Last Update 07 Jun 26

Fair value Increased 8.88%SOBI: Gout And Lipid Trials Will Gradually Shape A More Balanced Outlook

Narrative Update: Swedish Orphan Biovitrum

Analysts have lifted their price target for Swedish Orphan Biovitrum from SEK 433.18 to SEK 471.67, citing updated assumptions for fair value, discount rate, revenue growth, profit margin and future P/E following a recent bullish research initiation on the stock.

What's in the News

- Sobi reported positive topline Phase 3 REDUCE 2 results for pozdeutinurad in adults with gout, with both tested doses achieving the primary goal of more patients reaching serum uric acid levels below 6 mg/dL at month 6 compared with placebo, and safety in line with prior studies. Source: company announcement, May 21, 2026.

- New pooled Phase 3 CORE and CORE2 data for Tryngolza (olezarsen) in severe hypertriglyceridemia showed an 85% relative reduction in acute pancreatitis risk and a 66% reduction in triglycerides after six months, with 85% of treated patients reaching triglyceride levels below 10 mmol/L. The U.S. FDA accepted Tryngolza for Priority Review in February 2026. Source: company announcement, May 26, 2026.

- The European Medicines Agency validated an indication extension application for Tryngolza in adults with severe hypertriglyceridemia with triglyceride levels at or above 880 mg/dL, backed by Phase 3 CORE and CORE2 results previously published in The New England Journal of Medicine.

- Sobi reaffirmed its 2026 earnings guidance, indicating an expectation for revenue to grow at a low double digit rate at constant exchange rates.

- Health Canada approved EMPAVELI (pegcetacoplan) for certain rare kidney diseases, C3 glomerulopathy and primary immune complex membranoproliferative glomerulonephritis, based on the Phase 3 VALIANT study that reported reductions in proteinuria, stable kidney function and clearance of C3 deposits.

Valuation Changes

- Fair Value: increased from SEK 433.18 to SEK 471.67, indicating a modest upward adjustment in the assessed equity value.

- Discount Rate: decreased from 5.52% to 5.47%, reflecting a slight reduction in the rate used to discount future cash flows.

- Revenue Growth: revised from 11.88% to 12.29%, indicating a small upward revision to expected top line growth, expressed in SEK.

- Net Profit Margin: adjusted from 21.56% to 21.44%, showing a marginal downward adjustment to expected profitability.

- Future P/E: increased from 21.01x to 21.98x, indicating a modest increase in the valuation multiple applied to future earnings.

Key Takeaways

- Successful Altuvoct launch in Europe and expanding regulatory approvals for Aspaveli and Gamifant could significantly boost revenue through market share growth and new entries.

- Strategic operational efficiency, cost management, and increased Beyfortus royalties are expected to enhance margins and stabilize earnings.

- Reliance on international expansion and competition challenges may limit revenue growth, while geopolitical and regulatory factors could further impact margins and earnings stability.

Catalysts

About Swedish Orphan Biovitrum- A biopharma company, provides medicines in the areas of haematology, immunology, and specialty care in Europe, North America, the Middle East, Asia, and Australia.

- The successful launch and rapid adoption of Altuvoct in markets like Germany, where it achieved a 57% market share within 9 months, present a significant opportunity for market share growth in Europe, potentially boosting future revenues.

- The expected regulatory approvals and market entries for Aspaveli in nephrology indications and Gamifant in secondary HLH show potential for new revenue streams, as these products address unmet medical needs in growing markets.

- Expansion of Gamifant into new indications, such as interferon-gamma-driven sepsis and the subsequent international filings, could drive significant long-term revenue growth, solidifying its position in an untapped market segment.

- The ongoing development and subsequent potential label expansion of Vonjo through the PACIFICA Phase III study and international launches may unlock new growth areas, positively impacting revenue and earnings.

- The strategic focus on enhancing operational efficiency and cost management, alongside anticipated increased royalty rates from Beyfortus, should support margin improvement and earnings stabilization in the coming years.

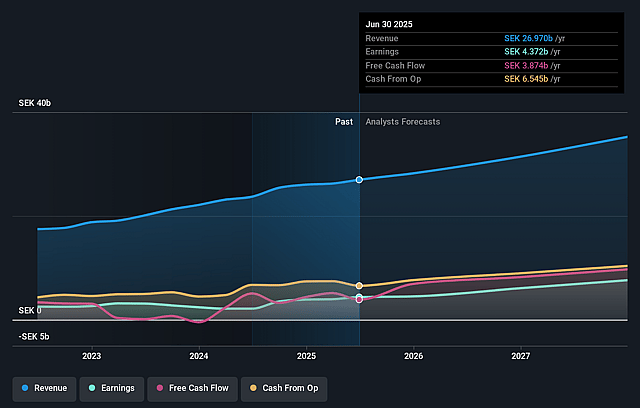

Swedish Orphan Biovitrum Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Swedish Orphan Biovitrum's revenue will grow by 12.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.2% today to 21.4% in 3 years time.

- Analysts expect earnings to reach SEK 8.8 billion (and earnings per share of SEK 25.81) by about June 2029, up from SEK 921.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting SEK11.7 billion in earnings, and the most bearish expecting SEK7.5 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 22.0x on those 2029 earnings, down from 167.7x today. This future PE is lower than the current PE for the GB Biotechs industry at 37.2x.

- Analysts expect the number of shares outstanding to grow by 0.36% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.47%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The growth rate, while positive, is relatively modest at 3% due to discontinuation of certain manufacturing revenues and seasonal impacts, potentially signaling limited expansion capacity which could affect future revenue expectations.

- The reliance on international expansion for products like Altuvoct is subject to reimbursement and regional regulatory challenges, particularly in markets like Spain and France, which could impact revenue growth if expected launches face delays.

- The intensified competition in some therapeutic areas, such as the competition Aspaveli faces from new oral medicines, may exert downward pressure on pricing or slow market penetration, affecting net margins and revenue.

- Stocking issues and adjustments related to Medicare Part D reform have negatively impacted Vonjo's quarterly performance, highlighting risks that might disrupt earnings consistency if not managed effectively.

- Fluctuating exchange rates and potential tariffs due to geopolitical factors could affect both revenue and EBITDA margins, as a significant portion of operations and sales occur in multiple currencies outside of the Swedish krona.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SEK471.67 for Swedish Orphan Biovitrum based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK550.0, and the most bearish reporting a price target of just SEK350.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SEK41.0 billion, earnings will come to SEK8.8 billion, and it would be trading on a PE ratio of 22.0x, assuming you use a discount rate of 5.5%.

- Given the current share price of SEK446.6, the analyst price target of SEK471.67 is 5.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Swedish Orphan Biovitrum?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.