Last Update 22 Jun 26

BR: AI Trading And Tokenization Platforms Will Drive Future Upside

Analysts kept their fair value estimate for Broadridge Financial Solutions at $206.50, with only minor model tweaks to the discount rate, revenue growth, profit margin, and future P/E assumptions, resulting in a largely unchanged price target narrative.

What's in the News for Broadridge Financial Solutions

- LTX, backed by Broadridge Financial Solutions, introduced new agentic AI capabilities in its BondGPT tool. These capabilities allow users to set up AI agents that monitor real time bond markets and execute predefined trading workflow actions under human supervision. (Source: LTX/BondGPT news)

- Broadridge reported that its Distributed Ledger Repo platform processed US$7.2 trillion of repo transactions in May 2026, with an average daily volume that was more than 3x the level reported a year earlier. The company also outlined plans to extend this infrastructure to tokenized securities across multiple asset classes. (Source: DLR platform news)

- Broadridge and Fispoke agreed to collaborate so independent advisors, RIAs, broker dealers, and wealth platforms can access securities based lending and private banking style liquidity tools through Fispoke’s white labelled interface built on Broadridge technology. (Source: Broadridge and Fispoke partnership news)

- Broadridge joined Anthropic’s Project Glasswing to apply frontier AI models to cybersecurity, with the goal of strengthening protection for critical financial software systems and sensitive data. (Source: Project Glasswing news)

- Matrix Trust Company, a Broadridge subsidiary, is providing the collective investment trust structure and trustee role for Pacific Life’s new Income Horizon series. This series is designed to offer defined contribution plan participants access to guaranteed lifetime income inside existing plan setups. (Source: Pacific Life Income Horizon news)

Valuation Changes for Broadridge Financial Solutions

- Fair Value Estimate held steady at $206.50, indicating no change to the central valuation level.

- Discount Rate rose slightly from 7.70% to 7.74%, reflecting a modest adjustment to the risk or return assumptions used in the model.

- Revenue Growth was kept effectively unchanged at 5.11%, with only a minor recalibration in the underlying inputs.

- Net Profit Margin was maintained at about 14.61%, with only a very small numerical adjustment that does not alter the margin view.

- Future P/E nudged slightly higher from 23.05x to 23.08x, signalling a small tweak to the multiple applied in the valuation framework.

Key Takeaways

- Growth in digital services, regulatory solutions, and SaaS models is driving more predictable, recurring revenue and supporting margin expansion.

- International expansion and technology leadership in secure, innovative platforms are positioned to boost client retention and long-term earnings resilience.

- Revenue and earnings growth face headwinds from declining event-driven revenues, macro uncertainty, competitive pressures, margin constraints, and disruptive financial technology trends.

Catalysts

About Broadridge Financial Solutions- Provides investor communications and technology-driven solutions for the financial services industry.

- The continued shift toward digitization of financial services, evidenced by Broadridge's growing double-digit digital revenue and rapid increases in digitization rates for regulatory communications (now >90% for equity proxies), positions the company to benefit from rising demand for digital investor communications and lower-cost delivery, supporting long-term recurring revenue growth and future margin expansion.

- Increasing regulatory complexity-such as new requirements in digital assets, shareholder engagement, and disclosure regimes-are creating additional high-margin compliance and governance work; Broadridge is expanding solutions like its voting choice platform (growing from 8 to 400 funds in 2 years) and adding new products in digital asset disclosure, driving sustained growth in regulatory revenue streams.

- Broadridge's leadership in secure, scalable, and innovative transaction processing (including blockchain/tokenization and AI-enabled platforms like OpsGPT and distributed ledger repo solutions) aligns with financial institutions' growing focus on security and the modernization of back-office operations, enabling new product launches, increasing switching costs, and supporting revenue growth and improved operating margins.

- Expansion into international markets, highlighted by the acquisition of Acolin and growing international client wins (e.g., new sales to leading Japanese and Canadian institutions), is expanding Broadridge's addressable market and expected to be a catalyst for top-line revenue growth over the next several years.

- The company's increasing share of SaaS and recurring subscription models, combined with consistently high client retention rates (97–98%), is enhancing the predictability and resilience of revenues and earnings, and positioning Broadridge for sustainable EPS growth and ongoing dividend increases.

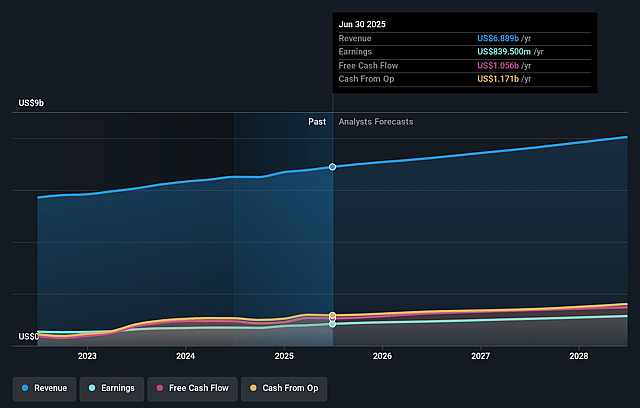

Broadridge Financial Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Broadridge Financial Solutions's revenue will grow by 5.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 15.0% today to 14.6% in 3 years time.

- Analysts expect earnings to reach $1.2 billion (and earnings per share of $11.18) by about June 2029, up from $1.1 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 23.1x on those 2029 earnings, up from 14.5x today. This future PE is greater than the current PE for the US Professional Services industry at 18.7x.

- Analysts expect the number of shares outstanding to decline by 1.26% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.74%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Event-driven revenues, which contributed a record $319 million in fiscal '25 and supported adjusted EPS growth, are expected to decline in fiscal '26, returning closer to their historical average; this presents a risk to year-over-year earnings and revenue growth.

- Longer sales cycles in key segments-particularly GTO (capital markets and wealth)-reflect ongoing macro uncertainty and client hesitancy, which may constrain new sales conversion, impacting future recurring revenue growth and backlog replenishment.

- The transition of some clients away from Broadridge's capital markets offerings, including an exit to an alternate provider causing a 1-point drag on segment growth, illustrates competitive and client concentration risks that could pressure revenue stability.

- Margin expansion may be limited due to headwinds from lower float income (as interest rates fall) and higher distribution revenues (which are low/no margin), risking net margin compression despite underlying operational efficiency.

- While tokenization and blockchain are presented as growth drivers, the broader industry trend toward direct, real-time engagement by investors (disintermediation) and the potential of next-gen financial technology could bypass traditional intermediaries like Broadridge, threatening its core proxy and processing businesses and, longer term, top-line revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $206.5 for Broadridge Financial Solutions based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $255.0, and the most bearish reporting a price target of just $165.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $8.5 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 23.1x, assuming you use a discount rate of 7.7%.

- Given the current share price of $137.6, the analyst price target of $206.5 is 33.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Broadridge Financial Solutions?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.