Last Update 18 May 26

Fair value Decreased 11%JACK: Turnaround Plan Will Rely On 2026 EBITDA Recovery Under New Interim CEO

Jack in the Box's analyst-derived fair value estimate has been reduced from $20.56 to $18.26, as analysts reset price targets across the board in response to weaker same-store sales, lowered guidance, leadership changes, ongoing concern about franchisee profitability, and upcoming refinancing costs.

Analyst Commentary

Recent research shows a wide range of views on Jack in the Box, with most firms cutting price targets but differing on how much value they still see in the stock. Target prices now span roughly US$12 to US$24, reflecting contrasting opinions on execution risk, earnings visibility, and the impact of recent guidance changes.

Bullish Takeaways

- Bullish analysts who keep Outperform or similar ratings point to management's updated 2026 EBITDA guidance, which they say still lines up with current consensus. They suggest the current valuation already reflects a lot of the recent bad news.

- Some research notes highlight commentary that same-store sales trends are moving toward flattish into fiscal Q3. They see this as a potential stabilizer for profit expectations if that trend holds.

- There are a few price target increases into the low to mid teens. These analysts indicate that, at current levels, risk and reward look more balanced than before even after "underwhelming" fiscal Q2 results and reduced 2026 guidance.

- Several Neutral and Hold ratings alongside modestly higher targets suggest that, while growth visibility is limited, some analysts see room for execution improvements to support current or slightly higher valuations over time.

Bearish Takeaways

- Bearish analysts, including at Goldman Sachs, have cut price targets into the low teens and maintain cautious views. They cite weaker same-store sales, lowered guidance, and limited visibility on margins and growth.

- Multiple research notes emphasize that fiscal Q2 same-store sales fell 3.8% and that management reduced fiscal year guidance. This drives concerns about the company hitting its longer term earnings targets.

- Franchisee profitability is flagged as under pressure, which could restrict reinvestment in stores and weigh on longer term growth and brand execution, putting the current valuation at risk if trends do not improve.

- Upcoming debt refinancing is expected by some analysts to lift annual interest expense by about US$23m. They see this as another headwind for free cash flow and equity valuation unless operating performance improves.

What's in the News

- The board appoints Mark King as Interim CEO effective May 13, 2026, following his tenure as board member and chair and prior CEO roles at Taco Bell and Xponential Fitness (Executive Changes).

- The company updates fiscal 2026 guidance to a low single digit same store sales decline versus fiscal 2025, and separately reiterates a range of same store sales of 1% decline to 1% growth versus fiscal 2025, with pressure expected in the first quarter and sequential improvement anticipated over the rest of the year (Corporate Guidance).

- There is an ongoing proxy fight with Biglari Capital, which urges shareholders to vote against Independent Chair David Goebel, citing what it describes as significant shareholder value destruction and governance concerns, while Jack in the Box defends its board and strategy and encourages support for all 10 director nominees (Investor Activism).

- Proxy advisory firms are split on governance, with ISS recommending shareholders vote for all board nominees and Glass Lewis and Egan Jones recommending votes against Goebel and several directors, reflecting differing views on performance and governance at the company (Investor Activism, Supporting Statements).

- The company extends its product lineup with a limited-time Smashed Jack Sliders Munchie Meal tied to its 75th anniversary and rolls out a nationwide matcha beverage platform featuring a Matcha Iced Latte and an OREO Matcha Shake (Product Announcements).

Valuation Changes

- Fair Value: The analyst-derived fair value estimate has been reduced from $20.56 to $18.26, a cut of roughly 11%.

- Discount Rate: The discount rate used in the model has edged down slightly from 12.5% to 12.46%.

- Revenue Growth: Assumed revenue growth has been revised from a 7.61% decline to a 10.29% decline, indicating a more cautious view on future dollar revenue trends.

- Net Profit Margin: Assumed net profit margin has moved from 7.46% to 14.13%, implying expectations for a higher share of dollar earnings per dollar of sales in the forecast period.

- Future P/E: The future P/E multiple has been reduced from 6.45x to 3.38x, indicating a lower valuation multiple being applied in the forward earnings model.

