Key Takeaways

- Pinterest has a differentiated and growing discovery business, catering to young shoppers.

- The project-driven platform attracts close to 500M high-intent MAUs.

- The company is shifting focus to profitability with its lower-funnel tools.

- Classic and new AI will improve discovery and content.

- 55% of users view Pinterest as a place to shop, indicating a high success rate.

- However peers also have good discovery software which could slow Pinterest’s competitive edge.

Catalysts

Pinterest Built A Great Platform, It’s Time To Monetize

Pinterest differentiates itself from competitors as a project-driven platform, where people that embark on projects can find inspiration. Their main value proposition is idea discovery, and primarily targets young female demographics as well as project-driven shoppers.

Users tend to experience friction between gathering ideas and finding the items in online stores. This is a part of the solution offered by Pinterest, as the company is designing its platform to connect people’s ideas closer to realization.

The company showcased the steps it took in order to decrease the gap between idea to action by adding lower-funnel advertising solutions:

- Mobile and direct deep linking: This allows users to click on an ad and be taken directly to the relevant product page on the advertiser's website or mobile app.

- Shopping ads: Shopping ads allow users to see product prices and availability directly on Pinterest - bringing users closer to a decision without leaving the platform.

- API for conversions: This allows advertisers to track conversions from Pinterest ads and measure the campaign effectiveness. Advertisers are responding positively and have increased their spend by more than 30%.

The results from this have been positive. In 2023, only 2% of Pinterest's revenue came from customers who used at least three of the company's lower funnel tools. This number has significantly grown to 23%, demonstrating an improving user experience.

While the key vertical in the past was building the visual idea platform, Pinterest will now add focus to the other side and work on monetization. Executing on this side will allow the company to demonstrate the latent potential it has built thus far, and will be reflected in scaling up profitability.

Pinterest Is Establishing Itself As The Place To Find Ideas

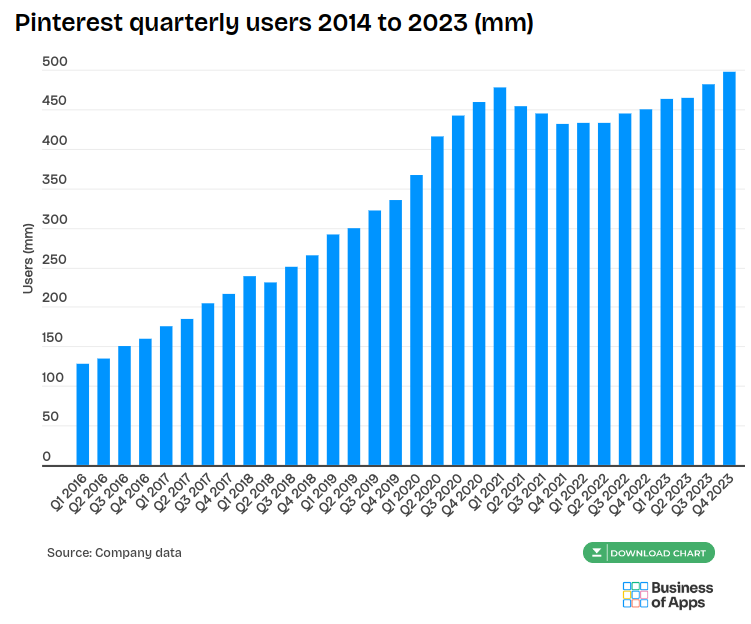

The company’s focus on improving the user experience with features like collages and shoppable content is driving growth. The platform is still in the high-growth phase and has posted a 18.5% CAGR of monthly active users from 2016 through 2023. In that time, Pinterest has increased its user base from 128M to 498M.

Pinterest monthly active users 2016 to 2024

Pinterest’s CEO notes that the platform is built in a way that aligns the interests of advertisers with shoppers - which makes Pinterest closer to Google, as a search engine tailored for idea generation. This is especially important as people use Pinterest with intent frequently in the categories of: fashion, events, home, reconstruction, and recently even travel.

The feature improvements have generated positive reception from advertisers, as the CEO notes that “...Brands are responding by using our full suite of products to drive even better campaign performance. Pinterest is the rare business where the interests of users and advertisers are aligned. It’s proven to be true as we continue to post double-digit revenue growth and have achieved an all-time high for global MAU.”

The half a billion monthly active users indicate a substantial monetization opportunity as the platform develops in the future. When compared to Meta (Facebook) - a relatively close advertising peer, we can see that in Q4 Pinterest’s average revenue per user was 1⁄6th of what Meta makes globally, and 1⁄8th of their U.S. & Canada ARPU.

Pinterest average revenue per user

While this is not a direct comparison, it does showcase that Pinterest has room to grow margins in the future.

Advertising Tools And AI Are Key Verticals

When considering AI for Pinterest, I am referring to the classic discovery and categorization algorithms that companies use to increase engagement and conversions, as well as the new generative AI which Pinterest can use to improve content.

Pinterest relies on Amazon’s AWS cloud infrastructure for major parts of its services. This allows the company to focus on building their engine, while their storage, data solutions, machine learning and other infrastructure is handled by AWS. The company has an ongoing contract with AWS, committing to spend $3.25B from 2021 to 2029.

- Pinterest Lens (image AI): allows users to snap a picture of an object and let the AI identify similar pins, so that the user can find inspiration much faster than manually browsing. Pinterest Lens uses AWS Elastic Compute Cloud to refine its machine learning recommendation system on a daily basis, giving users more relevant content.

