Last Update 20 May 26

Fair value Increased 4.68%UMAC: Drone Dominance Program And Supercycle Tailwinds Will Support Future Upside

Analysts have nudged their fair value estimate for Unusual Machines higher from $24.20 to about $25.33, citing stronger Q1 revenue, higher Street expectations, and potential demand from U.S. drone programs reflected in recent $22 and $25 price targets.

Analyst Commentary

Recent research points to a more optimistic stance on Unusual Machines, with bullish analysts framing the company as a potential beneficiary of U.S. drone programs and regulatory shifts that favor non China-sourced components.

Bullish Takeaways

- Bullish analysts view Unusual Machines as a key supplier candidate for large U.S. drone initiatives, including a cited US$1b Drone Dominance program, which they see as supportive of the stock's growth narrative.

- The better than expected Q1 revenue is cited as evidence that the company is executing against demand tied to what some call a U.S. drone supercycle, which they link to their higher price targets.

- Some research points to Unusual Machines as a diversified supplier and low cost producer, which bullish analysts argue could help the company compete effectively for component share and support long term revenue visibility.

- Certain bullish analysts reference a potential path to a US$100m revenue run rate by 2027, and use that framework to justify higher valuation assumptions and increased conviction in the stock's upside case.

Bearish Takeaways

- Expectations around a US$1b Drone Dominance program and a U.S. drone supercycle create a high bar, and bearish analysts would likely argue that any delays or scale back in these programs could pressure growth assumptions and fair value estimates.

- The reference to a US$100m revenue run rate by 2027 is a specific target, and if execution or market share gains fall short, valuation multiples implied by current price targets may look demanding.

- Reliance on regulatory exclusion of China-made parts is a key part of the bullish thesis, which leaves the story exposed to potential regulatory changes or sourcing workarounds that could cap the addressable opportunity.

- With higher Street expectations cited by bullish analysts, any future revenue outcomes that do not match this more optimistic setup could trigger estimate revisions that work against the stock's current pricing.

What’s in the News

- Unusual Machines placed approximately US$75 million of inventory orders with U.S. suppliers after raising about US$150 million to support materials, long lead items, and supply chain readiness across its drone component lines, citing clearer demand signals from programs such as the Department of War’s Drone Dominance initiative (company press release).

- The company completed a follow on equity offering of common stock, raising about US$150 million by offering 8,823,529 shares at US$17 per share, with a US$1.19 discount per share (company filing).

- Common stock and certain stock options held by executive officers, directors, and other holders are subject to a lock up agreement that runs from 23 March 2026 to 23 May 2026, limiting sales and transfers of these securities during that period (company agreement).

- Lantronix and Unusual Machines entered into a collaboration to develop next generation autonomous drone components that combine edge AI compute with flight control systems, with joint development starting immediately and initial demonstrations targeted over the next 12 months (company announcement).

- Unusual Machines was added to the S&P Technology Hardware Select Industry Index, bringing the stock into a defined industry benchmark (index announcement).

Valuation Changes

- Fair Value: Adjusted higher from $24.20 to about $25.33, representing a modest upward move in the valuation anchor used in the analysis.

- Discount Rate: Increased slightly from 8.29% to about 8.78%, indicating a somewhat higher required return being applied to future cash flows.

- Revenue Growth: The assumed long-term revenue growth rate was reduced from about 135.06% to about 93.14%, reflecting more measured expectations for the pace of future dollar revenue expansion.

- Net Profit Margin: Lowered from about 8.26% to about 7.01%, signaling a more conservative view on future profitability levels.

- Future P/E: Increased from about 120.21x to about 217.13x, suggesting a higher multiple being applied to expected future earnings in the updated framework.

Key Takeaways

- Growing government investment and policy changes in the U.S. drone sector will drive rising demand, with Unusual Machines well-placed to capitalize through new contracts and scaled domestic production.

- Focus on advanced manufacturing, acquisition opportunities, and higher-margin enterprise and government sales positions the company for sustainable margin expansion and long-term growth beyond core drone markets.

- Heavy dependence on volatile government demand and expansion amid regulatory, operational, and supply chain risks threaten both revenue stability and sustained profitability.

Catalysts

About Unusual Machines- Engages in the commercial drone industry.

- Significant government policy changes and increasing U.S. federal investment in drone technology are set to unlock material new demand for domestically sourced drone components; Unusual Machines' expectation of imminent and sizable government orders-including multiple customers vying for contracts like the $500 million PBAS program-positions the company to capture a large share of a rapidly expanding market, which is likely to drive sequential revenue growth over the next several quarters.

