Last Update 08 Jul 26

Fair value Increased 10%AKRBP: Execution Risks On Norwegian Projects Will Restrain Future Share Returns

Aker BP’s updated analyst price target has moved from NOK 211.08 to NOK 232.48, with analysts citing adjusted fair value assumptions, higher projected revenue growth, stronger profit margins and a lower future P/E estimate as key supports for the change.

Analyst Commentary

Recent research on Aker BP reflects a mix of upgraded ratings and renewed attention to valuation, as some analysts reassess where the stock should trade relative to its earnings outlook and risk profile. While certain firms have shifted to more neutral stances, the commentary still highlights areas that cautious investors may want to monitor closely.

One recent change saw Aker BP moved to a Hold rating with a stated price target of NOK 306. This type of shift toward a more neutral view can signal that analysts see a balance between potential upside and the key risks around execution, capital allocation and the earnings multiple the stock is currently trading on.

At the same time, other research indicates that some institutions have become more constructive on Aker BP, pointing to factors that, in their view, support an improved outlook. However, these more positive views still sit alongside concerns about how much optimism is already reflected in current valuation levels and how reliably the company can deliver against expectations.

For readers, the mixed tone of recent coverage means it is particularly important to understand where analysts see vulnerabilities in the investment case and how those might affect longer term returns.

Bearish Takeaways

- Bearish analysts point to the risk that Aker BP’s valuation already prices in optimistic assumptions on growth and margins, which could limit upside if earnings or cash flow delivery is weaker than expected.

- There is caution that future changes to fair value estimates or P/E assumptions could move price targets lower if sector conditions, project timelines or cost profiles do not line up with current forecasts.

- Some bearish analysts flag execution risk around Aker BP’s project pipeline, warning that delays, budget pressure or operational setbacks could lead to cuts in earnings estimates and more muted price target revisions.

- Cautious commentary also highlights the potential for sentiment to turn if macro factors or sector specific developments reduce confidence in forward revenue and profit assumptions that underpin existing research views.

What’s in the News for Aker BP

- Aker BP reported net production of 383,600 mboepd for the second quarter of 2026, giving investors an updated data point on current operating levels. (Source: Aker BP operating results announcement)

- The company reaffirmed production guidance for 2026 in the range of 370 mboepd to 400 mboepd, outlining the volume levels management is targeting for the full year. (Source: Aker BP corporate guidance)

- Aker BP and Equinor advanced the Ringvei Vest project, agreeing on a development concept for one of the largest early phase projects on the Norwegian Continental Shelf, with approximately 240 million barrels of oil equivalent in estimated gross resources. (Source: Ringvei Vest development update)

- Aker BP and Equinor entered a wider collaboration across Ringvei Vest, Yggdrasil and Wisting, involving licence swaps and a US$23 million cash consideration, intended to align ownership interests and support coordinated development on the Norwegian Continental Shelf and adjacent UK areas. (Source: Aker BP and Equinor collaboration announcement)

- The Johan Sverdrup unit redetermination increased Aker BP’s ownership interest to 31.7163% and provides for an additional 2.2 million barrels of oil equivalent to be allocated to the company over the next two years, alongside a payment of approximately NOK 300 million before tax linked to historic investments. (Source: Johan Sverdrup redetermination announcement)

Valuation Changes for Aker BP

- Fair Value: NOK 211.08 to NOK 232.48, a higher assessed level for Aker BP’s updated valuation range.

- Discount Rate: unchanged at 6.65%, indicating no adjustment to the risk assumption used in the valuation work.

- Revenue Growth: 0.17% to 2.32%, reflecting a higher projected growth rate for revenue in the underlying model.

- Net Profit Margin: 9.22% to 13.31%, pointing to a higher expected level of profitability for Aker BP.

- Future P/E: 16.43x to 11.85x, indicating a lower valuation multiple being applied to forward earnings in the updated analysis.

Key Takeaways

- Accelerating renewable energy shifts and stricter regulations threaten Aker BP's demand outlook, cost structure, and long-term profitability.

- High capital intensity, geographic concentration, and global oil oversupply heighten risks to cash flow, revenue stability, and dividend growth.

- Low-cost operations, strong project discipline, and industry-leading sustainability initiatives position the company for resilient cash flow, growth investment, and enhanced shareholder returns.

