Last Update 25 Jun 26

BULL: AI Trading And Buybacks Will Drive Long-Term Upside Potential

Analysts have reiterated their price target on Webull at $12.00, citing only very small tweaks to the discount rate, revenue growth, profit margin, and future P/E assumptions rather than any major shift in the underlying outlook.

What’s in the News for Webull

- Webull launched its Model Context Protocol (MCP) AI server for U.S. clients, allowing investors to use plain language to query real-time data, check balances, and place or modify orders through the platform’s OpenAPI, with plans to extend access to additional markets. (Source: company announcements, June 2026)

- Webull introduced mutual funds for IRA accounts in beta for select U.S. customers, giving retirement investors access to professionally managed, diversified mutual funds within the Webull platform, with a broader rollout to all IRA accounts planned. (Source: company announcements, 2026)

- Webull launched private market SPVs for accredited investors through a partnership with Monark Markets and Monark Capital Management LLC, providing exposure to late stage private companies that have typically been available mainly to institutional and high net worth investors. (Source: recent news stories)

- Webull Canada rolled out 24/5 Overnight Trading and zero commission trading on U.S. and Canadian equities, extending trading hours and reducing explicit trading costs for Canadian clients while offering free level one overnight market data and access to advanced tools. (Sources: company announcements, recent news stories)

- Webull Corporation authorized a share repurchase program of up to US$100 million, to be funded by existing cash and future cash flow over a 12 month period. (Source: company announcements, April 2026)

Valuation Changes for Webull

- Fair Value: The model fair value for Webull is held at $12.0 per share, with no change from the prior $12 level.

- Discount Rate: Discount rate assumptions are adjusted slightly higher from 7.76% to about 7.77%.

- Revenue Growth: Forecast revenue growth is kept effectively unchanged at around 23.10%.

- Net Profit Margin: The expected net profit margin remains broadly stable at roughly 22.44%.

- Future P/E: The future P/E assumption is adjusted slightly higher from about 38.42x to roughly 38.44x.

Key Takeaways

- Diversification through global expansion and thriving subscription-based services is enhancing customer growth, revenue stability, and higher average user returns.

- Agile adoption of digital assets and favorable regulations strengthen product innovation, user engagement, and expansion of revenue sources worldwide.

- Webull's reliance on retail trading, exposure to regulatory and competitive pressures, and vulnerability to changing investor behavior threaten sustained revenue and margin growth.

Catalysts

About Webull- Operates as a digital investment platform.

- Ongoing expansion into new international markets, including recent launches in Canada, Latin America, and Europe, is rapidly diversifying Webull's customer base and driving robust growth in assets under management (AUM), which supports future revenue and top-line growth.

- The successful launch and acceleration of subscription-based offerings such as Webull Premium and paid analytics products are already exceeding targets, combining higher daily trading activity and increased average revenue per user (ARPU) to boost net margins and recurring revenue stability.

- Rapid adoption and reintroduction of crypto trading, alongside the platform's ability to quickly add new digital asset classes and prediction markets, positions Webull to capture growing demand for broad, mobile-accessible investment options, fueling revenue growth and market share.

- Strategic capital raises, including a $1 billion standby equity facility, are enabling accelerated new product development and global platform rollout, ensuring continued scale and innovation while supporting future margin expansion and operating leverage.

- Positive regulatory developments fostering transparency and enabling expanded access to digital assets allow Webull to introduce and monetize innovative products globally, driving higher user engagement, increased fee income, and broader revenue streams.

Webull Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

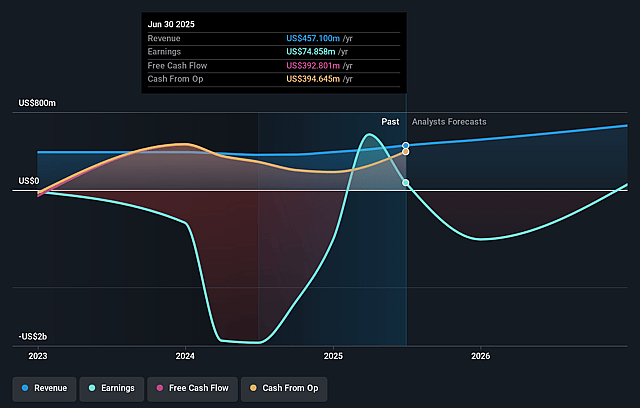

- Analysts are assuming Webull's revenue will grow by 23.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from -82.5% today to 22.4% in 3 years time.

- Analysts expect earnings to reach $254.0 million (and earnings per share of $0.48) by about June 2029, up from -$500.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 38.4x on those 2029 earnings, up from -7.3x today. This future PE is lower than the current PE for the US Capital Markets industry at 40.0x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.77%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Webull's significant growth in trading volumes, revenue, and customer assets is highly correlated with recent market volatility and favorable equity market conditions-if broader macroeconomic cycles change or retail trading activity structurally declines, transaction-based revenue could contract, impacting both revenue and long-term earnings.

- The platform's profitability and expansion are reliant on acquiring and monetizing active, self-directed retail traders; demographic shifts as younger investors age or widening consumer skepticism toward aggressive trading platforms could hinder customer acquisition, retention, and wallet share growth, thus slowing revenue expansion.

- Although rapid international and crypto rollout is highlighted as an opportunity, regulatory approval processes vary by region and asset class-with increasing regulatory scrutiny globally, delays, restrictions, or adverse regulations could constrain product offerings and require higher compliance costs, pressuring net margins and future revenue.

- Webull faces intensifying competition from larger, diversified brokers (e.g., Fidelity, Schwab, Robinhood) and specialized fintechs, which may escalate customer acquisition costs and impede the up-selling of higher-margin products (e.g., premium subscriptions, wealth management), thereby limiting margin and earnings growth.

- Ongoing industry-wide price competition (e.g., zero-commission trading, low-cost margin loans) and commoditization of core brokerage services places sustained pressure on fee structures, risking long-term margin compression and eroding profitability even as operating scale increases.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $12.0 for Webull based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $14.0, and the most bearish reporting a price target of just $10.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.1 billion, earnings will come to $254.0 million, and it would be trading on a PE ratio of 38.4x, assuming you use a discount rate of 7.8%.

- Given the current share price of $6.71, the analyst price target of $12.0 is 44.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Webull?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.