Last Update 17 Apr 26

Fair value Increased 18%WULF: AI Compute Pivot And Contracted Power Portfolio Will Drive Future Upside

Analysts have lifted the TeraWulf fair value estimate from about $22.10 to roughly $26.17, reflecting higher modeled revenue growth, a stronger profit margin profile, and updated P/E assumptions that incorporate recent price target increases across several research firms.

Analyst Commentary

Recent Street research around TeraWulf reflects a mix of optimism about the company’s repositioning and some caution around execution and capital needs, which feeds directly into the updated fair value estimate.

Bullish Takeaways

- Bullish analysts are lifting price targets into the low to high US$20s, which supports the higher modeled fair value and suggests confidence in how TeraWulf’s fundamentals line up with current P/E assumptions.

- Several research notes describe TeraWulf as well positioned as a former Bitcoin miner pivoting into the AI and high performance computing space, tying the company’s power expertise and 2.2 GW portfolio to potential long term growth drivers.

- Commentary highlights the transition to HPC as gaining momentum, with some analysts framing recent results as a temporary drag while the business mix shifts, rather than a signal of structural weakness.

- Where analysts reference recent share price pullbacks from the February 25 52 week high, they often view the reset as making the risk reward more appealing relative to their revised targets.

Bearish Takeaways

- Some research trims EBITDA estimates to reflect higher spending and the accounting impact of the Abernathy joint venture, which could pressure near term profitability relative to earlier expectations.

- Cautious analysts point to higher operating expenses and the shift away from Bitcoin mining as weighing on recent results, underlining execution risk as the company moves further into HPC.

- There is concern that investors may be applying very conservative assumptions to TeraWulf’s current lease value and 2026 lease signings, which could limit how quickly valuation multiples rerate.

- One set of views also flags the expectation that TeraWulf exits mining by year end, which concentrates the story on HPC success and leaves less room for the legacy business to offset any hiccups in the transition.

What's in the News

- TeraWulf filed a follow-on equity offering of up to US$800 million in common stock, and subsequently completed a separate follow-on equity offering of US$900.6 million, issuing 47,400,000 shares at US$19 with a US$0.475 per share discount.

- The company issued guidance for first quarter 2026, with revenue expected in a range of US$30 million to US$35 million.

- Lock-up agreements are in place for 435,381,960 common shares, certain restricted stock units, and certain warrants, with the lock-up period running from April 14, 2026 to May 15, 2026.

- TeraWulf completed its existing buyback program, repurchasing a total of 24,468,750 shares for US$151.36 million, representing 6.38% of the company under the authorization announced on October 23, 2024.

- Media coverage around U.S. crypto regulation, including a stalled crypto bill in Congress and upcoming White House meetings with banks and crypto firms, continues to reference TeraWulf alongside other publicly traded crypto-related companies as part of the broader sector under discussion (Reuters, WSJ).

Valuation Changes

- Fair Value: The modeled fair value estimate has risen from about $22.10 to roughly $26.17, reflecting updated assumptions across the key inputs.

- Discount Rate: The discount rate has increased from 8.98% to about 10.01%, indicating a higher required return in the updated framework.

- Revenue Growth: Revenue growth assumptions have moved from roughly 83.71% to about 93.23%, pointing to a higher expected top line expansion in the model.

- Net Profit Margin: The net profit margin input has shifted from about 3.19% to roughly 11.39%, a sizable change in the profitability profile used in the valuation.

- Future P/E: The future P/E multiple has been reduced from a very large 441.68x to about 130.62x, bringing the valuation multiple closer to levels more commonly used for high growth names.

Key Takeaways

- Transition to diversified digital infrastructure with major institutional backing reduces reliance on bitcoin price, boosting revenue stability and supporting margin growth.

- Expansion of sustainable, regulatory-compliant infrastructure positions the company to meet rising enterprise demand, drive new revenue streams, and achieve operational efficiency.

- Aggressive diversification into AI and HPC hosting exposes TeraWulf to rising costs, tenant risks, and operational challenges that threaten margin stability and long-term financial health.

Catalysts

About TeraWulf- Operates as a digital asset technology company in the United States.

- TeraWulf's recent multi-billion-dollar, multi-year hyperscale hosting agreements (e.g., with Fluidstack and Google), mark a significant shift from a pure bitcoin mining model toward diversified, contracted revenue streams in high-demand digital infrastructure-this underpins higher revenue visibility and insulates earnings from bitcoin price volatility.

