Catalysts

About Cineplex

Cineplex operates movie theatres and location based entertainment venues, and sells cinema media advertising across Canada.

What are the underlying business or industry changes driving this perspective?

- Growing consumer appetite for premium theatrical formats, reflected in box office per patron of $13.23 and premium experiences accounting for 44.7% of box office, points to a mix shift toward higher priced tickets that can support revenue per guest and potentially lift margins over time.

- Rising contribution from international and alternative content, with international cinema at 13.6% of box office compared with 9.3% a year earlier and hits such as Demon Slayer and Punjabi films, broadens the audience base and gives Cineplex more levers to drive box office revenue and advertising demand.

- Expansion of the location based entertainment business, where Q3 revenue reached a record $34.6 million supported by three new venues and additional openings planned, offers a second growth engine that can contribute to total revenue and, as new sites mature, improve overall earnings.

- Cinema Media growth despite a softer advertising market, with Q3 revenue of $19.2 million, 6.1% higher year over year, cinema media per patron at $1.59 and segment EBITDA margin near 80%, suggests a scalable high margin revenue stream that can support overall EBITDA and cash generation.

- Sale of Cineplex Digital Media for $70 million at roughly a 10x multiple on estimated 2025 earnings, combined with a debt free $100 million credit facility and plans for share buybacks and potential debt reduction, gives Cineplex more financial flexibility to manage leverage and support future earnings per share.

Assumptions

This narrative explores a more optimistic perspective on Cineplex compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

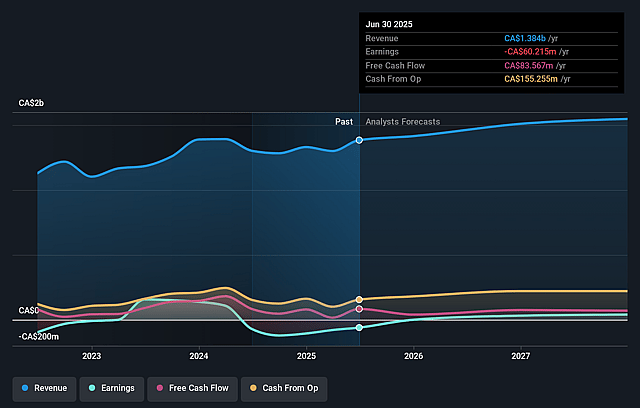

- The bullish analysts are assuming Cineplex's revenue will grow by 6.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -2.7% today to 5.9% in 3 years time.

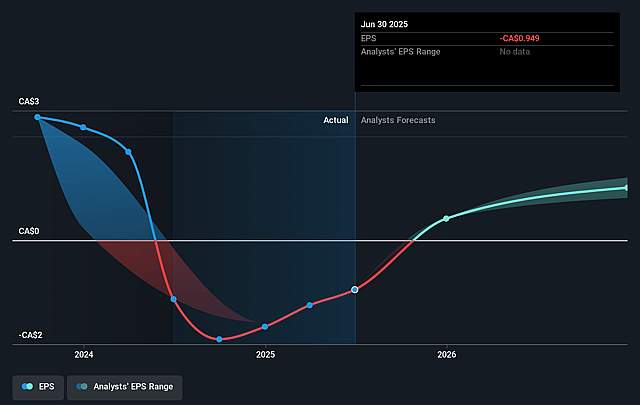

- The bullish analysts expect earnings to reach CA$94.4 million (and earnings per share of CA$1.76) by about January 2029, up from CA$-35.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 15.7x on those 2029 earnings, up from -19.3x today. This future PE is lower than the current PE for the CA Entertainment industry at 15.8x.

- The bullish analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.17%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Cineplex is still heavily tied to the theatrical release calendar, and Q3 2025 showed how a tough comparison against last year's Deadpool and Wolverine period translated into a 9.1% attendance decline and an 8.8% drop in box office revenue. Any multi year stretch with fewer breakout titles or more uneven slates could weigh on revenue and limit earnings progress.

- Location based entertainment revenue grew in Q3 2025, but same store sales declined 3.3% and same store EBITDA margin sat at 21%, while total portfolio margin was 16.7% compared with a higher level last year. If consumer pressure on discretionary spending persists, this segment could stay margin dilutive and hold back consolidated EBITDA and net income.

- The sale of Cineplex Digital Media removes an earnings contributor and concentrates the media segment on cinema advertising only. Although Cineplex Media remains the exclusive sales agent for those digital out of home networks, any long term weakness in the broader advertising market or shift in media budgets away from cinema could slow Cinema Media revenue and its near 80% EBITDA margin, which would directly affect overall cash generation and earnings.

- Promotional tactics like the $5 Labor Day offer supported attendance and were a net positive contribution in Q3 2025, but they also pulled box office per patron down by $0.32 and concession per patron down by $0.12. If Cineplex needs to rely more often on discounting to keep seats filled, that could pressure per patron revenue and keep net margins below what bullish expectations assume.

- The business still carries meaningful fixed costs and is targeting leverage of 2.5x to 3x. If box office or LBE performance falls short for several years, Cineplex could have less room to invest, less flexibility on capital returns like buybacks and less ability to lift earnings per share at the pace implied by more optimistic assumptions.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Cineplex is CA$17.0, which represents up to two standard deviations above the consensus price target of CA$13.83. This valuation is based on what can be assumed as the expectations of Cineplex's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$17.0, and the most bearish reporting a price target of just CA$11.5.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be CA$1.6 billion, earnings will come to CA$94.4 million, and it would be trading on a PE ratio of 15.7x, assuming you use a discount rate of 11.2%.

- Given the current share price of CA$10.89, the analyst price target of CA$17.0 is 35.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Cineplex?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.