Last Update 17 Jun 26

Fair value Increased 1.14%CTC.A: True North Plan And Buybacks Will Shape Balanced Share Returns

Canadian Tire Corporation's analyst fair value estimate has edged up to CA$193.18 from CA$191, with the change reflecting updated assumptions on discount rate, profit margin and future P/E, following a series of revised Street price targets ranging from CA$185 to CA$216 and a new CA$215 initiation tied to the company's "True North" plan.

Analyst Commentary

Recent Street research on Canadian Tire Corporation clusters around the "True North" plan and a tight band of valuation targets, giving you a clearer view of where analysts see room for upside and where they see execution risk.

Bullish Takeaways

- Bullish analysts point to the "True North" initiative as a key driver for earnings improvement and potential shareholder returns, which they reflect in targets at the upper end of the C$200s range.

- The C$215 initiation suggests confidence that Canadian Tire can execute on its transformation efforts well enough to support a premium relative to the updated fair value estimate.

- Positive ratings alongside these targets indicate that some analysts see the current share price as not fully reflecting the potential benefits of the plan.

- The maintenance of constructive ratings, even when targets are adjusted, signals that supportive analysts still view the long term story as intact.

Bearish Takeaways

- Bearish analysts, or those taking a more cautious stance, have trimmed price targets to C$185 and C$200 and paired these with Market Perform or Hold ratings. This highlights concern that execution on "True North" could be uneven.

- Lowered targets suggest that some expect more modest valuation support relative to prior expectations, with less room for Canadian Tire shares to move above current levels without clearer progress.

- The split between higher targets around C$215 to C$216 and more restrained figures near C$185 underlines uncertainty about how quickly the plan might translate into financial outcomes.

- Cautious ratings reinforce the view that, while Canadian Tire has identified key priorities, investors may want to watch evidence of delivery on cost, margin and growth goals before expecting a re rating.

What’s in the News for Canadian Tire Corporation

- Canadian Tire Corporation reported that from January 4, 2026 to March 10, 2026 it repurchased 335,000 shares, representing 0.63%, for C$60.1 million, completing a total repurchase of 3,062,209 shares, or 5.63%, for C$511.7 million under the buyback announced on March 7, 2025. (Source: Key Developments)

- A subsequent buyback tranche update for the period March 9, 2026 to April 4, 2026 showed no additional repurchases, with 0 shares bought for C$0 million, and the buyback program reported as completed. (Source: Key Developments)

- Canadian Tire Corporation launched the Hudson's Bay Stripes Summer '26 Collection, a 32 piece assortment that extends the Hudson's Bay Stripes design into outdoor living, beach and entertaining products, including items such as a pickleball set, a cedar strip canoe and Muskoka chairs, with availability across Canadian Tire stores, online at canadiantire.ca and selected Mark's locations and marks.com. (Source: Key Developments)

- Following the 2025 acquisition of select Hudson's Bay Company intellectual property, Canadian Tire Corporation highlighted the Hudson's Bay Stripes Summer '26 Collection as the first full seasonal assortment developed entirely by its teams, with several products made in Canada and curated to maintain the quality and style associated with the Stripes brand. (Source: Key Developments)

- Canadian Tire Corporation and WestJet introduced a partnership between Triangle Rewards and WestJet Rewards that allows members to link accounts and earn both Canadian Tire Money and WestJet points on eligible spending across participating Canadian Tire, SportChek, Mark's and WestJet channels, with the option to convert WestJet points into Canadian Tire Money. (Source: Key Developments)

Valuation Changes for Canadian Tire Corporation

- Fair Value: CA$193.18, up slightly from CA$191.00. This reflects a modest upward adjustment in the analyst model.

- Discount Rate: 10.69%, down slightly from 11.00%. This change increases the present value placed on Canadian Tire Corporation’s projected cash flows.

- Revenue Growth: 2.20%, marginally lower than the previous 2.23%. This indicates a small reduction in assumed top line expansion for Canadian Tire Corporation.

- Net Profit Margin: 5.11%, up from 4.83%. This represents a small improvement in expected profitability on each CA$ of revenue.

- Future P/E: 14.03x, reduced from 14.78x. This suggests a slightly lower valuation multiple applied to Canadian Tire Corporation’s projected earnings.

Key Takeaways

- Short-term sales gains may not be sustainable due to demographic shifts, changing consumer habits, and transitory growth drivers fading over time.

- Investments in digital and store improvements face challenges from rising costs, tough online competition, and potential margin pressures impacting long-term profitability.

