Last Update17 Oct 25Fair value Decreased 2.81%

Analysts have trimmed their average price target for Santos from A$8.10 to A$7.88. This reflects more cautious assumptions on revenue growth and profit margins. However, many continue to see upside potential given the recent withdrawal of the XRG takeover proposal and the company’s promising project pipeline.

Analyst Commentary

Market experts have weighed in on Santos following recent developments, with their commentary reflecting a mix of optimism and caution regarding the company's outlook.

Bullish Takeaways- Bullish analysts highlight renewed upside potential in Santos shares after the withdrawal of the XRG consortium's takeover offer. They see the company as well-positioned for organic growth.

- Successful progress in major projects such as Barossa and Pikka is expected to unlock significant free cash flow over the next five years, supporting future value creation.

- Current valuations are perceived as attractive in light of Santos' promising development pipeline and improved capital discipline.

- Some price targets have been set above the current trading levels. This indicates scope for potential share price appreciation as operational goals are met.

- Bearish analysts remain cautious on forecasts for revenue growth and profit margins, tempering expectations for near-term financial performance.

- Project execution risks remain a key concern. Timelines and cost controls are being closely scrutinized in the current environment.

- There is ongoing uncertainty surrounding the broader macroeconomic backdrop, which could impact demand for Santos’ products and weigh on overall sector multiples.

- With the removal of the takeover premium, Santos must now deliver on its operational promises to justify further gains in its share price.

What's in the News

- The proposed AUD 28.8 billion acquisition of Santos Limited by the XRG Consortium, Abu Dhabi Developmental Holding Company PJSC, and The Carlyle Group Inc. has been cancelled following an extended period of due diligence and negotiations. (Key Developments)

- Santos Limited announced an ordinary fully franked dividend of USD 0.1340 per security for the six months ended June 30, 2025. Record Date is September 3, 2025; Payment Date is October 1, 2025. (Key Developments)

Valuation Changes

- Consensus analyst price target has fallen moderately from A$8.10 to A$7.88, suggesting a slightly more cautious outlook on future share value.

- The discount rate has risen slightly from 6.96% to 7.00%, reflecting a modest increase in perceived risk or required return.

- Revenue growth expectations have decreased from 10.05% to 9.68%, indicating tempered forecasts for future expansion.

- Net profit margin projections have edged down from 23.32% to 23.03%, showing minor adjustments to profitability assumptions.

- Future P/E ratio estimates have declined from 12.98x to 12.68x, pointing to somewhat lower expected earnings multiples.

Key Takeaways

- Accelerated production growth and strong long-term LNG contracts position Santos for stable revenue, improved margins, and earnings resilience amid rising energy demand.

- Advancements in carbon capture and efficiency drive ESG improvements and cost reductions, unlocking new revenue streams and boosting free cash flow potential.

- Exposure to commodity cycles, regulatory and environmental risks, and rising ESG pressures threaten earnings stability, growth prospects, and access to capital for Santos.

Catalysts

About Santos- Explores, develops, produces, transports, and markets hydrocarbons in Australia and Papua New Guinea.

- Near-term production growth is set to accelerate with the imminent ramp-up of major projects (Barossa LNG and Pikka Phase 1), positioning Santos to benefit from structurally rising global LNG and natural gas demand, especially in emerging Asia; this should boost future revenue and operating margins.

- Strong momentum in securing long-term, oil-linked LNG contracts-92% of portfolio contracted and 80% oil-linked through 2029-enhances revenue visibility and pricing power amid ongoing geopolitical-driven energy security concerns, supporting stable and growing earnings.

- Santos' rapid progress and delivery in carbon capture and storage (CCS), highlighted by the Moomba CCS project already storing over 1 million tonnes of CO2e, positions the company to leverage the global transition to lower-carbon energy; this not only helps reduce emissions intensity and improve ESG credentials, but may also unlock new premium revenue streams and support higher net margins.

- Company-wide focus on operational efficiency, project self-execution, and continued cost reductions (targeting sub-$7/boe unit costs) is likely to improve free cash flow generation and net margins as new projects come online and CapEx cycles moderate.

- A robust pipeline of backfill, infill, and expansion projects (across PNG, Alaska, Beetaloo, and Western Australia) integrated with existing infrastructure increases long-term growth optionality and underpins sustained production and revenue expansion, supporting higher long-term earnings resilience.

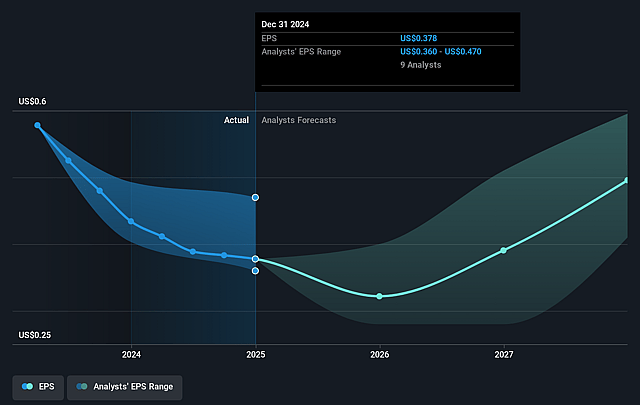

Santos Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Santos's revenue will grow by 9.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 19.6% today to 23.2% in 3 years time.

- Analysts expect earnings to reach $1.6 billion (and earnings per share of $0.51) by about September 2028, up from $1.0 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $1.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.7x on those 2028 earnings, down from 16.1x today. This future PE is lower than the current PE for the AU Oil and Gas industry at 14.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.97%, as per the Simply Wall St company report.

Santos Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Large capital expenditure requirements for major development projects like Barossa and Pikka increase exposure to commodity price cycles and project execution risk, which could negatively impact net margins and result in potential asset impairments.

- Decommissioning and remediation liabilities for retiring assets, such as those arising in mature fields and demonstrated by ongoing decommissioning campaigns, require substantial future provisioning and could place downward pressure on future earnings and free cash flow.

- Concentrated asset portfolio in politically and environmentally sensitive regions (such as Papua New Guinea and Northern Australia) exposes Santos to regulatory, operational, and environmental risks, potentially disrupting production and impacting revenue stability.

- Growing global decarbonization policies, accelerating renewables adoption, and stricter emissions targets may erode long-term demand for LNG and gas, creating structural headwinds for Santos' core business and putting pressure on both revenue and long-term earnings growth.

- Increasing scrutiny from investors and higher ESG-related expectations or requirements can raise the company's cost of capital and restrict access to funding or insurance for fossil fuel-related projects, limiting growth opportunities and putting strain on net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$8.511 for Santos based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$9.42, and the most bearish reporting a price target of just A$7.6.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $6.9 billion, earnings will come to $1.6 billion, and it would be trading on a PE ratio of 13.7x, assuming you use a discount rate of 7.0%.

- Given the current share price of A$7.83, the analyst price target of A$8.51 is 8.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.