Last Update 02 May 26

Fair value Increased 30%NOD: Edge AI And Device Management Progress Will Support Shares Despite Mixed Sentiment

Narrative fair value for Nordic Semiconductor has been updated from NOK 145.70 to NOK 189.31, reflecting higher analyst price targets around NOK 185 and analyst expectations for modestly higher revenue growth, profit margins, and a richer future P/E multiple.

Analyst Commentary

Recent research points to a split in sentiment around Nordic Semiconductor, with several large banks adjusting price targets toward NOK 185 while at least one firm has turned more cautious on the shares. This mix of views gives you a useful cross check on both upside potential and execution risks that might impact the updated narrative fair value of NOK 189.31.

Bullish Takeaways

- Bullish analysts lifting price targets toward NOK 185 are effectively signaling confidence that current valuation leaves room for further upside if revenue growth and margins track their expectations.

- Higher targets from major firms, including JPMorgan and others, suggest that the sector backdrop and company positioning are seen as supportive of a richer future P/E multiple than previously assumed.

- The cluster of price targets around a similar level reinforces the idea that there is some alignment among bullish analysts on what they view as a reasonable medium term value anchor.

- Bullish research generally ties its optimism to execution on growth and profitability, implying that if management delivers on these fronts, the updated narrative fair value is within the range of market expectations.

Bearish Takeaways

- Bearish analysts, including SEB Equities, have moved to a more cautious stance, which points to concerns around execution risks that might make it harder to justify higher valuation multiples.

- The downgrade highlights the possibility that growth or margin expectations embedded in higher price targets could prove demanding, especially if end market demand or competitive pressures do not cooperate.

- More cautious views also draw attention to the gap between current trading levels, the NOK 185 analyst targets, and the NOK 189.31 narrative fair value, suggesting that upside may be sensitive to smaller missteps in delivery.

- This mix of upgrades and downgrades indicates that while there is support for higher valuation levels, there is also meaningful debate on how consistently Nordic Semiconductor can execute against those expectations.

What’s in the News

- Nordic introduced a lifetime FOTA and device management license through nRF Cloud to help device makers meet upcoming EU Cyber Resilience Act security update requirements from 2027, with pricing starting at US$1 per device and coverage across nRF54, nRF53, nRF52 and nRF91 platforms (Key Developments).

- The company advanced its edge AI roadmap with broad availability of the NPU enabled nRF54LM20B SoC, which targets real time intelligence for wearables, smart home, industrial and medical sensors, and other battery powered devices, with development kits already available and volume production of the SoC expected to begin in Q2 2026 (Key Developments).

- Nordic announced Fuel Gauge v2.0 for its nPM1300 and nPM1304 power management ICs, adding State of Health tracking, adaptive battery modeling and fleet analytics to help manufacturers comply with EU battery regulations and manage large deployed device fleets through nRF Cloud (Key Developments).

- The nRF54L Series was expanded with entry level nRF54LS05A and nRF54LS05B Bluetooth LE SoCs aimed at simple, cost focused devices such as tags, sensors and PC peripherals, with evaluation available now and production targeted for Q3 2026 (Key Developments).

- The company broadened its cellular IoT line up with new nRF92 and nRF93 Series products and updates to the nRF91 Series, including support for satellite NTN and sub GHz fallback, with nRF93M1 general availability planned from mid 2026 and nRF92 Series general availability from early 2027 (Key Developments).

Valuation Changes

- Fair Value Narrative: NOK 145.70 has been updated to NOK 189.31, indicating a higher central value in the current narrative framework.

- Discount Rate: 9.81% has shifted to 9.95%, reflecting a slightly higher required return applied in the valuation inputs.

- Revenue Growth: Assumed long term dollar revenue growth has moved from 14.10% to 15.35%, pointing to a somewhat stronger growth profile in the model.

- Net Profit Margin: Assumed dollar net profit margin has adjusted from 11.23% to 11.90%, indicating a modestly higher profitability assumption.

- Future P/E: The future P/E multiple has changed from 34.16x to 45.69x, implying a richer valuation multiple embedded in the updated narrative fair value.

Key Takeaways

- Market optimism may be overestimating sustainable revenue growth, as cyclical benefits and external risks could limit long-term sales and profitability.

- High valuation is tied to growth in green technology and IoT, but rising costs, regulatory pressures, integration challenges, and increased competition threaten margins and earnings.

- Strong innovation, broadening market reach, and a strategic solutions shift position Nordic Semiconductor for sustained growth, margin resilience, and long-term competitive differentiation.

