Last Update 18 Jun 26

Fair value Decreased 0.12%J69U: Mall Divestment And Stable Distributions Will Support Future Upside

Analysts have nudged their fair value estimate for Frasers Centrepoint Trust slightly lower from SGD 2.60 to around SGD 2.60. This change reflects small adjustments to their discount rate, revenue growth outlook and profit margin assumptions, while future P/E expectations are kept broadly similar.

What’s in the News for Frasers Centrepoint Trust

- Frasers Centrepoint Trust reported a distribution per unit of 6.136 Singapore cents for 1HFY26, covering the six months from 1 October 2025 to 31 March 2026, according to Frasers Centrepoint Asset Management Ltd.

- The 1HFY26 distribution consists of a taxable component of 6.134 Singapore cents per unit and a tax exempt component of 0.002 Singapore cents per unit, as reported by the manager.

- Unitholders on record with The Central Depository (Pte) Limited as at 5.00pm on 5 May 2026 are entitled to the 1HFY26 distribution, which is scheduled to be paid on 29 May 2026, according to the manager.

- Frasers Centrepoint Trust is reported to be in the process of selling its White Sands shopping mall in Pasir Ris. TE Capital Partners is said to be in exclusive due diligence for a potential transaction of over SGD 470,000,000, according to The Business Times.

- The reported White Sands deal implies an exit yield of around 4.5% on a property valued at SGD 431,000,000 as at 30 September 2025. Frasers Centrepoint Trust acquired the property in 2020 for SGD 428,000,000, with Cushman & Wakefield and Savills appointed as marketing agents, according to The Business Times.

Valuation Changes for Frasers Centrepoint Trust

- Fair Value: The fair value estimate for Frasers Centrepoint Trust has edged slightly lower from SGD 2.60133 to around SGD 2.59812.

- Discount Rate: The discount rate assumption has been adjusted marginally from 7.023955% to about 7.006686168100062%.

- Revenue Growth: The revenue growth outlook now reflects a slightly larger expected decline, changing from a fall of 3.058261% to a fall of 3.0719904003005616%.

- Profit Margin: The profit margin assumption has been trimmed from 58.329615% to about 58.086809128562614%.

- Future P/E: The future P/E multiple assumption remains broadly similar, moving slightly from 24.612518x to about 24.68343981631108x.

Key Takeaways

- Strong demand for suburban retail space and favorable demographics support high occupancy, stable rental income, and consistent earnings growth.

- Focus on necessity-driven malls, active asset enhancements, and disciplined capital management provide income resilience and opportunities for future expansion.

- Heavy reliance on Singapore malls, rising costs, e-commerce disruption, and tenant health concerns threaten earnings stability and long-term income growth.

Catalysts

About Frasers Centrepoint Trust- Frasers Centrepoint Trust (“FCT”) is a leading developer-sponsored retail real estate investment trust (“REIT”) and the largest suburban retail mall owner by net lettable area in Singapore with assets under management of approximately $7.1 billion.

- The ongoing tight supply of prime suburban retail space in Singapore, combined with strong demand and limited new completions over the next 3 years, is expected to support high occupancy rates and positive rental reversions, driving future revenue and earnings growth.

- Favorable demographic trends-specifically rising population and urbanisation in Singapore-are boosting consistent shopper footfall and tenant sales, which should underpin the durability of FCT's rental income and support stable or improving net margins.

- FCT's focus on necessity-driven suburban malls, with high exposure to supermarkets and F&B tenants, ensures steady recurring revenue streams and lowers income volatility, providing resilience and visibility for future net property income and margins.

- Proactive asset enhancement initiatives (AEIs), including completed and upcoming projects like Tampines 1 and Hougang Mall, are creating tangible value through higher rental rates and returns on investment (7-8% yield on recent AEIs), which will likely translate into earnings and NAV per unit growth.

- Continued capital management discipline and moderate gearing (targeting below 40%) position FCT to seize accretive acquisition opportunities as smaller landlords exit, potentially expanding its asset base and boosting distributable income and DPU.

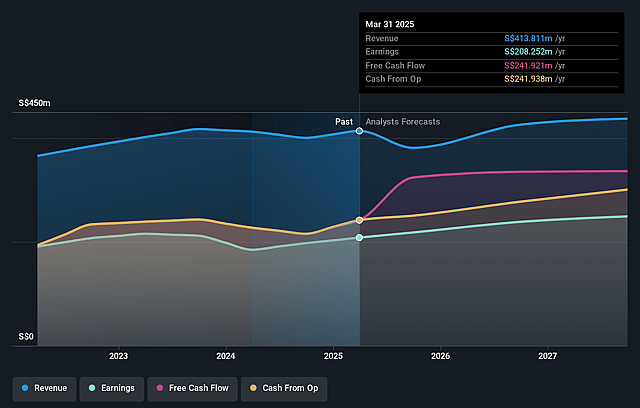

Frasers Centrepoint Trust Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Frasers Centrepoint Trust's revenue will decrease by 3.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 45.5% today to 58.1% in 3 years time.

- Analysts expect earnings to reach SGD 263.9 million (and earnings per share of SGD 0.13) by about June 2029, up from SGD 227.2 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as SGD296.0 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 24.7x on those 2029 earnings, up from 20.1x today. This future PE is greater than the current PE for the SG Retail REITs industry at 14.5x.

- Analysts expect the number of shares outstanding to grow by 0.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.01%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- FCT's portfolio remains highly concentrated in Singapore's suburban retail malls, exposing the company to localised demographic shifts, competition, and economic shocks-posing a risk to long-term revenue stability and leading to potentially volatile earnings if Singapore retail fundamentals weaken.

- The ongoing structural shift toward e-commerce and online retail channels remains a significant secular trend, as evidenced by management's need to re-purpose cinema space and introduce new tenant concepts-indicating persistent risks to footfall, occupancy, and rental income growth over time.

- Asset enhancement initiatives (AEIs) and acquisitions require substantial capital expenditure and increase leverage (post-South Wing acquisition, gearing is at 40.4%); if execution is delayed, AEIs underperform, or market conditions turn, this could erode net margins and slow distributable income growth.

- Rising operating and maintenance costs-including those related to sustainability, technology upgrades, and inflation-could weigh on net property income and compress margins, especially if rental growth or cost pass-through lags sector-wide expense escalation.

- Retail tenant health, especially for categories like cinemas and SMEs facing arrears or structural decline, introduces risk of higher default rates and vacancy; if tenant churn persists or replacement tenants secure lower rents, revenue and net operating income will face long-term pressure.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SGD2.6 for Frasers Centrepoint Trust based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SGD3.06, and the most bearish reporting a price target of just SGD2.19.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SGD454.3 million, earnings will come to SGD263.9 million, and it would be trading on a PE ratio of 24.7x, assuming you use a discount rate of 7.0%.

- Given the current share price of SGD2.24, the analyst price target of SGD2.6 is 13.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Frasers Centrepoint Trust?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.