Last Update 15 May 26

Fair value Increased 1.25%UCB: Epilepsy Blockbusters And Neuroscience Pipeline Will Drive Future Upside Potential

Analysts have nudged their average price target for UCB higher, with fair value moving from €284.65 to about €288.21 as they factor in updated assumptions on discount rate, revenue growth, profit margins, and future P/E, supported by recent target hikes and fresh Outperform ratings on the stock.

Analyst Commentary

Recent research points to a split but constructive view on UCB, with several firms adjusting ratings and targets as they reassess the stock's risk and reward profile.

Bullish Takeaways

- Bullish analysts setting price targets around €304 and €340 are anchoring their views on higher assumed fair value, which feeds directly into the higher average target and supports the updated valuation range.

- The reference to "multiple blockbusters" in epilepsy signals confidence in UCB's product portfolio, which bullish analysts see as a key driver for revenue and earnings assumptions baked into their models.

- Outperform ratings indicate that some analysts expect UCB to execute well on its pipeline and commercial footprint, which they reflect through higher target P/E multiples or more generous margin assumptions.

- Coverage initiations with positive ratings suggest that UCB is gaining attention in broader sector work on neuroscience and biotech, which can support liquidity and interest in the stock over time.

Bearish Takeaways

- Bearish analysts have moved to more neutral stances such as Equal Weight with price targets around €260, implying that at current levels they see limited upside relative to their assessment of risk.

- The description of risk and reward as "balanced" highlights concerns that execution on the portfolio, including epilepsy assets, may already be well reflected in the share price.

- More cautious research flags the potential for earnings or margin outcomes to fall short of the optimistic scenarios that support higher targets, which could cap how much investors are willing to pay on a P/E basis.

- The mix of downgrades and higher targets suggests that some analysts view valuation as full against their base case assumptions, even if the underlying business profile remains solid.

What's in the News

- UCB plans to pay an annual dividend of €1.0150 per share on May 6, 2026, with an ex date of May 4, 2026, and a record date of May 5, 2026 (Key Developments).

- The Board of Directors authorized a share buyback plan on March 13, 2026, along with a separate repurchase program of up to 500,000 shares running to June 30, 2026, primarily to cover long term incentive plans (Key Developments).

- UCB is asking shareholders on April 30, 2026, to renew the Board's authority to increase share capital by up to 10% under specified conditions, with related changes to the Articles of Association (Key Developments).

- The company selected Gwinnett County, Georgia, for a new 460,000 square foot U.S. biologics manufacturing facility designed as a digital first site using AI, robotics and automation, with an estimated economic impact of about €5,000 million equivalent and around 330 permanent jobs once operational (Key Developments).

- Multiple product updates include new data for BIMZELX in hidradenitis suppurativa and plaque psoriasis, extensive neurology data at major U.S. medical meetings, positive topline results from the BE BOLD psoriatic arthritis trial, and additional studies in generalized myasthenia gravis, all highlighting ongoing clinical work across UCB's immunology and neurology franchises (Key Developments).

Valuation Changes

- Fair Value: The average fair value estimate edged up slightly from €284.65 to about €288.21 per share.

- Discount Rate: The discount rate used in models rose slightly from 6.27% to about 6.44%, which can modestly reduce present values for future cash flows.

- Revenue Growth: The long-term revenue growth assumption is broadly stable, moving from about 11.31% to around 11.29%.

- Net Profit Margin: The projected net profit margin eased slightly from about 26.75% to around 26.50%.

- Future P/E: The future P/E assumption increased from about 22.84x to roughly 23.48x, signalling a small uplift in the multiple analysts apply to expected earnings.

Key Takeaways

- Expansion into chronic and underserved conditions with innovative therapies and specialty biologics positions UCB for sustained growth and resilience against competitive pressures.

- Investments in manufacturing, digital R&D, and effective global market access enhance scalability, operational efficiency, and long-term margin expansion.

- Sustained pressures from pricing, patent expiries, changing reimbursement, R&D risks, and therapeutic alternatives threaten UCB's long-term growth, margins, and demand for core products.

Catalysts

About UCB- A biopharmaceutical company, develops products and solutions for people with neurology and immunology diseases worldwide.

