Last Update 09 Aug 26

Fair value Increased 2.06%5108: Raw Material Cost Pressures And Recent Rally Will Constrain Future Returns

Analysts have slightly raised their price target for Bridgestone to ¥3,650 from ¥3,600, citing a mix of potential profit support from steadier crude oil prices and offsetting pressure from rising natural rubber costs, along with more limited upside following recent share price gains.

What’s in the News for Bridgestone

- Bridgestone issued consolidated earnings guidance for the fiscal year ending December 31, 2026. The company expects revenue of ¥4,500,000 million, profit attributable to owners of parent of ¥340,000 million, and basic earnings per share of ¥270.87. Source: company guidance.

- The company announced a second quarter end dividend for the fiscal year ending December 31, 2026 of ¥60.00 per share, with the scheduled dividend payment commencement date on September 1, 2026. Source: company dividend announcement.

- Bridgestone provided year end dividend guidance for the fiscal year ending December 31, 2026 of ¥65.00 per share. Source: company dividend guidance.

- From April 1, 2026 to June 30, 2026, Bridgestone repurchased 17,688,700 shares, representing 1.4% of shares, for ¥59,586.11 million. This completed a total repurchase of 32,118,900 shares, representing 2.53% of shares, for ¥109,274.09 million under the buyback announced on February 16, 2026. Source: company buyback update.

Valuation Changes for Bridgestone

- The Fair Value estimate has risen slightly, moving from ¥3,652.31 to ¥3,727.69 per share.

- The Discount Rate has edged higher, from 6.70% to 6.81%.

- The Revenue Growth assumption is a bit higher, shifting from 3.67% to 3.94%.

- The Net Profit Margin forecast is slightly firmer, moving from 8.76% to 8.98%.

- The future P/E multiple has been reduced, moving from 10.84x to 9.82x.

Key Takeaways

- Bridgestone's shift to premium and specialty tires aims to drive revenue and margin growth due to higher profit margins.

- Strategic growth investments in India target the premium car tire market to enhance market leadership and drive revenue growth in a growing region.

- Challenges in multiple markets, structural changes, and high costs indicate potential strains on profitability and revenue growth for Bridgestone.

Catalysts

About Bridgestone- Manufactures and sells tires and rubber products.

- Bridgestone is focusing on restructuring and rebuilding its European and Latin American operations, particularly aiming to improve profitability by optimizing production and distribution. This effort should positively impact net margins as efficiency improves by 2026.

- The company is enhancing its sales mix with a focus on premium tires and specialty tire solutions in areas like ultra-large mining and aircraft tires. This shift toward high-value products is expected to drive revenue growth and margin expansion due to their higher profit margins.

- Bridgestone is actively implementing cost reductions globally, anticipating an annualized impact of approximately ¥66 billion. These cost-saving measures are expected to improve operating income and net margins starting from 2025.

- In North America, Bridgestone is strengthening its multi-brand strategy, including the introduction of new Firestone and ENLITEN tire products in 2025, which is expected to increase market share and revenue.

- The company plans strategic growth investments in India, targeting the premium passenger car tire market. This initiative aims to enhance market leadership and revenue growth in a region with expected continued growth.

Bridgestone Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Bridgestone's revenue will grow by 3.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.8% today to 9.0% in 3 years time.

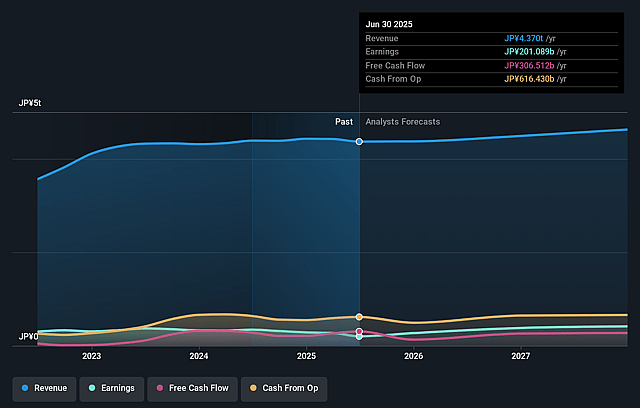

- Analysts expect earnings to reach ¥467.1 billion (and earnings per share of ¥425.37) by about August 2029, up from ¥408.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ¥558.5 billion in earnings, and the most bearish expecting ¥360.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 9.8x on those 2029 earnings, down from 12.8x today. This future PE is greater than the current PE for the JP Auto Components industry at 9.7x.

- Analysts expect the number of shares outstanding to decline by 6.7% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.81%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Challenges in the Latin American market, particularly Brazil's struggle with low-priced imports and profitability issues, suggest sustained financial strain, potentially decreasing future revenues and net margins.

- Lower unit sales and profitability in North America's aftermarket passenger car tire segment indicate pressure on earnings, impacting overall revenue growth.

- Structural changes in the European and Latin American markets demand significant restructuring costs, which could reduce net margins and delay profit recovery.

- Increased low-cost imports from Asia in the North American replacement market may apply downward pressure on product pricing, affecting gross margins and future earnings.

- Persistent high costs in the Chemical and Industrial Products sectors, along with start-up costs for new EV-related businesses, could hinder profit margins, impacting cash flow and overall profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ¥3727.69 for Bridgestone based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥4300.0, and the most bearish reporting a price target of just ¥3400.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ¥5203.9 billion, earnings will come to ¥467.1 billion, and it would be trading on a PE ratio of 9.8x, assuming you use a discount rate of 6.8%.

- Given the current share price of ¥4199.0, the analyst price target of ¥3727.69 is 12.6% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Bridgestone?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.