual General Meeting. Source: Key Developments

- The share buyback program is intended to support liquidity in the stock, fund equity compensation plans, provide shares for potential mergers or asset deals, and allow for possible share cancellations over an 18 month period from the date of the meeting. Source: Key Developments

- The Board of Directors proposed a total distribution of €127.2 million for 2025, or €0.71 per share, split between an interim payment of €0.36 per share made on November 14, 2025 and a second instalment of €0.35 per share planned for June 17, 2026, subject to shareholder approval. Source: Key Developments

- A Board meeting on March 11, 2026 included review of the consolidated financial statements for the 2025 financial year. Source: Key Developments

Valuation Changes

- Fair Value: trimmed from €12.63 to €11.85, a modest reduction in the modelled estimate.

- Discount Rate: inched up from 7.24% to 7.28%, reflecting slightly higher required return assumptions.

- Revenue Growth: adjusted from 18.37% to 17.18%, indicating a more cautious outlook for growth in the model.

- Net Profit Margin: moved from 47.41% to 44.20%, implying lower expected profitability on future earnings.

- Future P/E: raised from 12.05x to 12.52x, signalling a slightly higher multiple applied to projected earnings.

Key Takeaways

- Antin's strategic focus on electrification, decarbonization, and data growth aligns with long-term trends, enhancing infrastructure investment returns and revenue streams.

- Successful fundraising and expansion into North America and Asia Pacific boost capital deployment ability and create substantial growth opportunities for earnings and margins.

- High dividend payout may limit reinvestment, while fundraising misalignment and rising costs could pressure future earnings and margins amidst geopolitical and regulatory challenges.

Catalysts

About Antin Infrastructure Partners SAS- A private equity firm specializing in infrastructure investments.

- Antin Infrastructure Partners is well-positioned to leverage supportive secular trends such as electrification, decarbonization, and the exponential growth of data, which are expected to drive long-term growth in its infrastructure investments, potentially leading to increased revenue streams.

- With successful fundraising efforts for Flagship Fund V, now the largest infrastructure fund closed globally in 2024, Antin's increasing ability to deploy capital effectively could enhance future earnings growth and profitability.

- The company is set to expand its investor base, notably within the North American and Asia Pacific markets, providing additional growth opportunities that could positively impact revenue and earnings.

- Antin's focus on performance improvement through AI and data science, alongside sustainability initiatives, positions its portfolio companies to capitalize on growth initiatives, potentially improving net margins and overall value creation.

- The imminent launch of Mid Cap Fund II and the potential acceleration of exit activity, including planned exits in 2025 and 2026, are expected to enhance carried interest revenue and augment their earnings trajectory.

Antin Infrastructure Partners SAS Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

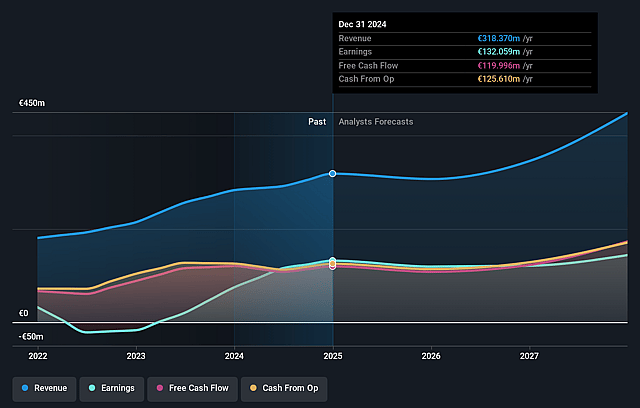

- Analysts are assuming Antin Infrastructure Partners SAS's revenue will grow by 17.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 36.6% today to 44.2% in 3 years time.

- Analysts expect earnings to reach €208.0 million (and earnings per share of €1.16) by about June 2029, up from €106.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 12.6x on those 2029 earnings, down from 15.7x today. This future PE is lower than the current PE for the FR Capital Markets industry at 13.8x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.28%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Despite strong financial performance, the plan to maintain the dividend at €0.71 per share and the high payout ratio of 93% might limit reinvestment opportunities, potentially affecting future earnings growth.

- With several funds near full deployment but next fundraising cycles planned for 2026, there could be a temporary misalignment between investments and fundraising, which might impact revenue.

- Prolonged holding periods due to uncertain market conditions can delay exits, affecting the realization of carried interest expected from funds like Fund III-B, thus impacting earnings projections.

- Rising operating expenses, including compensation increases and the hiring of senior personnel, may pressure net margins if not offset by proportional revenue growth.

- The geopolitical environment and potential regulatory changes, especially in renewables and U.S. investments, can introduce valuation uncertainties, impacting fund performance and subsequent exit strategies.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €11.85 for Antin Infrastructure Partners SAS based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €14.6, and the most bearish reporting a price target of just €8.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €470.6 million, earnings will come to €208.0 million, and it would be trading on a PE ratio of 12.6x, assuming you use a discount rate of 7.3%.

- Given the current share price of €9.42, the analyst price target of €11.85 is 20.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Antin Infrastructure Partners?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.