- The buildout of new domestic manufacturing capacity for motors and headsets, alongside the ability to scale production to tens of thousands of units monthly with further ramp potential, will enable Unusual Machines to quickly fulfill large, near-term orders and provide reliable, onshore supply to B2B and government customers, supporting both revenue acceleration and gross margin expansion as supply chains become more efficient.

- The accelerating adoption of automation, robotics, and IoT-combined with the explosion of the U.S. drone market and increased demand for advanced, NDAA-compliant components-expands Unusual Machines' long-term addressable market beyond just drones to broader smart hardware and embedded electronics, positioning the company for durable, above-market revenue growth well into the future.

- A strengthened balance sheet, with over $80 million in cash and no debt, allows Unusual Machines to aggressively pursue strategic acquisitions, vertical integration, and investments in production scaling and proprietary IP-each of which has the potential to improve net margins and enhance earnings growth through both operational leverage and increased differentiation versus lower-cost commodity competitors.

- The company's proactive move toward U.S.-based, tariff-advantaged production, combined with a focus on higher-margin enterprise and government sales (with enterprise already exceeding 30% of sales and a long-term target of 50%+), is expected to boost blended gross margins (targeting 35-50%) and shorten the path to cash flow positivity in 2026, positively impacting net margins and earnings.

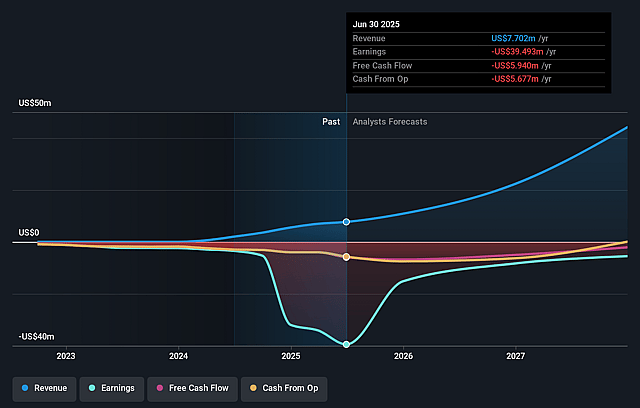

Unusual Machines Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Unusual Machines's revenue will grow by 93.1% annually over the next 3 years.

- Analysts are not forecasting that Unusual Machines will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Unusual Machines's profit margin will increase from -32.7% to the average US Electronic industry of 7.0% in 3 years.

- If Unusual Machines's profit margin were to converge on the industry average, you could expect earnings to reach $8.7 million (and earnings per share of $0.15) by about May 2029, up from -$5.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $27.2 million in earnings, and the most bearish expecting $-14.8 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 219.2x on those 2029 earnings, up from -115.6x today. This future PE is greater than the current PE for the US Electronic industry at 30.1x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.78%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Unusual Machines' significant revenue growth and scale-up plans are heavily dependent on large and rapid increases in U.S. government orders, which creates risk if policy priorities or budget allocations change, leading to volatile or disappointing revenue realization.

- The company's aggressive expansion-including factory build-outs, new product lines, and workforce scaling-poses execution risks relating to operational efficiency, quality control in new manufacturing lines, and the ability to realize planned margin improvements, which may weigh on both net margins and earnings if poorly managed.

- The current strength in gross margins is partly attributed to tariffs on imported products, but increasing regulatory volatility, ongoing tariff policy changes, and potential shifts in trade relations may either pressure input costs or erode Unusual Machines' price competitiveness, directly impacting margins and profitability.

- A reliance on a handful of government-driven projects and a primarily domestic customer base heightens revenue concentration risk; failure to win key contracts or delays in government purchasing processes could cause significant earnings swings and impair revenue stability.

- The rapid pace of technological change in the drone and electronics sector, combined with supply chain vulnerabilities (e.g., 6-month lead times on magnets), exposes Unusual Machines to risks of inventory obsolescence and potential cost spikes, possibly requiring high ongoing R&D investment and reducing both short

- and long-term profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $25.33 for Unusual Machines based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $30.0, and the most bearish reporting a price target of just $22.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $124.3 million, earnings will come to $8.7 million, and it would be trading on a PE ratio of 219.2x, assuming you use a discount rate of 8.8%.

- Given the current share price of $13.66, the analyst price target of $25.33 is 46.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Unusual Machines?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.