Last Update 05 Jun 26

Fair value Increased 7.31%SAIC: Future Cash Flows Will Reflect Federal Contract Mix And Margin Risks

The analyst price target for Science Applications International has been raised from $109.78 to $117.80, as analysts respond to recent Q1 earnings beats, higher Street targets in the $110 to $137 range, and views that updated earnings guidance appears achievable despite flagged risks in certain contracts and segment margins.

Analyst Commentary

Recent Street research on Science Applications International reflects a mix of optimism on execution and earnings, alongside caution around contract concentration and margin sustainability. Price targets now span roughly US$95 to US$137, with ratings clustered around Neutral or Hold and a smaller group at Buy.

Bullish Takeaways

- Bullish analysts view the recent Q1 earnings beat and "beat and raise" quarter as evidence that management is executing against guidance. This supports higher valuation targets in the US$119 to US$137 range.

- Some see the upgraded earnings guidance as achievable. They point to remaining performance obligations and what they describe as more normal market conditions as support for continued delivery on current expectations.

- Citi and Stifel, which keep Buy ratings with targets at US$132 and US$137, highlight that the strong Q1 print and earnings‑focused guidance support what they describe as a more constructive view on earnings power, even if revenue expectations remain measured.

- One firm notes that SAIC should trade in line with sector averages when considering organic growth, margins, leverage and recompete performance. This can be read as supportive if the stock trades at a discount to peers.

Bearish Takeaways

- Bearish analysts point to risks that Q1 Civil segment margins may not be sustainable. They suggest this could limit upside to earnings and justify more cautious targets such as US$95 to US$110 and Hold or Neutral ratings.

- Several reports flag contract related overhangs, including the Evolve recompete in the second half of FY27 and delayed RITS contract roll off. They note these could affect future revenue visibility and put pressure on valuation multiples if outcomes are unfavorable.

- Earlier research that cut targets, including from JPMorgan, Citi, Jefferies and Truist, underscores concerns around prior quarter results and the longer term outlook. This indicates that sentiment has not fully shifted to outright bullish despite the Q1 beat.

- One Hold rated firm emphasizes potential risk from the Vanguard program and suggests SAIC should only trade in line with the group. This implies limited relative upside if execution or recompete performance disappoints.

What's in the News

- SAIC reported Q1 fiscal 2026 results that beat revenue and earnings estimates, with a 1.5% year over year revenue increase and a 41.7% adjusted EPS beat. The company raised full year adjusted EPS guidance to US$10 at the midpoint while keeping revenue guidance at US$7.1b, and the stock moved to a 52 week high with gains in the 12.4% to 14.8% range. Management highlighted margin expansion, portfolio realignment toward higher margin, mission critical work, and expectations around potential M&A and index inclusion as supporting factors (source: recent earnings coverage, June 1, 2026).

- Q1 fiscal 2027 results showed revenue of US$1.91b and adjusted diluted EPS of US$3.23, as well as a record adjusted EBITDA margin of 11.6% versus 8.4% previously. The company raised full year guidance for adjusted EBITDA, adjusted EBITDA margin, and adjusted diluted EPS to US$9.90 to US$10.10 per share while maintaining revenue guidance of US$7.0b to US$7.2b, with growth led by the Defense and Intelligence segment and supported by a backlog of about US$22.9b (source: Q1 FY2027 earnings reports, June 10, 2024).

- SAIC is reshaping its business mix by consolidating operating groups from five to three. The company is focusing on mission critical and engineering offerings and reducing emphasis on commoditized enterprise IT, while using AI tools to support contract profitability and delivery across major federal programs (source: Q1 FY2027 earnings reports, June 10, 2024).

- The U.S. Navy’s Naval Undersea Warfare Center in Newport, Rhode Island awarded SAIC a follow on US$50.6m task order to continue work on torpedo defense systems such as the AN/SLQ-25 Nixie and related technologies. SAIC will use digital engineering, modeling, and simulation to support system upgrades and vessel survivability (sources: Navy contract news June 3, 2026 and client announcement filing).

- SAIC continues to return capital to shareholders, completing the repurchase of 6,569,338 shares, or 14.27% of the company, for US$677.98m between December 5, 2024 and May 1, 2026, alongside an ongoing dividend of US$0.37 per share mentioned in earlier earnings coverage (sources: buyback tranche updates and Q1 FY2027 earnings reports).

Valuation Changes

- Fair Value: Updated estimate has risen from $109.78 to $117.80, a gain of about 7.3%.

- Discount Rate: Assumed discount rate has edged down from 8.54% to about 8.42%, indicating a slightly lower required return in the model.

- Revenue Growth: Long term revenue growth assumption has shifted from 33.71% to a decline of about 1.14%, signaling a much more cautious stance on future revenue expansion.

