Last Update 09 Apr 26

VLE: Rising Thai Field Production And Buybacks Will Drive Future Repricing

Analysts have kept their CA$16.50 price target for Valeura Energy unchanged, pointing to stable assumptions on fair value, discount rate, revenue trends, profit margin and forward P/E as support for their view.

What's in the News

- A special or extraordinary shareholders meeting is planned for May 14, 2026, in Calgary, Alberta, Canada. This provides a key date to watch for corporate decisions that require shareholder approval (Key Developments).

- A share buyback tranche was completed from October 1, 2025 to November 13, 2025, with 1,457,308 shares repurchased for CA$10.6 million. This brings the total under the November 12, 2024 buyback to 5,034,820 shares for CA$20.88 million, or 4.74% of shares (Key Developments).

- An update on a subsequent buyback program announced November 18, 2025 reported no shares repurchased and no capital deployed between November 18, 2025 and December 31, 2025 (Key Developments).

- An infill drilling campaign was completed at the Manora field in the Gulf of Thailand. Three wells are now producing oil, and reported Manora working interest oil production is 2,626 bbls/d compared with a prior average of 1,950 bbls/d before the new wells came online. The company also plans to move the drilling rig to the Nong Yao field for further production oriented work (Key Developments).

- Production guidance for 2026 was released, with a full year oil production midpoint of 21,000 bbls/d. The company also reported fourth quarter 2025 oil production of 24,721 bbls/d and full year 2025 working interest oil production before royalties of 23.2 mbbls/d, described as an increase of 1.8% over 2024 (Key Developments).

Valuation Changes

- Fair Value: The CA$16.50 estimate is unchanged, reflecting a steady view of the share's core worth on the current assumptions.

- Discount Rate: The discount rate is held flat at 6.254%, indicating no change in the required return used to assess the cash flows.

- Revenue Growth: The modelled revenue change is effectively stable at a 50.82% decline, with only a very small technical adjustment in the figure.

- Net Profit Margin: The assumed net profit margin is essentially unchanged at about 10.06%, with only a minor rounding difference.

- Future P/E: The forward P/E has edged down slightly from 24.96x to 24.92x, representing a very small reduction in the valuation multiple being applied.

Key Takeaways

- Successful drilling and production strategies are set to boost reserves and production, driving growth in revenue and cash flow.

- Operational efficiencies and tax integration are projected to enhance net margins and reduce costs, improving cash flow and sustainability.

- Regulatory delays, cost overruns, and timing mismatches in oil production and tax impacts may strain Valeura's financial performance and cash flow visibility.

Catalysts

About Valeura Energy- Engages in the exploration, development, and production of petroleum and natural gas in Thailand and in Turkey.

- The successful infill development drilling and exploration activities, which resulted in a 250% reserve replacement ratio and an increase in 2C reserves by 140%, are likely to drive future production growth and contribute positively to future revenue.

- The Wassana Field redevelopment, expected to reach FID in early Q2 2025, could significantly increase the 2P reserves and double production upon completion, enhancing revenue and cash flow in the coming years.

- Operational efficiencies have lowered OpEx, coming in at $22.8 per barrel in Q4, and capitalized on cost-effectiveness in drilling activities. This efficiency is expected to improve net margins by reducing production costs further.

- The integration and tax consolidation of Thai III companies, accessing approximately $400 million in tax losses, will substantially decrease future tax burdens, boosting after-tax earnings and cash flow.

- The development of projects such as the low-BTU generator for waste gas power and Manora's debottlenecking project, aimed at reducing greenhouse gas emissions and operational costs, are poised to enhance net margins and contribute to environmental sustainability goals.

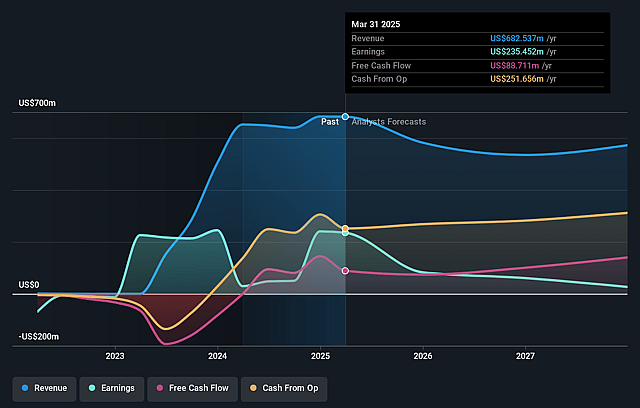

Valeura Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Valeura Energy's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will increase from 3.8% today to 10.1% in 3 years time.

- Analysts expect earnings to reach $59.1 million (and earnings per share of $0.54) by about April 2029, up from $22.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $77.6 million in earnings, and the most bearish expecting $45.0 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 25.1x on those 2029 earnings, down from 43.5x today. This future PE is greater than the current PE for the CA Oil and Gas industry at 18.6x.

- Analysts expect the number of shares outstanding to decline by 0.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.25%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Regulatory delays or changes in government policies, as noted in the approval delay for the exploration phase in Turkey, could impact the company's ability to explore and develop new fields, affecting future reserves and revenue.

- The necessity of a successful final investment decision (FID) for the Wassana redevelopment project to increase reserves and production might lead to increased financial pressure if there are delays or cost overruns, affecting future earnings.

- The potential mismatch in timing between production and lifting of oil may cause temporary fluctuations in reported quarterly revenues, which could impact short-term cash flow visibility for investors.

- Uncertainties regarding the timing and financial impact of tax payments and consolidation benefits may affect net margins and the predictability of after-tax cash flows.

- The ambition to grow through large development assets rather than focusing more on cash flow-accretive acquisitions could lead to increased capital expenditures, potentially affecting net cash flow if the production timelines are delayed or the expected returns are not realized.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CA$16.5 for Valeura Energy based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$19.0, and the most bearish reporting a price target of just CA$12.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $587.5 million, earnings will come to $59.1 million, and it would be trading on a PE ratio of 25.1x, assuming you use a discount rate of 6.3%.

- Given the current share price of CA$12.91, the analyst price target of CA$16.5 is 21.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Valeura Energy?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.