Last Update 18 Jun 26

NPKI: Buybacks And Higher 2026 Guidance Will Drive Bullish Share Price Outlook

Analysts lifted their price target on NPK International by $2 to reflect updated assumptions around the company’s discount rate, revenue growth, profit margin and future P/E framework.

What’s in the News for NPK International

- NPK International reported that from January 1, 2026 to March 31, 2026, it repurchased 200,000 shares, representing 0.24% of its stock for $2.7 million under its existing buyback program. Source: Key Developments

- Since the buyback program was announced on February 21, 2024, NPK International has completed the repurchase of 3,239,103 shares, representing 3.78% of its stock for $22.99 million. Source: Key Developments

- NPK International raised earnings guidance for 2026, with the company now expecting revenues in a range of $310 million to $325 million for the year. Source: Key Developments

Valuation Changes for NPK International

- Fair Value: Held steady at $20.33 per share, with no change in the underlying fair value estimate for NPK International.

- Discount Rate: The discount rate has fallen slightly from 8.18% to 8.14%, reflecting a modest adjustment to the company’s risk assumptions.

- Revenue Growth: The revenue growth assumption is effectively unchanged at 12.20%, indicating a consistent outlook for NPK International’s top line trajectory.

- Net Profit Margin: The profit margin assumption remains stable at 17.25%, suggesting no material shift in expected profitability levels.

- Future P/E: The future P/E multiple has edged down slightly from 30.89x to 30.86x, marking a small reduction in the valuation multiple applied to NPK International.

Key Takeaways

- Expanding infrastructure spending and longer rental contracts are driving sustained revenue growth, improved asset utilization, and enhanced earnings consistency.

- Innovation in high-margin products and a strong balance sheet enable ongoing investment, market share gains, and improved shareholder returns.

- Dependence on large infrastructure projects, unpredictable product sales, slow market diversification, and rising cost pressures create significant risks to NPK International's revenue and profitability stability.

Catalysts

About NPK International- A temporary worksite access solutions company, manufactures, sells, and rents recyclable composite matting products.

- NPK International is benefiting from robust, sustained demand for utility transmission and pipeline infrastructure, supported by increasing global investment in critical infrastructure modernization and energy transition projects; with the company reasonably early in this wave of spending and utilities reaffirming or upping their CapEx commitments, there is a visible multi-year revenue growth runway from these long-term infrastructure trends.

- The ongoing shift by utility and infrastructure customers toward longer-duration rental contracts is increasing asset utilization rates (currently trending at the high end of historical ranges), providing greater revenue visibility and operational leverage-which should support improved earnings consistency and operating margins.

- Continued expansion of NPK International's rental fleet and geographic footprint-especially in high-growth regions such as the Midwest, Gulf Coast, and markets tied to infrastructure spending-positions the company to capture more share from secular increases in food, energy, and infrastructure demand, driving sustainable top-line and EBITDA growth over the long term.

- Industry adoption of advanced, longer-life composite mats (versus traditional timber) for access solutions is accelerating, with NPK's product innovation and strong customer relationships with utilities and fleet operators driving a secular transition to higher-margin, value-added products-enhancing overall net margins.

- Strong and flexible balance sheet with ample liquidity allows continued investment in fleet expansion, operational efficiency, and share repurchases, while also enabling potential strategic acquisitions; this supports both revenue growth and shareholder returns (EPS uplift from buybacks), and underpins the company's undervaluation relative to forward growth prospects.

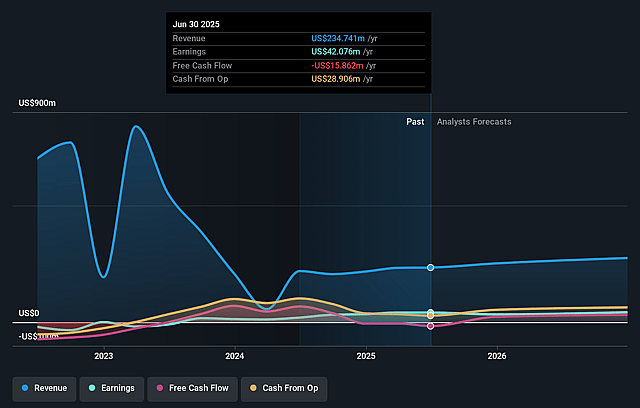

NPK International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming NPK International's revenue will grow by 12.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.5% today to 17.2% in 3 years time.

- Analysts expect earnings to reach $70.0 million (and earnings per share of $0.81) by about June 2029, up from $35.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 31.0x on those 2029 earnings, down from 37.4x today. This future PE is greater than the current PE for the US Trade Distributors industry at 24.6x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.14%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- NPK International's significant increase in rental revenues has been driven by a concentrated surge in large-scale infrastructure projects; however, this exposes the company's future revenues to project timing risks and sector cyclicality-potentially leading to revenue volatility if such projects decline or are delayed.

- The company's product sales, while currently robust, are described as more difficult to predict and are down year-over-year from record levels, suggesting a risk of declining or inconsistent revenue streams as industry transitions or customer preferences shift-negatively impacting both revenue stability and net margins.

- While NPK International is expanding geographically, its historical concentration in oil and gas basins and slower expansion into new markets could limit long-term growth and expose the company to competitive pressure and regional market downturns-putting both revenue growth and earnings at risk.

- The elevated SG&A expenses tied to performance-based incentives and rightsizing efforts, along with management's ongoing focus on streamlining overhead, indicate operating cost pressures and execution risk; if not managed effectively, these could compress operating margins and lower overall profitability.

- Increasing reliance on large utility and infrastructure customers, and the heavy investment in rental fleet scale, may create vulnerability if regulatory or policy changes (e.g., delayed utility CapEx, shifting infrastructure priorities, or increased compliance demands) result in reduced project pipelines or higher operational costs-adversely impacting revenue growth, EBITDA, and net earnings over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $20.33 for NPK International based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.0, and the most bearish reporting a price target of just $18.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $405.8 million, earnings will come to $70.0 million, and it would be trading on a PE ratio of 31.0x, assuming you use a discount rate of 8.1%.

- Given the current share price of $15.9, the analyst price target of $20.33 is 21.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on NPK International?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.