Last Update 07 Jun 26

VLTSA: Long Term CPPAs And New Solar Assets Will Support Returns

Analysts have kept Voltalia's fair value unchanged at €10.16 per share, with only very small tweaks to assumptions such as discount rate, revenue growth, profit margin and future P/E informing the latest price target update.

What's in the News

- Voltalia fully commissioned the Bolobedu solar farm in South Africa’s Limpopo province, a 148 megawatt project supplying around 300 gigawatt-hours per year to Richards Bay Minerals under a long term CPPA, with reported annual CO2 emissions savings of more than 237,000 tonnes and employment for around 800 local residents during construction. (Source: Key Developments)

- The company commissioned three photovoltaic power plants in the south of France, with a combined capacity of 26.9 megawatts. This includes two sites totaling 17.1 megawatts in Bouches du Rhône and a 9.8 megawatt plant in Alpes Maritimes, partly backed by a 15 year corporate power purchase agreement with CERN covering 34.3 gigawatt-hours per year. (Source: Key Developments)

- Voltalia reported first quarter 2026 production of 1,105 GWh, compared with 1,121 GWh in the same period a year earlier, and production curtailment of 113 GWh compared with 87 GWh. (Source: Key Developments)

- The company’s Annual General Meeting on May 21, 2026 approved amendments to Article 18 and to Articles 12.7 and 12.8 of the Articles of Association to align with new legal provisions and clarify wording. (Source: Key Developments)

- A Board meeting held on May 20, 2026 had on its agenda potential changes to Voltalia’s Board of Directors. (Source: Key Developments)

Valuation Changes

- Fair Value was kept unchanged at €10.16 per share, indicating no revision to the central value estimate.

- The Discount Rate edged down slightly from 8.21% to 8.14%, reflecting a small adjustment in the required return used in the model.

- Revenue Growth was held effectively steady at 8.51%, with only a very small technical tweak to the input.

- The Net Profit Margin was maintained at about 6.81%, with only a minor rounding-level adjustment.

- The future P/E was trimmed slightly from 33.0x to 32.9x, implying a marginally lower valuation multiple assumption for future earnings.

Key Takeaways

- The SPRING project and long-term PPAs aim to simplify operations and stabilize revenues, enhancing overall performance and margins.

- Strategic diversification in power generation and geographic focus on Europe could boost revenues and increase long-term earnings and EBITDA.

- Regulatory uncertainties, high leverage, and market shifts may hinder Voltalia's revenue growth, profitability, and financial stability in a competitive renewable energy landscape.

Catalysts

About Voltalia- Engages in the production and sale of energy generated by the wind, solar, hydropower, biomass, and storage plants.

- The launch of the SPRING transformation project aims to simplify Voltalia's business model, prioritize returns against growth, and consolidate geographical presence, which could enhance overall performance and lead to improved margins and earnings.

- Securing long-term, inflation-indexed PPAs with an extended lifespan of over 16 years ensures stability and predictability of revenues from energy sales, which is expected to positively affect revenue and net margins.

- The dual focus on centralized and decentralized green power generation diversifies market opportunities, potentially boosting revenues and balancing risk exposure to grid congestion, leading to higher net margins.

- The development of innovative projects, such as the storage project in Uzbekistan with a 15-year PPA, offers new revenue streams with no merchant risk, expected to enhance earnings and margins.

- Strategic geographical diversification and growth in the pipeline, with increased focus on Europe, alongside continued development and sale of high-margin projects, potentially increase long-term revenue and EBITDA.

Voltalia Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Voltalia's revenue will grow by 8.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -17.1% today to 6.8% in 3 years time.

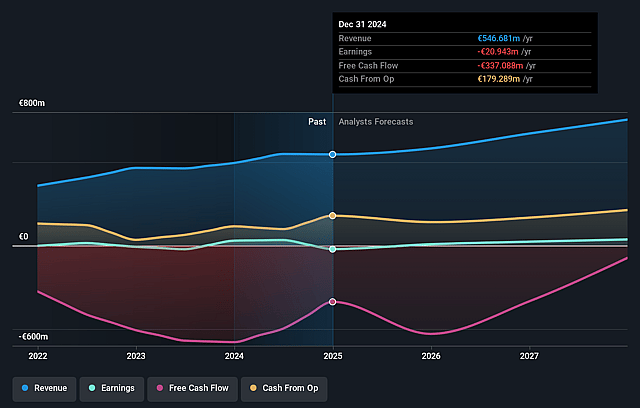

- Analysts expect earnings to reach €51.1 million (and earnings per share of €0.39) by about June 2029, up from -€100.5 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 32.9x on those 2029 earnings, up from -10.5x today. This future PE is greater than the current PE for the GB Renewable Energy industry at 10.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.14%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The competitive environment for signing new PPAs, along with the potential slower growth pace in the renewable energy market, could impact Voltalia’s revenue growth and profitability.

- The significant net loss of €21 million reported for 2024, driven by equipment supply business decline and curtailment impacts, indicates risks to net margins and overall earnings.

- Continued curtailment issues in Brazil and regulatory uncertainties could negatively affect project returns and increase the risk of impairments, thereby impacting earnings.

- High leverage with a net debt to EBITDA ratio of 9%, combined with an increased cost of debt to 6.1%, could affect cash flow and financial stability, impacting net margins.

- Merchant price exposure aversion and potential market shifts in the structure of PPAs might limit flexibility and revenue predictability, posing risks to sustained earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €10.16 for Voltalia based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €21.8, and the most bearish reporting a price target of just €7.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €751.0 million, earnings will come to €51.1 million, and it would be trading on a PE ratio of 32.9x, assuming you use a discount rate of 8.1%.

- Given the current share price of €8.06, the analyst price target of €10.16 is 20.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Voltalia?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.