Last Update 15 Jun 26

Fair value Increased 2.31%GLEN: Future Copper Expansion And Labor Challenges Will Shape Fair Execution Outlook

Glencore's revised analyst price target has edged higher, with recent moves from banks such as Deutsche Bank lifting targets from around £5.50 to £6.10 per share as analysts refresh their models on revenue growth, margins and P/E assumptions.

Analyst Commentary

Recent research on Glencore points to a cluster of upward revisions to price targets, with key moves coming from major banks such as JPMorgan and Deutsche Bank alongside upgrades and target lifts from other institutions. The tone of this research is generally constructive on valuation and execution, with some clear areas where analysts remain more cautious.

Bullish Takeaways

- Bullish analysts have lifted price targets into the 560 GBp to 610 GBp range, which indicates that they see the current valuation as leaving room for further upside if Glencore delivers on its plans.

- The upgrade at HSBC, together with higher targets from several banks, suggests growing confidence in Glencore's ability to execute on its operating and capital allocation priorities.

- Repeated target increases from global banks, including JPMorgan, point to a more supportive stance on Glencore's earnings and cash flow profile as analysts refresh their models.

- Target hikes across multiple firms indicate that Glencore is increasingly viewed as better positioned within its sector compared with earlier assessments, particularly on profitability and balance sheet strength as reflected in valuation work.

Bearish Takeaways

- JPMorgan maintains a Neutral rating despite raising its price target to 560 GBp, which shows that some analysts still see a balance between upside potential and execution or macro risks.

- The presence of at least one Neutral stance alongside Buy ratings points to ongoing questions around how Glencore will deliver against earnings expectations embedded in these refreshed targets.

- Higher targets, while supportive, can also indicate that a portion of the improvement that bullish analysts expect is already reflected in current valuation. This may limit the margin of safety for more cautious investors.

- The spread between more optimistic targets, such as 610 GBp, and more moderate views like 560 GBp highlights that there is no single consensus on Glencore's growth and margin profile. Execution is therefore likely to remain under close scrutiny.

What's in the News

- Glencore shares have risen 110% over the past year, supported by robust copper and gold prices, a 7% full year revenue increase and stronger performance from the metals division, according to recent AGM disclosures and news reports.

- At its AGM, Glencore outlined copper production ambitions of more than 1,000,000 tons annually by 2026 and 1,600,000 tons by 2035, linked to demand from electrification, renewable energy and AI related uses. Source: AGM and recent news coverage.

- The company reported total shareholder returns of US$3.5b, including US$2b in direct payouts and US$1.8b in share buybacks, alongside a focus on safety, labor relations, mine closure planning and tailings dam risk. Source: AGM reporting.

- Operations at the Cerrejon coal mine in Colombia have been suspended after a community blockade disrupted shipments and fuel, with Glencore declaring force majeure and pausing most employment contracts while calling for dialogue. Source: Colombia coal industry news.

- Glencore has resumed emissions reduction projects at the Horne Smelter in Quebec following the passage of Bill 11, which extends the arsenic emissions compliance deadline to 2033 and provides regulatory clarity that supported the restart of nearly US$300m in environmental investments and copper operations there. Source: Canadian regulatory and company statements.

Valuation Changes

- The Fair Value, expressed in £ per share, has risen slightly from £6.08 to £6.22.

- The Discount Rate has edged up marginally from 9.38% to 9.39%.

- The Revenue Growth assumption has risen slightly from 3.19% to 3.28%.

- The Net Profit Margin expectation has moved modestly higher from 2.40% to 2.41%.

- The Future P/E multiple has increased slightly from 18.30x to 18.58x.

Key Takeaways

- Rising copper production, new projects, and disciplined supply management position Glencore for sustained revenue and earnings growth amid strong electrification and EV demand.

- Ongoing efficiency initiatives and portfolio optimizations enhance margins, bolster cash flow resilience, and provide capital flexibility despite inflationary and geopolitical pressures.

- Decarbonization, regulatory and legal risks, volatile marketing returns, and ESG pressures threaten Glencore's earnings stability, project execution, and access to capital.

Catalysts

About Glencore- Engages in the production, refinement, processing, storage, transport, and marketing of metals and minerals, and energy products in the Americas, Europe, Asia, Africa, and Oceania.

- A significant uplift in copper production volumes is expected in the second half of 2025 and beyond, as operational bottlenecks and mine sequencing normalize across key sites, with a clear pathway to 1 million tonnes of annual copper by 2028 and new low-capex, high-return brown/greenfield projects in Argentina (MARA, El Pachón) progressing-supporting sustained, long-term revenue and EBITDA growth in alignment with continued global electrification and EV adoption.

