Last Update 01 Jun 26

Fair value Increased 2.82%GLEN: Fair Outlook Will Balance Tighter Earnings Execution With Recent Production And Labor Developments

Analysts have nudged Glencore's fair value estimate higher, with the updated model pointing to roughly a £0.17 per share uplift, helped by slightly stronger revenue growth and profit margin assumptions alongside a modestly higher future P/E, in line with recent Street target moves toward £5.60 to £6.10.

Analyst Commentary

Street research on Glencore has leaned toward higher price targets in recent months, with a mix of upgrades and trims that leave the stock trading against a fairly tight valuation range in the £4.60 to £6.10 per share bracket. For you as an investor, the key question is how much confidence to place in execution on earnings, cash generation and capital allocation relative to that range.

Bullish Takeaways

- Bullish analysts have moved price targets toward £5.60 to £6.10, which lines up with a view that Glencore can justify a higher multiple than previously used in their models.

- Several recent target lifts in 30 GBp to 60 GBp increments suggest increased comfort with the company’s ability to deliver on earnings assumptions and maintain margins built into Street forecasts.

- The presence of Buy ratings alongside the higher targets indicates that some analysts see risk or execution issues as manageable at current valuation levels, leaving room for upside if forecasts are met.

- Upgrades and target increases from large institutions, including JPMorgan, signal that key coverage now anchors around a mid £5s handle or higher, which can support confidence in the current fair value band used by many investors.

Bearish Takeaways

- Bearish analysts or more cautious desks have either kept Neutral ratings or trimmed targets, for example reducing a target from £5.20 to £4.60, which shows ongoing concern about execution or commodity cycle risk embedded in earnings assumptions.

- Where price targets have been cut slightly, such as moves from £6.10 to £6.00, it reflects a view that prior expectations may have been too optimistic, even if the stock is still seen as attractive on a Buy rating.

- The coexistence of Buy and Neutral ratings around similar price points highlights that conviction is not uniform, with some analysts preferring to wait for clearer evidence on profit delivery before assigning higher valuation multiples.

- For a cautious investor, the lower end of the target range around £4.60 is a reminder that if earnings or cash flow fall short of current assumptions, the stock could be judged fully valued more quickly than the bullish targets imply.

What's in the News

- Glencore and Taiwan's state refiner booked tankers to load oil, highlighting continued trading activity in the energy segment (Reuters).

- Workers at a Glencore Australian copper plant have threatened to strike after a pay dispute, with the union claiming staff are paid 15% less than nearby plants, and the refinery producing 300,000 tons of copper a year (Bloomberg).

- Glencore reported first quarter 2026 production results, including 199.6 kt copper, 5.8 kt cobalt, 176.9 kt zinc, 41.2 kt lead, 17.2 kt nickel, 68 koz gold, 4,869 koz silver, 830 kt chrome ore, 6.5 mt steelmaking coal, 22.9 mt energy coal and 13 kt ferrochrome.

- The company reaffirmed its 2026 production guidance, with expected output of 810 kt to 870 kt copper, 700 kt to 740 kt zinc, 70 kt to 80 kt nickel, 30 mt to 34 mt steelmaking coal and 95 mt to 100 mt energy coal.

- Glencore completed a share buyback tranche from July 7, 2025 to January 31, 2026, repurchasing 187,175,296 shares, equal to 1.57% of the company, for US$890m.

Valuation Changes

- Fair Value, revised to £6.08 from £5.91, has risen slightly and adds about £0.17 per share to the model output.

- Discount Rate, nudged up to 9.38% from 9.28%, now reflects a marginally higher required return on equity used in the valuation.

- Revenue Growth, now set at 3.19% from 3.07%, assumes a slightly higher long run dollar sales growth profile in the model.

- Net Profit Margin, adjusted to 2.40% from 2.36%, reflects a modestly higher expected dollar profitability on each unit of revenue.

- Future P/E, at 18.30x versus 18.30x previously, is effectively unchanged, so the fair value uplift is mainly driven by the revised growth and margin inputs rather than a higher multiple.

Key Takeaways

- Rising copper production, new projects, and disciplined supply management position Glencore for sustained revenue and earnings growth amid strong electrification and EV demand.

- Ongoing efficiency initiatives and portfolio optimizations enhance margins, bolster cash flow resilience, and provide capital flexibility despite inflationary and geopolitical pressures.

- Decarbonization, regulatory and legal risks, volatile marketing returns, and ESG pressures threaten Glencore's earnings stability, project execution, and access to capital.

Catalysts

About Glencore- Engages in the production, refinement, processing, storage, transport, and marketing of metals and minerals, and energy products in the Americas, Europe, Asia, Africa, and Oceania.