Catalysts

About Nordic Semiconductor- A fabless semiconductor company, develops and sells integrated circuits for use in short- and long- range wireless applications in Europe, the Americas, and the Asia Pacific.

- Investors may be overestimating Nordic Semiconductor's ability to sustain current high revenue growth rates as the company is currently benefitting from a cyclical rebound, inventory normalization, and restocking, while long-term consumer and industrial customer demand could slow due to macroeconomic volatility or shifts in global buying patterns; this could impact future revenue growth sustainability.

- Optimism about the company's exposure to green technology and sustainability trends could be inflating valuation, but tightening regulatory requirements and European climate policies may increase compliance costs and CapEx, potentially leading to downward pressure on net margins and earnings over time.

- The move toward a solution-oriented, chip-to-cloud provider and recent M&A (Newton AI, Memfault) are seen as strong long-term growth catalysts, but integration risks and consistently high R&D and OpEx requirements, especially for high-salary software talent, could weigh on profitability and net margins in the near term.

- Current multiples may reflect investor confidence that the ongoing proliferation of IoT, smart city, and digitalization trends will continue to drive above-market revenue and market share gains; if adoption rates plateau or competition intensifies (especially from low-cost or Asian providers), revenue growth and gross margins could disappoint relative to expectations.

- Elevated valuation could also be supported by expectations that Nordic's expansion in power management ICs and advanced SoCs (nRF54 series) will lead to accelerated sales traction and attach rates; a slower ramp due to extended customer design cycles, certification lags, or delays in broad-based adoption could limit earnings and revenue upside versus optimistic assumptions.

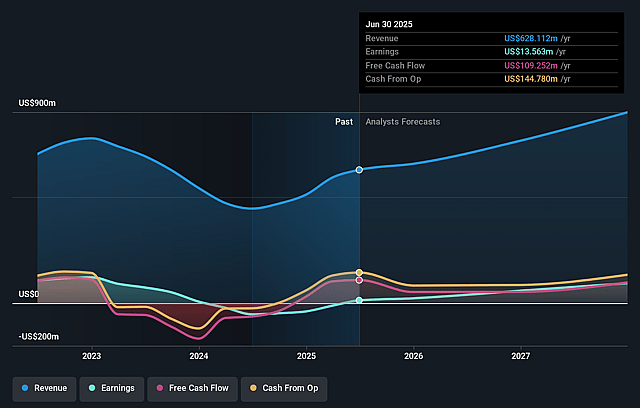

Nordic Semiconductor Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Nordic Semiconductor's revenue will grow by 15.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.7% today to 11.9% in 3 years time.

- Analysts expect earnings to reach $128.8 million (and earnings per share of $0.69) by about May 2029, up from $25.9 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $244.3 million in earnings, and the most bearish expecting $92.1 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 45.8x on those 2029 earnings, down from 156.3x today. This future PE is lower than the current PE for the GB Semiconductor industry at 156.3x.

- Analysts expect the number of shares outstanding to grow by 3.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.95%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Robust year-on-year revenue growth and recovery across both short

- and long-range product segments, with sustained demand from key customers in industrial, healthcare, and consumer markets, indicates potential for continued top-line expansion in the medium to long term, supporting future revenue growth.

- Ongoing product innovation and expansion, including the launch of the nRF54 series, extended PMIC offerings, and acquisitions like Newton AI and Memfault (cloud life cycle management), position Nordic as a leader in low-power, integrated semiconductor solutions and differentiated full-stack offerings, potentially enabling margin resilience and defending against commoditization.

- High customer engagement and a strong design pipeline for recently launched and upcoming products, along with significant leadership in Bluetooth Low Energy design certifications, suggest long-term customer stickiness, broadening market reach, and higher chances of recurring revenues and design win-driven growth.

- Commitment to sustainability and recognition as one of Europe's and the world's most sustainable companies increases Nordic's appeal to eco-conscious customers and partners across geographies, opening pathways to large, sustainability-driven contracts and long-term competitive differentiation, potentially leading to higher sales or improved margins.

- Strategic shift toward becoming a solutions provider (hardware, software, and cloud) diversifies Nordic's revenue streams, increases customer lock-in, and reduces business risk associated with reliance on single markets or product lines, supporting more stable EBITDA and earnings growth over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of NOK189.31 for Nordic Semiconductor based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK235.0, and the most bearish reporting a price target of just NOK134.01.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.1 billion, earnings will come to $128.8 million, and it would be trading on a PE ratio of 45.8x, assuming you use a discount rate of 9.9%.

- Given the current share price of NOK189.0, the analyst price target of NOK189.31 is 0.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Nordic Semiconductor?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.