Last Update 15 Jun 26

ARJO B: Future Upside Will Rely On Stable Margins And Required Yield

Analysts are keeping their SEK price target for Arjo steady at SEK27.0, citing relatively unchanged fair value views, along with slightly adjusted assumptions for discount rate, revenue growth, profit margin and future P/E.

What's in the News

- No recent company specific news, periodical coverage, or key developments for Arjo were provided in the available sources.

- The absence of fresh disclosures means the current SEK27.0 target is being discussed mainly in the context of existing assumptions, rather than new events.

- Investors may want to monitor upcoming company announcements, earnings releases, or regulatory filings for new information that could influence fair value views.

Valuation Changes

- Fair Value: SEK27.0 per share is unchanged, with analysts keeping their SEK27.0 target aligned to the same fair value estimate.

- Discount Rate: Adjusted slightly lower from 7.29% to 7.14%, which marginally raises the present value of projected cash flows in the model.

- Revenue Growth: Assumption nudged higher from 2.87% to 2.91%, reflecting a very small change in expected top line expansion in SEK terms.

- Net Profit Margin: Tweaked upward from 5.40% to 5.43%, indicating a modestly higher expected share of revenue in SEK converting to net profit.

- Future P/E: Brought down slightly from 14.25x to 14.09x, implying a marginally lower valuation multiple applied to future earnings in the model.

Key Takeaways

- Reliance on facility-based solutions and mature markets exposes Arjo to pricing pressure, limited growth, and margin compression amid shifting care models and economic constraints.

- Slow adaptation to digital health innovations and mounting competitive threats risk product obsolescence, market share loss, and persistent profitability challenges.

- Robust North American growth, rising orders, cost efficiencies, successful pricing, and expanding recurring revenues strengthen earnings and support long-term business resilience.

Catalysts

About Arjo- Develops and sells medical devices and solutions for patients for clinical and financial outcomes for healthcare in Europe, Asia, Latin America, Africa, and Pacific.

- As healthcare budgets and government spending face rising pressures, hospitals and care facilities may further reduce reimbursement rates and limit capital investments, directly constraining Arjo's ability to achieve sustainable revenue growth in its core patient handling and mobility equipment segments.

- The accelerating shift toward home-based care and outpatient services threatens to structurally decrease demand for capital-intensive, facility-based solutions, risking meaningful long-term revenue stagnation as Arjo's portfolio remains predominantly geared toward institutional settings.

- With heavy dependence on mature markets such as North America and Europe, where population aging is offset by cost containment policies and slower economic growth, Arjo faces continued pricing pressure that is likely to compress net margins and hinder meaningful top-line expansion.

- If Arjo fails to keep pace with rapid technological advancements and innovation in connected, digital health, and remote monitoring, it risks product obsolescence and market share erosion, ultimately depressing future revenue and profitability.

- Industry-wide threats from increased market consolidation, aggressive pricing from larger medtech competitors, and proliferation of low-cost copycat products from emerging markets may erode Arjo's pricing power and profitability, resulting in lower earnings growth and sustained margin pressure over the coming years.

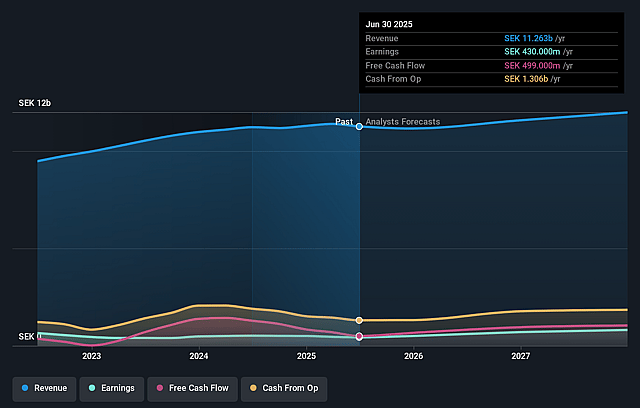

Arjo Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Arjo compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Arjo's revenue will grow by 2.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 3.2% today to 5.4% in 3 years time.

- The bearish analysts expect earnings to reach SEK 641.1 million (and earnings per share of SEK 2.35) by about June 2029, up from SEK 351.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as SEK822.7 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 14.1x on those 2029 earnings, down from 18.9x today. This future PE is lower than the current PE for the SE Medical Equipment industry at 32.0x.

- The bearish analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.14%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Strong organic growth in North America, particularly the United States with over 12% sales growth and no one-off effects, indicates robust demand and operational strength in a key market, which could support higher revenues and earnings in the coming years.

- Back-to-back quarters of rising order intake and a significantly larger order book versus the prior year suggest sustained future sales growth, directly supporting revenue and earnings stability.

- Ongoing cost efficiency measures across the value chain are showing tangible results, with the company now targeting flat operating expenses as a percentage of sales for the full year, which could lead to higher net margins and improved profitability over time.

- Successful introduction of price increases in the U.S. is already helping to offset increased tariffs, with management expressing confidence in their ability to fully compensate for cost headwinds, reducing risk to margins and supporting stable earnings.

- Consistent growth in service and rental business, expansion of patient handling solutions, and successful new product launches point to an evolving business model with higher recurring revenues, which can underpin long-term earnings and revenue resilience.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Arjo is SEK27.0, which represents up to two standard deviations below the consensus price target of SEK30.0. This valuation is based on what can be assumed as the expectations of Arjo's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK33.0, and the most bearish reporting a price target of just SEK27.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be SEK11.8 billion, earnings will come to SEK641.1 million, and it would be trading on a PE ratio of 14.1x, assuming you use a discount rate of 7.1%.

- Given the current share price of SEK24.4, the analyst price target of SEK27.0 is 9.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Arjo?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.