- Structural cost savings of ~$1 billion annually by 2026 are being delivered through over 300 efficiency and organizational optimization initiatives across Glencore's industrial portfolio, with more than half expected to be banked in H2 2025 and the remainder by 2026. This recurring benefit should materially improve net margins and operating leverage, offsetting inflationary pressures relative to peers.

- The upgraded marketing EBIT range (from $2.3–3.5bn, midpoint +16%) reflects robust performance in metals trading, particularly copper, and Glencore's ability to capitalize on persistent supply chain dislocations, trade realignments, and arbitrage opportunities amid tighter global supply and rising geopolitical focus on critical minerals-driving cash flow resilience and margin expansion over the cycle.

- Recent portfolio enhancements, including the integration of Tier 1, long-life, low-cost assets such as EVR and stakes in profitable industrials (e.g., Alunorte, Century), are poised to deliver incremental earnings and cash flows, with further monetization potential from Bunge shareholding and potential infrastructure asset sales, providing both downside protection and future capital return flexibility.

- The trend of disciplined supply management (e.g., targeted curtailments in coal, ferrochrome, and smelting) positions Glencore to benefit from shrinking capacity and slowing project development industry-wide-likely resulting in persistent supply deficits and structurally higher realized prices for battery and base metals, supporting long-term revenue growth and EBITDA uplift.

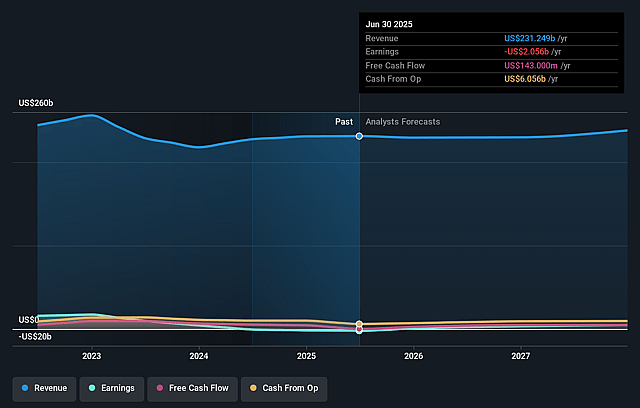

Glencore Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Glencore's revenue will grow by 3.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.1% today to 2.4% in 3 years time.

- Analysts expect earnings to reach $6.6 billion (and earnings per share of $0.57) by about June 2029, up from $363.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $8.9 billion in earnings, and the most bearish expecting $5.1 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 18.6x on those 2029 earnings, down from 252.6x today. This future PE is greater than the current PE for the GB Metals and Mining industry at 17.6x.

- Analysts expect the number of shares outstanding to decline by 1.57% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.39%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Weakness in first-half commodity prices, particularly for coal and copper, led to a significant decrease in industrial EBITDA; if this persists due to long-term global decarbonization or accelerated renewables adoption (limiting fossil fuel demand), Glencore's revenues and earnings from coal could structurally decline.

- Ongoing geopolitical and regulatory risks-including cobalt export bans in the DRC, uncertain Argentine regulatory frameworks for major copper projects (MARA, El Pachón), and potential global resource nationalism-could delay project execution, increase costs, or impede access to strategic minerals, ultimately impacting revenue growth and profit margins.

- Exposure to legacy coal operations and related carbon-intensive assets raises the risk of stranded assets, negative ESG sentiment, and shrinking access to ESG-linked capital as global investors increasingly shun fossil-fuel companies, potentially leading to higher cost of capital and reduced net margins.

- Marketing business returns have become more volatile and are increasingly reliant on short-term arbitrage opportunities driven by tariff uncertainty and market dislocations; if global trade becomes more stable, or commodity market regulations tighten further, structural profitability of the marketing business may become less predictable, pressuring Glencore's earnings and cash flow stability.

- Legal and remediation liabilities, particularly regarding historical corruption/bribery investigations and rising costs for environmental reclamation, mine closure, and water management, present material risks; future fines, tightening environmental standards, or new compliance mandates could create unpredictable headwinds for net earnings and increase operational expenditures.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £6.22 for Glencore based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £7.75, and the most bearish reporting a price target of just £4.62.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $272.7 billion, earnings will come to $6.6 billion, and it would be trading on a PE ratio of 18.6x, assuming you use a discount rate of 9.4%.

- Given the current share price of £5.83, the analyst price target of £6.22 is 6.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Glencore?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.