Last Update 05 Jun 26

Fair value Decreased 16%2858: Future Dividend And Margin Outlook Will Support A Higher Price

Analysts have trimmed their fair value estimate for Yixin Group from HK$3.64 to HK$3.07, citing updated assumptions around the discount rate, revenue growth, profit margins and the company’s future P/E.

What's in the News

- Shareholders approved a special dividend of HK$0.04 per share for the year ended December 31, 2025, at the Annual General Meeting held on April 23, 2026. (Source: Key Developments)

- PricewaterhouseCoopers was reappointed as auditor at the same April 23, 2026 Annual General Meeting, maintaining continuity in the company’s external audit oversight. (Source: Key Developments)

Valuation Changes

- Fair Value: Trimmed from HK$3.64 to HK$3.07, a moderate reduction in the estimated intrinsic value per share.

- Discount Rate: Adjusted slightly lower from 9.26% to 8.93%, reflecting a modest change in the required rate of return used in the model.

- CN¥ Revenue Growth: Tweaked marginally from 20.43% to 20.36%, indicating a very small change in projected top line growth assumptions.

- CN¥ Net Profit Margin: Raised from 11.94% to 12.80%, pointing to a modestly higher expected share of profit from each unit of revenue.

- Future P/E: Reduced from 14.96x to 11.54x, signaling a lower multiple being applied to the company’s expected earnings.

Key Takeaways

- AI-driven digital transformation and asset-light strategy are set to boost profitability, expand high-margin technology services, and diversify recurring revenue streams.

- Strong positioning in NEV and used car financing underpins revenue growth, with favorable industry fundamentals supporting market share gains and stable earnings.

- Rising credit risk, intensifying competition, regulatory pressures, partnership vulnerabilities, and shifting market trends threaten profitability, revenue growth, and core business sustainability.

Catalysts

About Yixin Group- Operates as an online automobile finance transaction platform in China.

- Rapid adoption of AI and digital risk management throughout all stages of financing and customer acquisition is expected to significantly increase approval efficiency, reduce fraud risk, and lower operating expenses, which should drive higher net margins and improved profitability over time.

- Sustained expansion in new energy vehicle (NEV) financing-with NEV transactions now making up over half of total financing volume-positions Yixin to capture secular growth from consumer shifts towards green mobility, thereby supporting continued revenue growth and increased platform income.

- Accelerated market share gains in the structurally underpenetrated used car finance segment, aided by AI-driven credit solutions and industry consolidation, create opportunities for higher-margin business and a broader, more stable customer base, positively impacting both revenue growth and net earnings.

- Strategic shift to a technology-driven and "asset-light" platform-by commercializing and exporting proprietary AI models and fintech solutions-promises new, recurring high-margin revenue streams from technology services, diversifying income mix and supporting margin expansion.

- Improving industry fundamentals, including rationalization and regulatory support against unhealthy competition, are leading to a more stable and efficient market structure that favors tech-enabled leaders like Yixin, enhancing visibility of earnings and reducing credit risks.

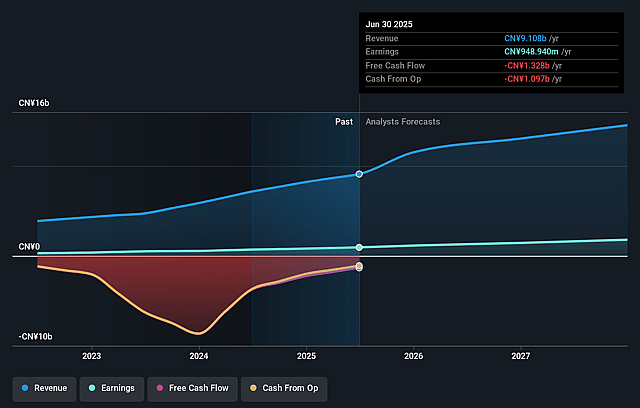

Yixin Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Yixin Group's revenue will grow by 20.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 13.2% today to 12.8% in 3 years time.

- Analysts expect earnings to reach CN¥2.0 billion (and earnings per share of CN¥0.29) by about June 2029, up from CN¥1.2 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 11.5x on those 2029 earnings, up from 6.8x today. This future PE is greater than the current PE for the HK Consumer Finance industry at 6.8x.

- Analysts expect the number of shares outstanding to grow by 0.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.93%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The rapid expansion into the used car financing market and increased exposure to long-tail customers heightens credit risk; rising delinquency and provisioning rates-especially if underwriting standards weaken or economic conditions deteriorate-could pressure net margins and overall profitability.

- Intensified industry competition, including from banks, fintechs, and automakers launching direct-to-consumer financing, may erode Yixin Group's market share and bargaining power, potentially limiting revenue growth and squeezing net margins.

- Ongoing and increasing regulatory oversight-especially anti-involution policies, credit risk controls, and evolving fintech/compliance standards in China and overseas-may increase compliance costs, restrict lending activities, and constrain sector-wide growth, negatively impacting both revenue and earnings.

- The company's business model heavily relies on partnerships with car dealers, OEMs, and financial institutions; any disruption or less favorable terms in these critical relationships could materially hinder loan origination volumes and revenue generation.

- Secular trends such as the shift toward shared mobility (e.g., ride-hailing, car-sharing) and stricter environmental regulations-especially those impacting gasoline and diesel vehicles-threaten to weaken the demand for individual car ownership and the used car market, undermining the company's core revenue drivers over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of HK$3.07 for Yixin Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of HK$3.76, and the most bearish reporting a price target of just HK$2.25.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CN¥15.9 billion, earnings will come to CN¥2.0 billion, and it would be trading on a PE ratio of 11.5x, assuming you use a discount rate of 8.9%.

- Given the current share price of HK$1.39, the analyst price target of HK$3.07 is 54.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Yixin Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.