Last Update 17 Jun 26

WDFC: Leadership Changes And Brand Strength Will Guide Fairly Valued Stock

Analysts now see WD-40 as fairly valued at around $249.50 per share, with the latest price target adjustments reflecting a mix of cautious recalibration and fresh bullish coverage that keeps the overall valuation framework essentially unchanged.

Analyst Commentary

Recent research on WD-40 stock reflects a split view, with some analysts focused on long-term growth potential and others adjusting expectations around execution and valuation at current levels.

Bullish Takeaways

- Bullish analysts highlight WD-40's brand strength as a key support for long-term demand, which they see as an anchor for the current valuation framework.

- They point to room for further market penetration and product adoption as potential drivers that could justify the stock trading near the latest fair value estimates.

- Supportive commentary suggests confidence that management can continue to execute on WD-40's core business model without needing major shifts in strategy.

- Some bullish views see the recent round of research coverage itself as a sign that WD-40 continues to attract institutional attention at current price levels.

Bearish Takeaways

- Bearish analysts are cautious enough on execution or growth expectations that they have cut price targets, indicating less comfort with upside from the prior valuation range.

- The lowered target implies concern that WD-40 may face limits to how much additional growth can be reflected in the share price without clearer evidence on future performance.

- Some of the cautious commentary frames the stock as fully priced, which could constrain near term re-rating potential if fundamentals simply track existing expectations.

- Overall, more conservative views see the latest adjustments as a reminder that even high quality consumer brands like WD-40 can face a tighter margin of safety when shares trade close to fair value estimates.

What’s in the News for WD-40

- WD-40 Company announced four executive leadership appointments aimed at strengthening organizational alignment and long term priorities, including Patricia Olsem as chief strategy and innovation officer and Claudia Fenske as chief brand and marketing officer, with a focus on collaboration and the use of AI and digital technologies for product development and marketing. Source: WD-40 Company Announces Four Executive Leadership Appointments to Boost Growth and Innovation.

- Sara Hyzer has been appointed president of the Americas division, with Nicholas Giordano joining the leadership team, supporting continuity across WD-40’s operations according to recent company communications. Source: WD-40 Company Announces Four Executive Leadership Appointments to Boost Growth and Innovation.

- Insider buying activity at WD-40 has included seven insider purchases over the past year, which the company’s recent leadership announcement highlighted as a signal of internal confidence. Source: WD-40 Company Announces Four Executive Leadership Appointments to Boost Growth and Innovation.

- On June 4, 2026, WD-40 reported that current chief financial officer Sara K. Hyzer plans to transition from the CFO role and is expected to assume the position of division president, Americas after a new CFO is appointed, while continuing as CFO until a successor is in place. Source: Company filing on executive changes.

- Between December 1, 2025 and February 28, 2026, WD-40 repurchased 38,175 shares, about 0.28% of its stock, for US$7.99 million, completing a total buyback of 162,175 shares, about 1.2%, for US$36.18 million under a program first announced on July 10, 2023. Source: Company buyback update.

Valuation Changes for WD-40 Stock

- Fair Value: steady at $249.50 per share, with no change between the prior and updated estimates.

- Discount Rate: unchanged at 7.11%, indicating a consistent required return in the updated model.

- Revenue Growth: effectively stable at about 6.24% in both the previous and current assumptions.

- Net Profit Margin: essentially flat at around 12.81%, with only a marginal numerical adjustment in the updated figure.

- Future P/E: maintained at roughly 40.75x, with no practical shift in the earnings multiple used for WD-40.

Key Takeaways

- Geographic expansion and direct market strategies in EIMEA indicate potential for sustained revenue growth and enhanced margins.

- Premiumization and divestment of less profitable brands aim to boost overall margins and refocus the company on higher-growth opportunities.

- Challenges such as divestiture uncertainty, currency fluctuations, and regional market conditions could affect WD-40's revenue growth and profit margins.

Catalysts

About WD-40- Develops and sells maintenance products, and homecare and cleaning products in North America, Central and South America, Asia, Australia, Europe, India, the Middle East, and Africa.

- The significant volume growth in Europe, India, the Middle East, and Africa (EIMEA), particularly driven by the transition to direct markets in areas like Brazil and potential new strategies for more markets, suggests continued revenue growth. This geographic expansion strategy will likely enhance revenue over the coming years.

- The company's focus on premiumization of products, with targets for a compound annual growth rate for premium products exceeding 10%, is poised to improve net margins by shifting the product mix towards higher-margin offerings.

- WD-40’s strategy to divest its less profitable home care and cleaning brands is expected to position the company as a higher growth and higher gross margin enterprise, ultimately boosting operational margins and net margins once complete.

- Supply chain optimization initiatives, such as improved efficiencies and cost savings through strategic supplier partnerships, are projected to mitigate potential tariff impacts and support margin expansion, contributing positively to gross margins.

- The focus on boosting digital commerce and expanding brand awareness via e-commerce platforms is anticipated to drive revenue growth and improve earnings by capitalizing on new customer acquisition and sales channels.

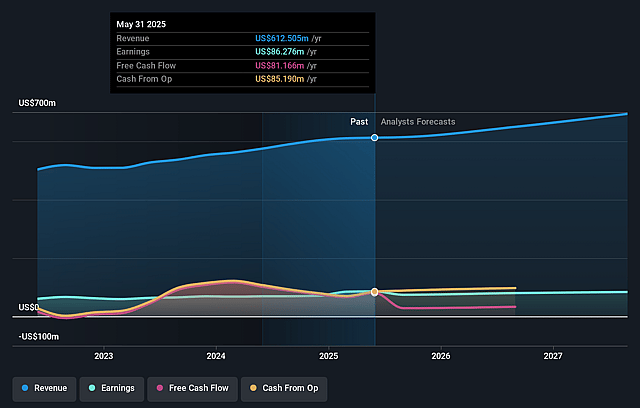

WD-40 Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming WD-40's revenue will grow by 6.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.5% today to 12.8% in 3 years time.

- Analysts expect earnings to reach $97.8 million (and earnings per share of $6.85) by about June 2029, up from $79.8 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 41.4x on those 2029 earnings, up from 38.4x today. This future PE is greater than the current PE for the US Household Products industry at 20.9x.

- Analysts expect the number of shares outstanding to decline by 0.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Uncertainty around the anticipated divestiture of WD-40's home care and cleaning business, which may impact revenue and operating income if not successfully completed as planned.

- Foreign currency exchange rate fluctuations present a headwind, impacting net sales and operating income as highlighted by currency-adjusted sales figures.

- Challenges in the Asia Pacific region, such as the 1% sales decline and weaker market conditions, could affect total revenue growth.

- Potential inflationary pressures and tariff impacts may necessitate price adjustments, potentially affecting profit margins and overall earnings.

- Higher operating expenses, particularly related to employee costs and brand-building activities, have increased the cost of doing business as a percentage of net sales, impacting net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $249.5 for WD-40 based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $763.2 million, earnings will come to $97.8 million, and it would be trading on a PE ratio of 41.4x, assuming you use a discount rate of 7.1%.

- Given the current share price of $227.64, the analyst price target of $249.5 is 8.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on WD-40?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.