- Enhanced customer loyalty, digital transformation, strong private brands, resilient core categories, and supply chain investments position the company for sustained growth and profitability.

Catalysts

About Canadian Tire Corporation- Provides a range of retail goods and services in Canada.

- Elevated investor optimism appears linked to recent strong discretionary sales and revenue growth, but this over-extrapolates consumer resilience; demographic headwinds like an aging population and shifting spending priorities are likely to dampen demand in home, automotive, and leisure categories, potentially limiting sustainable revenue expansion.

- There is an implicit bet that Canadian Tire's increased investments in digital, omnichannel infrastructure, and automation will quickly translate into competitive advantage, yet the ongoing catch-up spending compared to online-first retailers risks margin compression and leaves the company exposed to further market share loss, impacting long-term earnings growth and profitability.

- Strong short-term sales have benefited from patriotic purchasing, favorable weather, and post-pandemic replacement cycles-transitory drivers that may not persist, while the longer-term shift towards e-commerce and digital-first shopping habits may reduce the relevance of brick-and-mortar traffic and constrain future revenue growth.

- Ongoing investments in store refreshes, loyalty programs, and supply chain optimization are expected to drive cost efficiencies over time; however, the current and projected increase in fixed and variable costs, combined with wage and utility inflation, could pressure net margins and delay anticipated operating leverage improvements.

- Expectations for continued margin strength and market share gains may not sufficiently account for intensifying competition from global e-commerce giants and direct-to-consumer brands, nor for consumer shifts towards experiential spending over goods, raising the risk that revenue and net income projections are overly optimistic given secular industry changes.

Canadian Tire Corporation Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Canadian Tire Corporation's revenue will grow by 2.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.0% today to 5.1% in 3 years time.

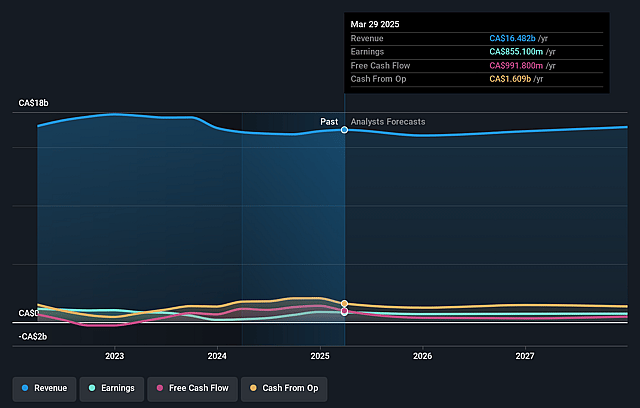

- Analysts expect earnings to reach CA$896.1 million (and earnings per share of CA$19.53) by about June 2029, up from CA$655.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.2x on those 2029 earnings, down from 14.9x today. This future PE is lower than the current PE for the CA Multiline Retail industry at 26.5x.

- Analysts expect the number of shares outstanding to decline by 2.69% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.69%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Strong customer loyalty, shown by a 6% increase in the active Triangle Rewards member base and expanded partnerships with RBC and WestJet, could drive higher repeat purchases, increase customer stickiness, and support long-term revenue stability and growth.

- Significant investments in digital infrastructure-including store automation, omnichannel enhancements (same-day delivery, one-click checkout), and the rollout of advanced data analytics/AI tools-are improving operational efficiency; over time, these are likely to drive higher sales and margin expansion as e-commerce sales are already outpacing overall growth.

- Ongoing strategic focus on private label and owned brands (with the HBC brand asset purchase and strong responses to new product launches) may result in higher gross margin and brand differentiation, supporting both top-line growth and improved profitability.

- The company's resilient and expanding core categories (home, automotive, seasonal, sporting goods) continue to benefit from Canadian trends in household formation, renewal cycles for big-ticket items, and robust discretionary spend-providing a buffer for long-term revenue and earnings even in periods of economic uncertainty.

- Ongoing supply chain investments-including a new large distribution center and increases in automation-are improving inventory velocity and cost leverage; combined with balance sheet deleveraging and active share repurchases, these efforts are positioned to drive improvements in net margin and overall shareholder returns in the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CA$193.18 for Canadian Tire Corporation based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$216.0, and the most bearish reporting a price target of just CA$165.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CA$17.5 billion, earnings will come to CA$896.1 million, and it would be trading on a PE ratio of 14.2x, assuming you use a discount rate of 10.7%.

- Given the current share price of CA$185.94, the analyst price target of CA$193.18 is 3.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Canadian Tire Corporation?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.