- A significant uplift in copper production volumes is expected in the second half of 2025 and beyond, as operational bottlenecks and mine sequencing normalize across key sites, with a clear pathway to 1 million tonnes of annual copper by 2028 and new low-capex, high-return brown/greenfield projects in Argentina (MARA, El Pachón) progressing-supporting sustained, long-term revenue and EBITDA growth in alignment with continued global electrification and EV adoption.

- Structural cost savings of ~$1 billion annually by 2026 are being delivered through over 300 efficiency and organizational optimization initiatives across Glencore's industrial portfolio, with more than half expected to be banked in H2 2025 and the remainder by 2026. This recurring benefit should materially improve net margins and operating leverage, offsetting inflationary pressures relative to peers.

- The upgraded marketing EBIT range (from $2.3–3.5bn, midpoint +16%) reflects robust performance in metals trading, particularly copper, and Glencore's ability to capitalize on persistent supply chain dislocations, trade realignments, and arbitrage opportunities amid tighter global supply and rising geopolitical focus on critical minerals-driving cash flow resilience and margin expansion over the cycle.

- Recent portfolio enhancements, including the integration of Tier 1, long-life, low-cost assets such as EVR and stakes in profitable industrials (e.g., Alunorte, Century), are poised to deliver incremental earnings and cash flows, with further monetization potential from Bunge shareholding and potential infrastructure asset sales, providing both downside protection and future capital return flexibility.

- The trend of disciplined supply management (e.g., targeted curtailments in coal, ferrochrome, and smelting) positions Glencore to benefit from shrinking capacity and slowing project development industry-wide-likely resulting in persistent supply deficits and structurally higher realized prices for battery and base metals, supporting long-term revenue growth and EBITDA uplift.

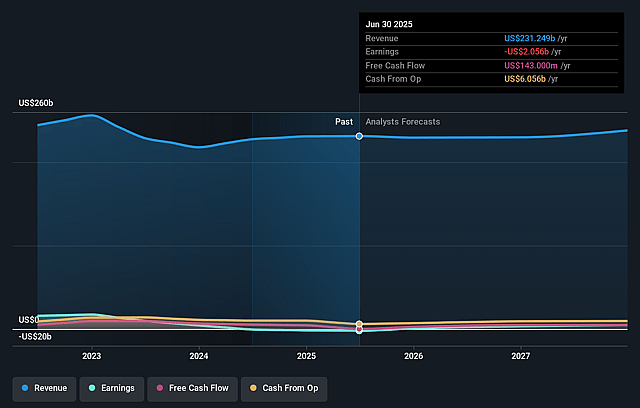

Glencore Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Glencore's revenue will grow by 3.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.1% today to 2.4% in 3 years time.

- Analysts expect earnings to reach $6.5 billion (and earnings per share of $0.57) by about June 2029, up from $363.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $8.8 billion in earnings, and the most bearish expecting $5.1 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 18.3x on those 2029 earnings, down from 246.8x today. This future PE is lower than the current PE for the GB Metals and Mining industry at 19.8x.

- Analysts expect the number of shares outstanding to decline by 1.57% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.38%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Weakness in first-half commodity prices, particularly for coal and copper, led to a significant decrease in industrial EBITDA; if this persists due to long-term global decarbonization or accelerated renewables adoption (limiting fossil fuel demand), Glencore's revenues and earnings from coal could structurally decline.

- Ongoing geopolitical and regulatory risks-including cobalt export bans in the DRC, uncertain Argentine regulatory frameworks for major copper projects (MARA, El Pachón), and potential global resource nationalism-could delay project execution, increase costs, or impede access to strategic minerals, ultimately impacting revenue growth and profit margins.

- Exposure to legacy coal operations and related carbon-intensive assets raises the risk of stranded assets, negative ESG sentiment, and shrinking access to ESG-linked capital as global investors increasingly shun fossil-fuel companies, potentially leading to higher cost of capital and reduced net margins.

- Marketing business returns have become more volatile and are increasingly reliant on short-term arbitrage opportunities driven by tariff uncertainty and market dislocations; if global trade becomes more stable, or commodity market regulations tighten further, structural profitability of the marketing business may become less predictable, pressuring Glencore's earnings and cash flow stability.

- Legal and remediation liabilities, particularly regarding historical corruption/bribery investigations and rising costs for environmental reclamation, mine closure, and water management, present material risks; future fines, tightening environmental standards, or new compliance mandates could create unpredictable headwinds for net earnings and increase operational expenditures.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £6.08 for Glencore based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £6.79, and the most bearish reporting a price target of just £4.59.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $272.0 billion, earnings will come to $6.5 billion, and it would be trading on a PE ratio of 18.3x, assuming you use a discount rate of 9.4%.

- Given the current share price of £5.68, the analyst price target of £6.08 is 6.6% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Glencore?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.