Last Update 18 May 26

Fair value Increased 23%SCST: Multi Instalment Dividend And Higher Margins Will Support Fairly Valued Shares

Analysts have lifted their SEK fair value estimate for Scandi Standard from SEK111.33 to SEK136.75, reflecting updated assumptions around the company’s discount rate, revenue growth, profit margins and future P/E expectations.

What's in the News

- The board of directors has proposed a total dividend of SEK 3.30 per share for the 2025 financial year, planned to be paid in two equal installments of SEK 1.65 per share, subject to approval at the annual general meeting (Key Developments).

- If approved, the first dividend payment is expected to have a record date of Thursday, 30 April 2026, with distribution scheduled for 6 May 2026. The second payment is expected to have a record date of Friday, 18 September 2026, with distribution scheduled for 23 September 2026, handled by Euroclear Sweden AB (Key Developments).

- The proposed total dividend corresponds to approximately SEK 216 million, based on all shares in the company excluding any treasury shares that may be held on the record dates. This means the final amount could change if the company buys or sells its own shares before those dates (Key Developments).

- The annual general meeting held on 28 April 2026 resolved on a total dividend of SEK 3.30 per share, in line with the board’s proposal. The second installment of SEK 1.65 per share is scheduled for payment on 23 September 2026, with a record date of Friday, 18 September 2026 (Key Developments).

Valuation Changes

- Fair Value: SEK111.33 to SEK136.75, indicating a higher central estimate for the stock.

- Discount Rate: 5.224% to 5.344%, a slight upward adjustment to the required return used in the valuation model.

- Revenue Growth: 5.76% to 5.69%, a marginally lower growth assumption for future SEK revenue.

- Net Profit Margin: 3.77% to 3.98%, reflecting a modestly higher expected profitability level.

- Future P/E: 13.42x to 15.35x, implying a higher valuation multiple assumed for future earnings.

Key Takeaways

- Expectations for sustained demand and premium pricing may prove optimistic if consumer trends shift toward plant-based proteins or regulatory pressures increase costs.

- Anticipated volume growth from capacity expansions relies on flawless execution, with operational delays or integration issues posing risks to earnings and efficiency.

- Strong market position, efficiency gains, and product innovation drive resilient revenue growth, margin improvement, and enhanced profitability amid favorable industry and consumer trends.

Catalysts

About Scandi Standard- Produces and sells chilled, frozen, and ready-to-eat chicken products in Sweden, Norway, Ireland, Denmark, Finland, Germany, the United Kingdom, rest of Europe, and internationally.

- The current valuation may be pricing in an overly optimistic continuation of the shift from red meats to poultry, assuming sustained robust consumer demand for chicken amid global health and wellness priorities; this could lead to disappointment if consumer trends toward plant-based alternatives accelerate, resulting in slower revenue growth than expected.

- The share price appears to factor in continued success in passing through higher production costs via price increases, despite ongoing volatility in input costs (notably feed), and assumes minimal margin pressure-even though there is increasing regulatory focus and potential public pressure on carbon emissions and animal welfare, which could drive up costs and compress profit margins.

- Investors seem to expect Scandi Standard's recent and planned capacity expansions (such as the Lithuanian and Dutch plants) will drive significant volume growth and enhanced efficiency, yet this relies on flawless execution of ramp-ups and integration-any delays or cost overruns could result in below-forecast earnings and ROCE.

- The market appears to be extrapolating strong export price growth and retail demand, potentially overlooking cyclical risks or downside from increased substitution by alternative proteins, which could lead to lower-than-anticipated top-line growth if global consumer preferences change or export markets slow.

- The valuation likely reflects the belief that Scandi Standard's leadership in sustainability and animal welfare will maintain premium pricing and market share; however, if regulatory standards tighten further or new entrants with disruptive plant-based or low-carbon alternatives gain traction, this could compress net margins and erode competitive advantage.

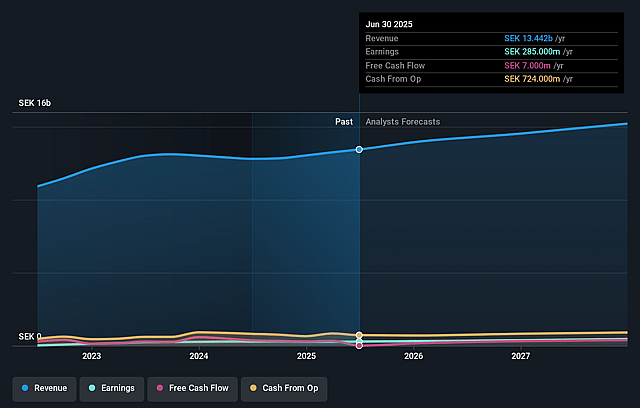

Scandi Standard Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Scandi Standard's revenue will grow by 5.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.8% today to 4.0% in 3 years time.

- Analysts expect earnings to reach SEK 676.9 million (and earnings per share of SEK 9.25) by about May 2029, up from SEK 402.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as SEK588.6 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.4x on those 2029 earnings, down from 22.7x today. This future PE is lower than the current PE for the GB Food industry at 22.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.34%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Strong ongoing and growing demand for chicken, supported by long-term trends of consumers switching from red meat (beef and pork) to poultry for reasons of affordability, sustainability, and health, helps insulate Scandi Standard's revenues from secular volume declines.

- Significant investments in new production capacity (Lithuania, Netherlands/Oosterwolde) position Scandi Standard for substantial volume growth and improved cost efficiency, which are likely to support higher future net sales and margin expansion.

- The company's established market leadership and consolidation in its core markets create high barriers to entry for new competitors, helping Scandi Standard maintain pricing power and stable or improving EBIT margins.

- Ongoing improvements in operational efficiency and automation, as well as strong management of feed and input costs (including hedging), enhance resilience and may positively impact long-term profitability and earnings growth.

- Expansion into value-added and ready-to-eat poultry products is leading to higher returns on capital, diversified revenue streams, and greater pricing power, which together support improved revenue growth and net margins over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SEK136.75 for Scandi Standard based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK160.0, and the most bearish reporting a price target of just SEK102.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SEK17.0 billion, earnings will come to SEK676.9 million, and it would be trading on a PE ratio of 15.4x, assuming you use a discount rate of 5.3%.

- Given the current share price of SEK140.0, the analyst price target of SEK136.75 is 2.4% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Scandi Standard?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.