- Recommendation AI: Pinterest uses AWS Rekognition to identify, describe and classify objects in images, giving their AI valuable context when tailoring recommendations to users.

The company is also adding features to their internal and advertising tools, enabling higher conversions for customers:

- Business Manager: The platform for advertisers is getting new features including dashboards for better performance visibility, and audience sharing for improved targeting.

- Creative Studio: This has the highest potential to leverage generative AI. Pinterest already set the stage for assisting creators in preparing marketing materials by using their creative studio resources. With the advent of visual generative AI, it is likely that this platform will become even more valuable to advertisers, as it helps them generate parts or whole marketing creatives. Conversely, this feature is a direct competitor to Meta’s creative hub, and has the potential to offer independent aspects comparable to Adobe’s Experience Cloud. While the peers target enterprise level advertisers, it is good to see Pinterest entering the scene with their own solution.

- Premiere Spotlight: Allows brands to exclusively own premium ad placements on the platform to promote their campaigns.

- Collages: Using the mentioned visual ML technology, users can cut objects from an image and combine them with other elements to create more appealing pins. Applying generative AI enables additional creative options and makes designing pins and ads faster.

The advent of AI gives Pinterest room to expand their professional tools and give marketers more resources to work with. It will be no surprise if the company experiments with allowing AI to suggest examples for headlines, descriptions, on-creative copy, etc., in the near future. Pinterest may also leverage its large scale ML engine to help creators A/B test better performing creative or individual elements and give suggestions for improvement.

Partnerships And Gen Z To Drive Growth

Pinterest is partnering with Amazon and Google to bring 3rd party ads to the platform. The company started implementing Amazon’s and Google’s ad content on the platform and expects to increase monetization, especially in international markets. While this will take some portion of the margins off the table for Pinterest, it will also enable users to find better ideas that are relevant for the projects they are engaged in.

The company reports that 55% of users see Pinterest as a place to shop. While the US user base is still growing, a significant portion of new users come from international regions. Gen Z is the fastest-growing demographic on Pinterest, now representing over 40% of all users. This focus on a younger audience bodes well for Pinterest's long-term prospects, as capturing a younger generation has the benefits of selling to early adopters and converting them to loyal customers as they narrow down the shopping platforms as they get older.

Despite the macro pressures and weakened digital ads market, Pinterest continues to invest in growth projects such as AI and product features centered around engagement and tools for marketers. The company is also starting to work on profitability with a focus on adjusted EBITDA which it expanded by 6.6%, indicating that there is a long way to go before finding the bottom-line.

The company has an employee base of around 4k, indicating that there is a good portion of manual operations needed. Given that Pinterest is a self-service platform, further optimization in the processes may be able to automate part of these operations - This should be balanced against the growth phase, so I don’t see the company embarking on optimization anytime soon.

Management expects Pinterest to grow Q1’24 revenues between 15% to 17%, reaching around $700M. I see no signs of Pinterest slowing down its long-term top line growth rate, especially as the company becomes more competitive with other advertising platforms such as Instagram and TikTok. For this reason, I will err on the side of optimism and allow the numbers to reveal when the company saturates its market instead of calling a cap too soon.

Assumptions

Revenue: I expect Pinterest to continue its growth trajectory slowly decelerating over time. I estimate the 5-year average annual growth rate to be around 15%, leading to revenues of $6.15B in 2029. This is a reasonable growth rate for Pinterest, but because of the nature and scale of software, it also leaves some room for positive surprises.

Profit: Earnings are a closer approximation of the company’s true bottom-line given that Pinterest is a heavy user of stock-based compensation ($648M in the trailing year), and free cash flows may be overestimating what the company can make for investors. I also expect Pinterest to have margin expansion opportunities in the future, leading to 20% profit margins in 5 years. This results in earnings of $1.2B.

Share count: Pinterest is currently engaged both in buying back its shares, as well as issuing stock-based compensation. The company seems to be doing this in order to optimize the financial side of operations, rather than return capital to shareholders. In my view, it is still early for the company to optimize returns, and I appreciate their current approach in driving growth with stock incentives. For this reason I expect that the number of shares will stabilize at 700M in the next 5-years.

Multiple: I expect growth enthusiasm to persist, and Pinterest to maintain a 25x PE multiple in five years. While growth opportunities from monthly active users may plateau in the next five years, I assume that the company will find ways to increase their service offering and grow profits by increasing the spend from existing customers.

Risks

- Increased competition from established e-commerce platforms: While Pinterest offers a unique user experience, established e-commerce players like Amazon and Etsy are constantly improving their discovery features. This could make it harder for Pinterest to maintain its competitive edge.

- Pressure from e-commerce stores: Competition in e-commerce has gradually increased as more startups are improving their software and providing incentives for customers to discover and shop on their sites. These include companies like: Zalando, Otrium, Wayfair, as well as Shopify-enabled online merchants.

- Competition from social media platforms: Apps like Instagram and TikTok are also heavily focused on visual content and increasingly incorporate shopping features.

- Limited network effects: Pinterest is a project-driven platform for customers that want to do something, but may lack the ideas. This means that while the platform lends itself to engaged users that are trying to solve a problem, it finds it difficult to produce network effects which the likes of Instagram make use of. With the exception of a small fraction of power users, there is little long-term utility in following someone for a short-term project, and sharing ideas is easily done outside of the platform. While this limits the growth path of Pinterest, it also gets them away from the direct-competitor category of Meta, allowing the platform to develop other growth paths, such as incentivizing advertisers to create and curate content on the platform.

How well do narratives help inform your perspective?