Last Update 25 Nov 25

Fair value Decreased 1.12%MTCH: Share Buybacks And Improved Margins Will Support Earnings Upside Ahead

Match Group's analyst price target was modestly reduced from $37.74 to $37.32, as analysts cited slight adjustments in expected revenue growth and discount rates while highlighting stable future profit margins.

Analyst Commentary

Market observers provide mixed signals regarding Match Group's near-term prospects, focusing on the balance of valuation, growth execution, and external risks impacting the stock's outlook.

Bullish Takeaways- Bullish analysts anticipate stable profit margins, suggesting the company has effectively managed operational inefficiencies and controls.

- Incremental improvements in price targets, even if modest, reflect confidence in Match Group's ability to deliver steady revenue growth.

- Analysts with a forward-looking perspective remain constructive due to the company's market position and potential for future upside as digital dating adoption continues globally.

- Bears highlight that the upward momentum in the share price may already reflect much of the anticipated operational improvements, limiting upside potential from current levels.

- Analysts emphasize that growth upside relies heavily on consistent execution and the realization of projected cost efficiencies.

- Ongoing concerns include sensitivity to broader macroeconomic variables, with revenue growth susceptible to competitive pressures and changes in consumer spending behavior.

What's in the News

- Match Group repurchased 6,688,891 shares between July and October 2025, completing a total buyback of 18,774,147 shares. This represents 7.6% of outstanding shares, for $602.57 million under its current buyback program. (Company filing)

- The company issued new earnings guidance for Q4 2025, projecting total revenue of $865 million to $875 million, up 1% to 2% year-over-year, and net income attributable to shareholders between $159 million and $164 million. (Company press release)

- Tinder, Match Group’s flagship app, launched Face Check, a mandatory facial verification feature for new users in select U.S. regions and globally. Early results showed over 60% decrease in exposure to bad actors and over 40% reduction in bad actor reports, contributing to improved user safety and authenticity. (Company announcement)

Valuation Changes

- Consensus Analyst Price Target has decreased modestly from $37.74 to $37.32.

- Discount Rate has risen slightly from 9.68% to 9.70%.

- Revenue Growth expectations declined from 5.24% to 5.07%.

- Net Profit Margin has improved slightly, increasing from 20.51% to 20.69%.

- Future P/E ratio forecast dipped from 11.77x to 11.66x.

Key Takeaways

- AI-driven innovation, safety enhancements, and alternative payments are set to boost engagement, retention, and profitability across Match Group's brands.

- Focused global expansion and shifting cultural trends help diversify users and revenue sources while strengthening growth beyond mature core markets.

- Declining user metrics, overreliance on Tinder, increased competition, regulatory costs, and user trust concerns threaten Match Group's long-term revenue growth and profitability.

Catalysts

About Match Group- Engages in the provision of digital technologies.

- Accelerated product innovation-especially at Tinder and Hinge with new AI-powered features, personalization, trust/safety enhancements, and lower-pressure connection options for Gen Z-should revitalize user growth, increase engagement, and support higher payer conversion rates; this is likely to drive sustained top-line revenue and margin expansion as new features mature.

- Strong international expansion plans for Hinge and other brands, targeting markets like Europe, Mexico, Brazil, and broader Asia, position Match Group to capture growth from increasing smartphone and internet adoption worldwide-expanding the addressable user base and diversifying revenue beyond more saturated U.S. markets.

- Growing societal acceptance and normalization of online dating, reinforced by product improvements focused on safety and authenticity (e.g., face check and bot detection), should reduce friction to adoption, broaden the user demographic, and support elevated ARPU and payer conversion, positively impacting long-term revenue and earnings.

- Successful rollout and optimization of alternative payment options (particularly on iOS), building on early test results of >30% transaction shift to web and >10% net revenue uplift, offer substantial potential for margin improvement and higher adjusted operating income (AOI)/free cash flow, with an estimated $65M AOI saving opportunity in 2026.

- Data-driven organizational and cultural turnaround (with flattened teams, rapid product cycles, and cross-brand AI/model sharing) increases efficiency and positions Match Group to leverage its large data set to improve user retention and stickiness-contributing to higher lifetime value and healthier net margin trends over the medium to long term.

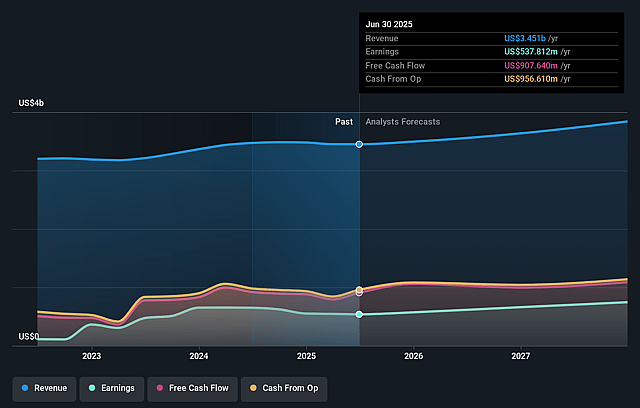

Match Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Match Group's revenue will grow by 5.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 15.6% today to 20.3% in 3 years time.

- Analysts expect earnings to reach $811.8 million (and earnings per share of $3.56) by about September 2028, up from $537.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.9x on those 2028 earnings, down from 17.1x today. This future PE is lower than the current PE for the US Interactive Media and Services industry at 17.0x.

- Analysts expect the number of shares outstanding to decline by 4.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.94%, as per the Simply Wall St company report.

Match Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistent year-over-year declines in Match Group's core user metrics-such as new account registrations, monthly active users (MAU), and payers-highlight demographic headwinds, competition, and product fatigue, which, if not fully reversed, could pressure long-term revenue growth and earnings.

- Overdependence on Tinder as the primary revenue driver presents significant risk, as Tinder direct revenue declined 4% year-over-year (and payers are down 7%), indicating potential market share loss or saturation, which could undermine revenue and net margins if product turnarounds do not succeed.

- Intensifying competition, including proliferating free and AI-powered dating options, may erode Match Group's pricing power and user engagement, resulting in higher customer acquisition costs and downward pressure on both revenue per payer and profitability.

- Increased regulatory scrutiny, evidenced by penalties such as the $14 million FTC settlement and ongoing need for compliance with data privacy and digital payments regulations, may elevate costs and limit monetization strategies, compressing long-term net margins and earnings.

- Ongoing user concerns regarding trust, safety, and digital burnout-alongside Match Group's need to continually enhance moderation and safety features-could dampen user growth and engagement, leading to higher operating expenses or reduced monetization potential, ultimately impacting overall revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $38.474 for Match Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $49.0, and the most bearish reporting a price target of just $31.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $4.0 billion, earnings will come to $811.8 million, and it would be trading on a PE ratio of 12.9x, assuming you use a discount rate of 8.9%.

- Given the current share price of $38.21, the analyst price target of $38.47 is 0.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.