Last Update 22 Jun 26

Fair value Increased 2.82%8411: Alliance With Rakuten Bank And Buybacks Will Support Measured Future Earnings Multiple

Analysts have lifted their price target for Mizuho Financial Group from about ¥7,617 to roughly ¥7,831, citing updated assumptions on revenue growth, profit margins and future P/E expectations that modestly adjust their valuation model.

What's in the News

- On May 20, Mizuho Financial Group and Rakuten Bank agreed on a capital and business alliance that includes Mizuho Bank acquiring shares in Rakuten Bank and working together on a new credit model that connects large corporate banking expertise with digital retail banking reach. Source: recent news report on the Mizuho Bank and Rakuten Bank alliance.

- The alliance with Rakuten Bank also covers collaboration on project finance, fund investments and operational efficiency in housing loans, tying Mizuho Financial Group more closely to Rakuten's broader FinTech reorganization. Source: recent news report on the Mizuho Bank and Rakuten Bank alliance.

- Mizuho Financial Group received a shareholder proposal to amend its Articles of Incorporation regarding risks tied to potential consolidation of Orient Corporation, then later received notice that the proposal was withdrawn after Mizuho Bank's shareholding ratio in Orient Corporation changed. Source: company press releases dated May 15 and May 28, 2026.

- The Board of Directors of Mizuho Financial Group met on May 28, 2026, and agreed to the withdrawal of the Orient Corporation related shareholder proposal and resolved to partially amend the matters to be submitted at the 24th Annual General Meeting of Shareholders scheduled for June 26, 2026. Source: company Board meeting disclosure.

- Mizuho Financial Group announced a share repurchase program of up to 25,000,000 shares, or 1.03% of issued share capital, for ¥100,000 million, with repurchased shares to be cancelled and the program set to expire on August 31, 2026. Source: company buyback announcement dated May 15, 2026.

Valuation Changes

- Fair Value: the updated estimate for Mizuho Financial Group has moved from about ¥7,616.82 to roughly ¥7,831.36, a small upward adjustment in the model output.

- Discount Rate: the discount rate has edged up slightly from 5.95% to about 5.96%, reflecting a minimal change in the cost of capital assumption.

- Revenue Growth: projected revenue growth has risen from about 1.38% to roughly 2.82%, indicating a higher growth assumption in the updated model for future ¥ revenue.

- Net Profit Margin: the profit margin assumption has eased from around 34.37% to about 32.77%, pointing to a modestly lower expected level of profitability on future ¥ earnings.

- Future P/E: the assumed future P/E multiple has shifted from about 13.01x to roughly 13.45x, a small increase in the earnings multiple applied to Mizuho Financial Group.

Key Takeaways

- Strategic acquisitions, partnerships, and cost-cutting initiatives aim to enhance competitive edge, improve efficiency, and expand revenue streams for Mizuho Financial Group.

- Diversifying revenue sources and enhancing shareholder returns through investments and buybacks could stabilize growth and elevate stock valuation.

- Operational costs and governance expenses could rise, while integration risks and domestic transaction dependence may affect revenue stability and net margins.

Catalysts

About Mizuho Financial Group- Engages in banking, trust, securities, and other businesses related to financial services in Japan, the Americas, Europe, Asia/Oceania, and internationally.

- Mizuho Financial Group is focused on growing its assets under management (AUM) and expanding product lines, which should enhance their revenue streams from wealth management and consulting services, potentially boosting future revenues.

- The strategic acquisitions and collaborations, such as those with Greenhill and Rakuten Securities, are expected to create new synergies and enhance the Group's competitive edge, leading to increased revenues and improved earnings.

- Cost reduction initiatives, alongside the transition to a new HR framework, are intended to improve operational efficiency and net margins, allowing for potential margin expansion as expenses are controlled.

- The diversification of revenue sources beyond traditional banking operations to include sales and trading, alongside developments in the overseas market, is intended to stabilize and grow revenues, reducing dependency on interest income and improving earnings predictability.

- Mizuho's strategy of enhancing shareholder returns through disciplined growth investments and share buybacks aims to improve earnings per share (EPS) and potentially elevate the stock's valuation relative to book value.

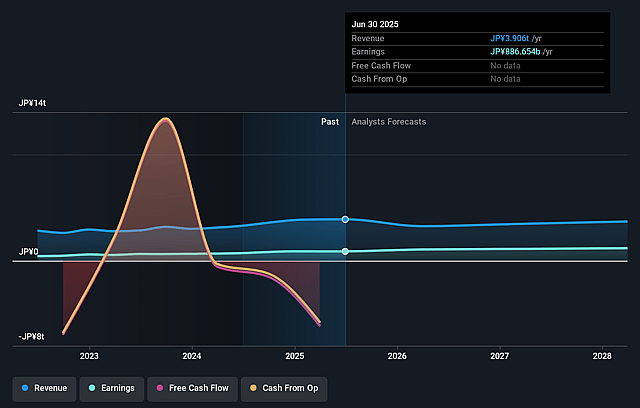

Mizuho Financial Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Mizuho Financial Group's revenue will grow by 2.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 28.4% today to 32.8% in 3 years time.

- Analysts expect earnings to reach ¥1568.3 billion (and earnings per share of ¥678.81) by about June 2029, up from ¥1248.6 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.5x on those 2029 earnings, down from 15.4x today. This future PE is lower than the current PE for the US Banks industry at 14.1x.

- Analysts expect the number of shares outstanding to decline by 2.43% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.96%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The environment surrounding the company is described as difficult, requiring significant infrastructure strengthening and efficiency improvements, which may increase operational costs and impact net margins.

- Rising expenses related to governance, infrastructure updates, and necessary investments in human capital due to increasing wages are highlighted, potentially affecting earnings and profitability.

- Integration and collaboration with entities such as Rakuten and Greenhill present potential execution risks, and challenges in aligning cultures or operational systems could disrupt revenue stability and growth.

- The dependence on large transactions in the domestic market implies potential volatility in revenue during economic downturns or changes in client needs, affecting net business profits.

- There is mention of many challenges in the asset and wealth management sector, suggesting potential shortfalls in consulting capabilities or competitive positioning, which could negatively impact revenue from these services.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ¥7831.36 for Mizuho Financial Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥9530.0, and the most bearish reporting a price target of just ¥4650.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ¥4785.5 billion, earnings will come to ¥1568.3 billion, and it would be trading on a PE ratio of 13.5x, assuming you use a discount rate of 6.0%.

- Given the current share price of ¥7884.0, the analyst price target of ¥7831.36 is 0.7% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Mizuho Financial Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.