Catalysts

About Aker BP- Explores for, develops, and produces oil and gas on the Norwegian Continental Shelf.

- Rapid acceleration in the global transition to renewable energy and electrification could undermine demand for oil and gas long before Aker BP's capital-intensive expansion projects reach peak production, resulting in persistently weaker revenue growth and potential long-term demand destruction even as new fields come online.

- Intensifying regulatory scrutiny, heightened carbon taxes, and stricter emissions compliance, especially across Europe, are likely to significantly raise ongoing operating costs and erode net margins for North Sea producers such as Aker BP, directly constraining earnings resilience in the face of tightening environmental policy.

- Aker BP's dependence on the Norwegian Continental Shelf exposes it to severe geographical concentration risk, limiting revenue diversification and exposing earnings to local operational, logistical, and regulatory setbacks, with future cash flow and dividend growth at risk if region-specific challenges materialize.

- High and escalating capital expenditure on both legacy and new developments, combined with the reality of maturing assets and field decline rates, means that return on capital and free cash flow could be squeezed over time, particularly if recent exploration success or cost containment efforts fail to consistently offset increased spending and higher breakeven levels.

- Global oil oversupply from persistent advances in shale and non-OPEC production, coupled with disruptive technologies like electric vehicle adoption, threaten long-term benchmark price stability and can compress Aker BP's realized prices, reducing top-line revenues and putting sustained pressure on profitability and cash generation even if operational execution remains strong.

Aker BP Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Aker BP compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Aker BP's revenue will grow by 2.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 5.3% today to 13.3% in 3 years time.

- The bearish analysts expect earnings to reach $1.5 billion (and earnings per share of $2.45) by about July 2029, up from $574.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $2.3 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 11.9x on those 2029 earnings, down from 35.4x today. This future PE is lower than the current PE for the GB Oil and Gas industry at 15.0x.

- The bearish analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.65%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Continued success in exploration, particularly in the Yggdrasil area and surrounding tie-backs, could add significant new resources at a low incremental cost, supporting production growth and potentially boosting revenues and long-term cash flows.

- Industry-leading low emissions intensity and an active decarbonization strategy position Aker BP favorably with regulators and ESG investors, which could help sustain lower costs of capital and stronger net margins despite broader fossil fuel divestment trends.

- Disciplined project execution, demonstrated by limited cost overruns (3% to 4% on like-for-like basis for major projects) and robust contingency planning, may mitigate inflationary pressures, reducing risks to earnings and preserving free cash flow.

- Strong operational efficiency with production costs among the lowest in the industry, combined with resilient financial health (ample liquidity and low leverage), increases the company's flexibility to invest in growth, offsetting maturity-driven declines and supporting dividend growth which positively impacts shareholder returns.

- The company's clear pathway to sustain or even increase production above 500,000 barrels per day beyond 2030, underpinned by advanced digitalization, technological improvements in exploration and drilling, and a deep reserve base, provides structural support for higher long-term revenues and stable or growing earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Aker BP is NOK232.48, which represents up to two standard deviations below the consensus price target of NOK325.81. This valuation is based on what can be assumed as the expectations of Aker BP's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK400.0, and the most bearish reporting a price target of just NOK200.0.

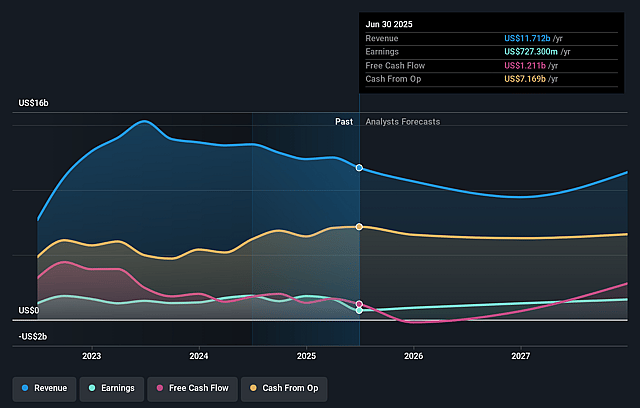

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $11.6 billion, earnings will come to $1.5 billion, and it would be trading on a PE ratio of 11.9x, assuming you use a discount rate of 6.7%.

- Given the current share price of NOK313.9, the analyst price target of NOK232.48 is 35.0% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Aker BP?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.