- Net Profit Margin: Projected net profit margin has eased from 5.17% to about 5.05%, a small reduction in expected profitability per dollar of revenue.

- Future P/E: Assumed future P/E multiple has moved up from 12.59x to about 13.88x, implying a higher valuation multiple applied to projected earnings.

Key Takeaways

- Ongoing investments in artificial intelligence and cost controls are expected to boost margins and cash flow despite a challenging revenue environment.

- Strategic positioning in digital modernization and government-focused solutions aligns SAIC for stable, long-term growth amid evolving federal priorities.

- Increased government scrutiny, budget uncertainty, and industry shifts threaten SAIC's growth, margins, and long-term relevance amid rising competition and reduced demand for traditional IT services.

Catalysts

About Science Applications International- Provides technical, engineering, and enterprise information technology (IT) services in the United States.

- Progress in operational efficiency through enterprise-wide adoption of artificial intelligence and automation is expected to drive incremental margin improvement, even in a restrained revenue environment, supporting higher net margins and free cash flow.

- The company's strategic focus on differentiated, high-growth capabilities in areas such as mission integration, digital transformation, and advanced IT modernization positions SAIC to benefit from the government's ongoing push to update legacy systems, likely accelerating top-line growth as procurement normalizes.

- A robust pipeline and strong book-to-bill ratios, along with sustained win rates in recompetes and pending award backlogs, provide significant building blocks for revenue recovery and long-term expansion once current government funding delays and efficiency initiatives subside.

- Increasing activity in defense, homeland security, missile defense, and space-driven by geopolitical uncertainty and elevated federal spending priorities-aligns well with SAIC's current solution portfolio, potentially leading to larger, higher-value contracts and stable revenue growth over the next few years.

- Targeted investments in cost control and operational flexibility are enabling SAIC to mitigate near-term revenue compression, while simultaneously preserving the ability to pursue capability-focused M&A and R&D, supporting future earnings and long-term shareholder value through improved capital allocation.

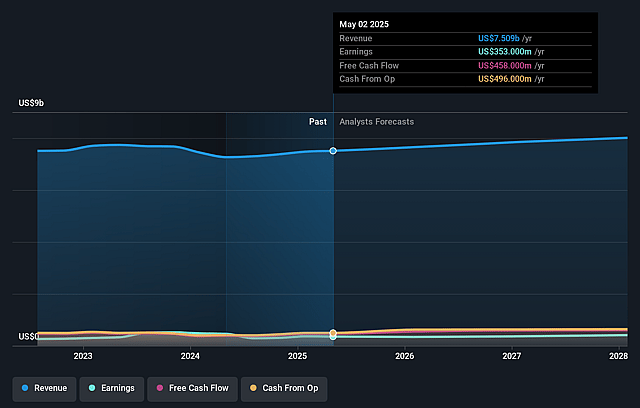

Science Applications International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Science Applications International's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will shrink from 5.6% today to 5.0% in 3 years time.

- Analysts expect earnings to reach $367.7 million (and earnings per share of $10.58) by about June 2029, down from $405.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.9x on those 2029 earnings, up from 12.2x today. This future PE is lower than the current PE for the US Professional Services industry at 19.3x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.42%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Increased government scrutiny on spending, efforts to drive efficiency, and budget uncertainty-especially in key areas like Army transformation and civilian agencies-are leading to delays and softness in on-contract growth and new business awards, which could compress revenues and prolong below-trend top-line growth.

- Rising competition from non-traditional and commercial technology entrants, combined with a shift toward commercial-like, fixed-price, or outcome-based government contracting, raises the risk of pricing pressure and margin compression if SAIC cannot effectively differentiate its offerings or protect its core services (potentially impacting net margins and EPS growth).

- Secular trends in government IT-specifically, the push to automate, modernize, and utilize commoditized cloud/off-the-shelf solutions-are materially reducing demand for traditional, labor-based, and legacy IT services, creating a risk of margin pressure and diminishing long-term revenue streams for SAIC's historic business mix.

- Labor market shortages, government workforce turnover (especially in acquisition functions), and SAIC's dependence on specific large programs/customers increase execution risk, potentially resulting in delayed or lost revenue, contract re-bids, or delivery challenges that can erode both net margins and revenue predictability.

- Expectations of flat to low-single-digit growth in government IT and defense budgets due to macro budget constraints, the potential for continuing resolutions or shutdowns, and ongoing structural reprioritization of federal funds all threaten future backlog conversion rates and could limit long-term revenue and free cash flow growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $117.8 for Science Applications International based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $137.0, and the most bearish reporting a price target of just $85.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $7.3 billion, earnings will come to $367.7 million, and it would be trading on a PE ratio of 13.9x, assuming you use a discount rate of 8.4%.

- Given the current share price of $116.57, the analyst price target of $117.8 is 1.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Science Applications International?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.