Last Update 01 Jun 26

STEL: Fair Outlook Will Balance Merger Vote And P E Assumptions

Analysts have adjusted their price target on Stellar Bancorp to $38.00, reflecting updated assumptions around the discount rate and future P/E, while maintaining their prior fair value estimate.

What's in the News

- Stellar Bancorp has scheduled a Special and Extraordinary Shareholders Meeting for May 27, 2026, at 10:00 a.m. Central Standard Time in the Galveston conference room, 9 Greenway Plaza, eighth floor, Houston, Texas.

- Shareholders are set to consider approval of an agreement and plan of merger dated January 27, 2026, between Stellar Bancorp and Prosperity Bancshares, Inc., which includes a proposed merger of Stellar Bancorp with and into Prosperity Bancshares.

- The meeting agenda includes a nonbinding, advisory vote on compensation that may be paid or become payable to Stellar Bancorp’s named executive officers in connection with the proposed merger.

- Shareholders may also be asked to approve any adjournment or postponement of the special meeting to solicit additional proxies if there are not sufficient votes to approve the merger proposal or to allow time for any supplement or amendment to the proxy statement or prospectus to be provided to holders of Stellar Bancorp common stock.

- Source: Company key developments filing for Stellar Bancorp, dated May 27, 2026.

Valuation Changes

- Fair Value: Model fair value remains at $38.00, with no change from the prior estimate.

- Discount Rate: The discount rate has risen slightly from 6.978% to 7.108% in the updated assumptions.

- Revenue Growth: Forecast revenue growth is effectively unchanged at around 5.76%.

- Net Profit Margin: The projected net profit margin remains essentially stable at about 25.71%.

- Future P/E: The assumed future P/E has risen slightly from 17.82x to 17.88x.

Key Takeaways

- High expectations for margin growth and branch-driven advantage may underestimate risks from digital disruption and declining relevance of physical branches.

- Valuation overlooks challenges from geographic concentration, integration risks, and rising compliance and technology costs, threatening long-term earnings stability.

- Favorable market trends, strong expense discipline, and strategic investments position Stellar Bancorp for resilient growth, improved profitability, and continued shareholder value enhancement.

Catalysts

About Stellar Bancorp- Operates as the bank holding company that provides a range of commercial banking products and services primarily to small and medium-sized businesses, professionals, and individual customers.

- Share price appears to reflect high expectations that Stellar Bancorp can effectively defend and grow margins through core deposit growth and disciplined relationship banking, despite intensifying competition from digital-first banks and fintechs, posing risk to long-term revenue and net margin stability if digital disruption accelerates.

- The current valuation seems to assume continued organic loan growth and sustained market share gains, banking on robust Texas/Southwest economic trends and small business expansion, while underestimating risk from geographic concentration and potential regional economic downturns that could pressure loan growth and future earnings.

- Investors seem to discount the challenge of rising compliance, technology, and ESG-related costs, as increased regulatory and stakeholder requirements may outpace operational leverage improvements, resulting in longer-term net margin compression.

- The share price likely prices in full and timely realization of merger-related synergies from Allegiance and CBTX, with little room for integration setbacks or cost overhang, which could dampen near-term earnings and inflate the expense base if synergies fall short.

- Valuation appears to presume that branch network relevancy and relationship banking will drive sustainable competitive advantage, discounting structural headwinds from declining physical branch usage and secular shift to online engagement, factors that could weaken cross-sell rates and constrain revenue growth over time.

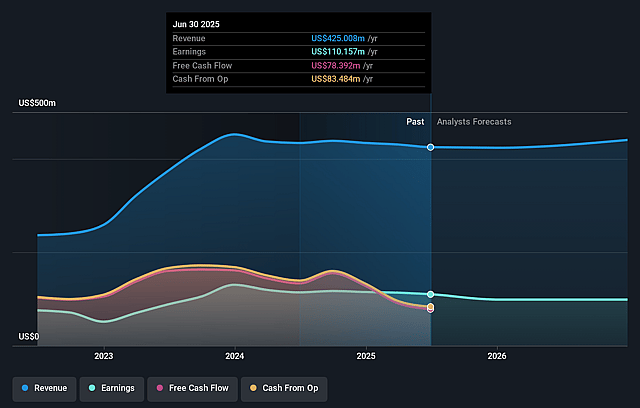

Stellar Bancorp Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Stellar Bancorp's revenue will grow by 5.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 25.0% today to 25.7% in 3 years time.

- Analysts expect earnings to reach $127.9 million (and earnings per share of $2.56) by about June 2029, up from $105.1 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $113.6 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 18.1x on those 2029 earnings, up from 17.8x today. This future PE is greater than the current PE for the US Banks industry at 11.5x.

- Analysts expect the number of shares outstanding to decline by 0.84% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Stellar Bancorp operates in a rapidly growing Texas market benefiting from favorable demographic and business migration trends, which underpins sustained commercial banking and small business loan demand and could drive ongoing revenue and earnings growth.

- The company has demonstrated effective expense management and positive operating leverage, reporting flat or improved non-interest expenses alongside growing net income and tangible book value, suggesting the potential for expanding net margins and stronger long-term profitability.

- Recent strategic investments in new talent, digital platforms, and expansion of C&I lending offer opportunities to further diversify revenue streams, improve customer acquisition and retention, and reduce risk concentrations, supporting more resilient earnings over time.

- Stellar's strong capital position (risk-based capital ratio of 15.98%), robust liquidity, and active share repurchase program provide the financial flexibility to pursue opportunistic growth via organic expansion or selective M&A, which could enhance shareholder value and buffer earnings volatility.

- The ability to maintain a structurally strong core net interest margin-currently above industry averages-and the likelihood of margin improvement should rates decline or funding composition continues to favor core sources, position Stellar Bancorp to defend and potentially grow net interest income and overall profitability in the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $38.0 for Stellar Bancorp based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $44.0, and the most bearish reporting a price target of just $32.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $497.6 million, earnings will come to $127.9 million, and it would be trading on a PE ratio of 18.1x, assuming you use a discount rate of 7.1%.

- Given the current share price of $36.78, the analyst price target of $38.0 is 3.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Stellar Bancorp?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.