- Strong demand drivers are in place due to the expansion of chronic disease prevalence in aging populations and increased global healthcare spending, especially in emerging markets; UCB's launch of BIMZELX and other late-stage therapies targeting underserved and chronic conditions positions the company to capture significant new revenue streams over the coming years.

- UCB's deep and advancing innovation pipeline, along with its focus on differentiated products in neurology and immunology, supports the ability to launch multiple new indications, address rare/orphan diseases, and leverage advances in personalized medicine, all of which underpin sustained long-term revenue growth and margin expansion.

- Effective global market access and rapid penetration-especially in the U.S., Europe, and Japan-with high conversion rates to paid scripts, broadening indications, and robust patient onboarding programs for key launches like BIMZELX are driving accelerating top-line growth and improved gross margin mix.

- Significant investments into manufacturing capacity (e.g., U.S. greenfield expansion) and digitalization of R&D are expected to support future scalability, operational efficiencies, and cost competitiveness, directly benefiting net margin and long-term earnings potential.

- Strategic focus on rare diseases and specialty biologics, where UCB already demonstrates strong expertise and growing market share, aligns with long-term industry trends toward higher pricing power and less competition, providing resilience against generic erosion and supporting durable high-margin revenue.

UCB Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

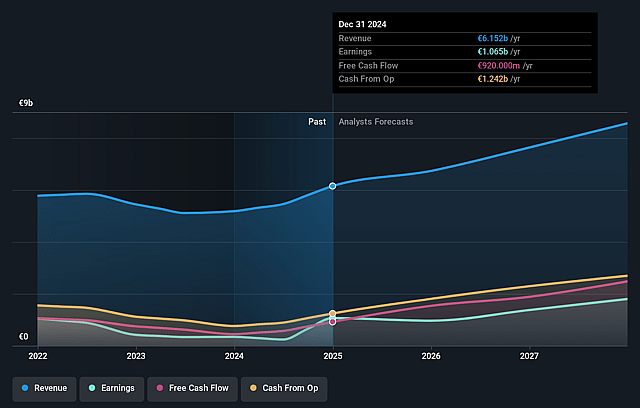

- Analysts are assuming UCB's revenue will grow by 11.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 20.1% today to 26.5% in 3 years time.

- Analysts expect earnings to reach €2.8 billion (and earnings per share of €15.07) by about May 2029, up from €1.6 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €3.7 billion in earnings, and the most bearish expecting €2.5 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 23.5x on those 2029 earnings, down from 29.0x today. This future PE is lower than the current PE for the GB Pharmaceuticals industry at 63.0x.

- Analysts expect the number of shares outstanding to grow by 0.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.44%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intense pricing pressure and increasing rebate rates in the U.S. market, especially for BIMZELX, are expected to continue as market access expands and payer negotiations intensify-this structural pricing erosion threatens UCB's long-term revenue growth and net margins.

- Patent expiries and biosimilar competition loom for key mature assets such as CIMZIA, as acknowledged with ongoing price erosion and normalization of U.S. buying patterns, putting significant pressure on both revenue and future earnings as exclusivity wanes.

- Rising global healthcare cost containment, payer scrutiny, and the potential implementation of U.S. tariffs could materially reduce reimbursement, increase supply chain costs, and create uncertainty around UCB's ability to sustain profitability, impacting both net margin and revenues over the long term.

- High R&D spending and pipeline concentration within neurology, immunology, and a few launch products (especially BIMZELX) increases vulnerability to late-stage clinical setbacks, regulatory hurdles, or competitive launches, risking volatility in R&D expenses and future earnings if approvals disappoint or therapeutic displacement occurs.

- Advancements in alternative modalities-such as efficacious oral therapies for chronic inflammatory diseases (e.g., Icotrokinra)-in combination with a general trend towards preventative medicine and digital health, may reduce long-term reliance on chronic biologic interventions and threaten sustained demand and revenue for UCB's cornerstone biologic products.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €288.21 for UCB based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €340.0, and the most bearish reporting a price target of just €195.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €10.7 billion, earnings will come to €2.8 billion, and it would be trading on a PE ratio of 23.5x, assuming you use a discount rate of 6.4%.

- Given the current share price of €237.0, the analyst price target of €288.21 is 17.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on UCB?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.