Last Update 22 Jun 26

1: Supermarket Merger Talks Will Drive Future Upside Potential

CK Hutchison Holdings' latest narrative-based fair value estimate remains steady at HK$81.59, with analysts pointing to only marginal model adjustments to the discount rate, revenue growth, profit margin and future P/E assumptions to support an unchanged price target outlook.

What's in the News for CK Hutchison Holdings

- CK Hutchison Holdings and Jardine Matheson Holdings are reported to be in talks to merge their Hong Kong supermarket divisions, according to people familiar with the matter, with discussions involving DFI Retail Group and CK Hutchison’s ParknShop chain. Source: Financial Times, Reuters, April 17, 2026.

- The talks around a potential supermarket merger are described as ongoing, with no deal reported as imminent and the parties either declining to comment or describing the situation as speculation or rumours. Source: Reuters.

- CK Hutchison Holdings has called a special or extraordinary shareholders meeting for April 27, 2026, at 16:15 China Standard Time in Hong Kong to seek approval for transactions under a Share Purchase Agreement.

- The shareholder meeting agenda includes approval for the disposal of CKI Sub’s sale shares and CKI Sub’s shareholder debt instruments, along with related actions by CK Hutchison Holdings and its subsidiaries.

Valuation Changes

- Fair Value: HK$81.59 remains unchanged, and the narrative-based estimate is steady compared with the latest update.

- Discount Rate: 9.71% in the earlier narrative has shifted very slightly to 9.72% in the updated model.

- Revenue Growth: HK$ revenue growth assumption is essentially unchanged at 22.69% in both the narrative and updated figures.

- Net Profit Margin: HK$ net profit margin assumption remains effectively stable, moving only fractionally from 5.48% to 5.48% in the updated input.

- Future P/E: The forward P/E assumption edges only marginally higher, from about 14.57x to 14.57x in the latest update.

Key Takeaways

- The merger-driven telecom synergies and ongoing retail and ports expansion are expected to enhance margins, recurring earnings, and revenue stability across core divisions.

- Robust financial flexibility and sustainability initiatives position CK Hutchison to capitalize on infrastructure growth and secure steady, long-term returns.

- Heavy reliance on non-recurring gains, weak retail in China, telecom margin pressure, asset underperformance, and complex regulation pose risks to sustainable growth and profitability.

Catalysts

About CK Hutchison Holdings- An investment holding company, primarily operates in ports and related services, retail, infrastructure, and telecommunications businesses in Hong Kong, Mainland China, Europe, Canada, Asia, Australia, and internationally.

- The successful merger of 3 UK and Vodafone UK, along with the broader ongoing review across European telecom operations, is expected to drive substantial operating and capital expense synergies (targeting GBP 700 million a year at run-rate within five years), enhancing recurring net margins and group earnings.

- Sustained investment and efficiency-driven growth in the Ports division, including expanded facilities in key geographies and increased storage income, position the company to benefit from global trade resilience and supply chain optimization-supporting higher revenue and stable cash flows.

- Strategic expansion and modernization of the group's retail arm (notably A.S. Watson's store portfolio and loyalty program development, plus omni-channel/dark store initiatives), are anticipated to drive same-store sales growth and operational leverage, contributing to higher revenue and sustainable bottom-line growth.

- CK Hutchison's strong balance sheet post-merger (with significant liquidity and a lower net debt ratio) increases management's flexibility to pursue value-accretive investments in infrastructure and regulated utilities, sectors poised for growth as urbanization and global infrastructure needs rise-potentially boosting returns on capital and net margins.

- The group's proactive sustainability and decarbonization investments, such as green bonds and operational emissions reductions, may lift the value of its regulated infrastructure assets and secure favorable regulatory returns, creating visible, stable earnings streams over the long term.

CK Hutchison Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

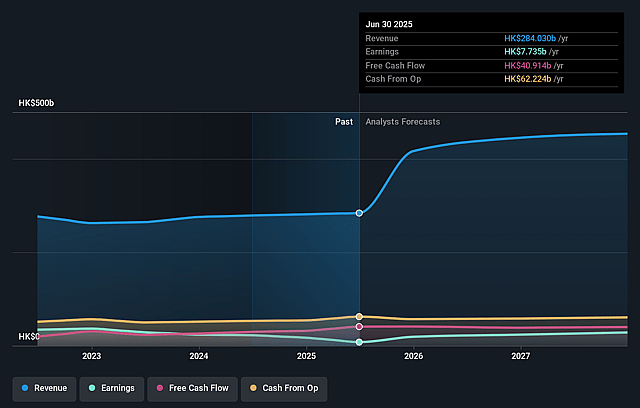

- Analysts are assuming CK Hutchison Holdings's revenue will grow by 22.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.2% today to 5.5% in 3 years time.

- Analysts expect earnings to reach HK$28.3 billion (and earnings per share of HK$7.54) by about June 2029, up from HK$11.8 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as HK$34.9 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.6x on those 2029 earnings, down from 22.2x today. This future PE is greater than the current PE for the HK Industrials industry at 8.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.72%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- CK Hutchison's earnings in the first half were significantly bolstered by favorable foreign exchange movements and non-recurring gains (e.g., Treasury gains, asset disposals), suggesting that the strong net earnings and free cash flow may not be sustainable in future periods if currency moves reverse or noncore gains are not repeated (impact: risk to underlying revenue and net earnings growth).

- The Health & Beauty retail business in Mainland China is facing persistent pressure from subdued consumer spending, increased competition, and margin erosion due to the transition to lower-margin online/delivery channels; management's actions are yet to show sustainable turnaround, posing a long-term risk of declining profitability in a key growth market (impact: risk to group revenue growth and net margins).

- CK Hutchison's European telecom operations, while posting headline growth, have been heavily dependent on one-off treasury gains, with structural challenges such as price wars (notably in Austria) and ongoing heavy capex requirements, indicating medium-term pressure on margins and limited earnings growth in mature, competitive markets (impact: risk to recurring EBITDA and long-term cash flows).

- The conglomerate's Finance & Investment segment experienced underperformance from major assets (e.g., Cenovus Energy, TPG Australia, Marionnaud), reflecting vulnerability to commodity prices, FX shifts, and operational setbacks; this underscores the risk that diversification across disparate industries may dilute management focus and exacerbate persistent structural discounts in valuation (impact: potential drag on group net earnings and shareholder returns).

- Navigating highly regulated infrastructure, utility, and telecom sectors in multiple jurisdictions exposes CK Hutchison to ongoing regulatory and political risks (e.g., required approvals for major transactions, water utility scrutiny in the UK, changing rules impacting pharma in China/US); tightening compliance, changing regulatory resets, and stakeholder activism may increase costs, delay strategic action, or squeeze returns (impact: potential margin compression and dampened revenue growth).

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of HK$81.59 for CK Hutchison Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of HK$102.0, and the most bearish reporting a price target of just HK$74.6.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be HK$517.2 billion, earnings will come to HK$28.3 billion, and it would be trading on a PE ratio of 14.6x, assuming you use a discount rate of 9.7%.

- Given the current share price of HK$68.5, the analyst price target of HK$81.59 is 16.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on CK Hutchison Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.