- Long-term partnerships and investments from marquee players (Google's $1.8B lease backstop and equity stake) signal institutional validation, enhance creditworthiness, and are likely to lower WULF's future cost of capital, directly supporting margin expansion and accelerated infrastructure growth.

- Rapid expansion of zero-carbon, high-capacity digital infrastructure (Lake Mariner and Cayuga) positions TeraWulf to capture rising enterprise demand for sustainable, regulatory-compliant compute, supporting long-term revenue and improved net margins as regulatory and ESG pressures rise globally.

- Proven operational track record (on-time, on-budget delivery, experienced team, long-standing contractor relationships) de-risks future capacity scale-up and enables disciplined cost management, supporting sustained margin improvement and higher EBITDA.

- Growing momentum for institutional and enterprise digital asset adoption, coupled with TeraWulf's expansion into grid-interactive, renewable-powered data centers, positions the company to benefit from both higher transaction volumes and new ancillary revenue streams, enhancing long-term earnings stability and upside.

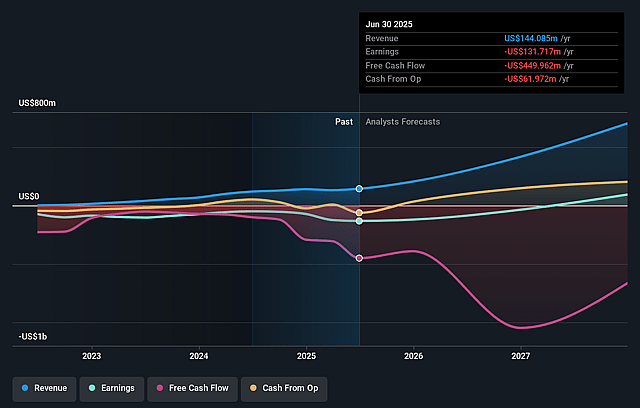

TeraWulf Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming TeraWulf's revenue will grow by 93.2% annually over the next 3 years.

- Analysts are not forecasting that TeraWulf will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate TeraWulf's profit margin will increase from -392.6% to the average US Software industry of 11.4% in 3 years.

- If TeraWulf's profit margin were to converge on the industry average, you could expect earnings to reach $138.5 million (and earnings per share of $0.27) by about April 2029, up from -$661.4 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 130.7x on those 2029 earnings, up from -14.1x today. This future PE is greater than the current PE for the US Software industry at 29.1x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.01%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- TeraWulf's aggressive expansion into High Performance Computing (HPC) and AI data center hosting (e.g., the Fluidstack deal and Cayuga site development) requires substantial capital expenditures and increases debt exposure, introducing long-term risks to free cash flow, net margins, and balance sheet stability-especially if demand or execution timelines falter.

- The company's revenue stream is rapidly diversifying away from its legacy crypto mining business, but longer-term returns are highly dependent on maintaining "transformative" leases with newer tenants (e.g., Fluidstack) whose own financial stability, customer base, and AI sector demand are not fully transparent, creating potential risks to recurring revenue and earnings should counterparties struggle or market conditions shift.

- Although Google's backstop reduces near-term counterparty risk, its credit support for the Fluidstack lease declines over time and is tied to equity dilution, potentially impacting future shareholder value and exposing TeraWulf to ongoing concentration risks if similar structures are used in future expansions.

- TeraWulf faces escalating operational costs (e.g., labor, custom buildouts, supply chain constraints) as evidenced by higher CapEx on Fluidstack versus Core42 and increasing SG&A guidance, posing a risk to gross and net margins unless efficiencies scale materially or future contracts continue to deliver very high site-level net operating income.

- The company's long-term growth relies on sustained strong demand in both the AI infrastructure and crypto mining sectors, both of which could be adversely affected by regulatory changes (e.g., U.S. energy/environmental policy, digital asset legislation) or technology disruptions, leading to potential declines in revenue, EBITDA, or asset utilization if sectoral sentiment or policy support weakens.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $26.17 for TeraWulf based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $37.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.2 billion, earnings will come to $138.5 million, and it would be trading on a PE ratio of 130.7x, assuming you use a discount rate of 10.0%.

- Given the current share price of $19.31, the analyst price target of $26.17 is 26.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on TeraWulf?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.