Key Takeaways

- Expansion in high-growth urban areas and modernization of restaurants are set to boost revenue, customer retention, and operational efficiency.

- Menu innovation, technology investment, and franchise-led growth are driving market share gains, improved margins, and long-term profitability.

- Heavy dependence on vulnerable customer segments and core regions, combined with rising labor costs and weak sales, threatens long-term growth and financial stability.

Catalysts

About Jack in the Box- Operates and franchises quick-service restaurants under the Jack in the Box and Del Taco brands in the United States.

- Strong early sales from new market openings in Chicago and Durham, combined with continued urbanization and population growth in core and expansion markets, position Jack in the Box for outsized revenue growth as these locations ramp and as the company increases its presence in high-growth urban corridors.

- Rollout of modernization initiatives, including upgrades to 1,000+ restaurants and full digital POS deployment, is likely to boost throughput, customer experience, and drive-thru convenience-directly supporting higher transaction volumes, improved customer retention, and ultimately higher top-line revenue.

- Focus on menu innovation (e.g., craveable flavor launches, targeted value offerings, and product variety) and culturally relevant marketing (especially to diverse and younger demographics) leverages demographic shifts in the US, positioning the brand to gain share and lift same-store sales over the long term.

- Enhanced technology investments-including digital ordering, loyalty, and data analytics-plus operational improvements and restaurant closures (via JACK on Track) are poised to reduce labor costs and overhead, supporting a sustainable improvement in net margins and operating leverage.

- Franchise-led expansion and attractive franchisee economics (via healthy real estate divestitures, improved value propositions, and operational initiatives) lay a foundation for long-term earnings growth and return on equity, even as capital intensity remains modest.

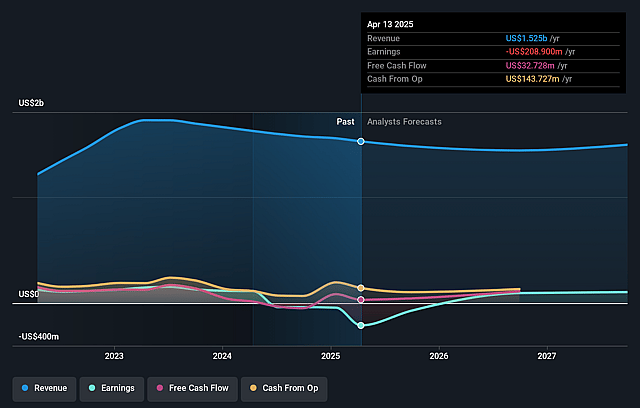

Jack in the Box Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Jack in the Box's revenue will decrease by 10.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -7.4% today to 14.1% in 3 years time.

- Analysts expect earnings to reach $146.2 million (and earnings per share of $7.42) by about May 2029, up from -$105.5 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 3.5x on those 2029 earnings, up from -2.0x today. This future PE is lower than the current PE for the US Hospitality industry at 20.0x.

- Analysts expect the number of shares outstanding to grow by 1.03% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy reliance on lower-income and Hispanic customer segments, who are exhibiting sustained spending pullbacks due to macroeconomic pressures, poses a long-term risk to traffic trends and revenue stability, particularly as these groups are over-indexed in Jack in the Box's core regions.

- Persistent same-store sales declines (-7.1% for Jack, -2.6% for Del Taco this quarter) and negative transaction growth, even amid price hikes, indicate weak underlying demand and threaten the company's ability to deliver sustained revenue and earnings growth.

- Elevated labor costs (Jack's labor cost at 34.5% of sales, Del Taco's at 39.6%) driven by wage inflation, regulatory changes (e.g., California minimum wage increases), and payroll tax adjustments continue to pressure restaurant-level margins, with further wage inflation anticipated, reducing net margins.

- High geographic concentration in California, Texas, and the Southwest limits diversification and increases vulnerability to localized economic downturns or policy changes, risking earnings volatility and compounding the impact of regional consumer weakness.

- Ongoing restaurant closures (80–120 expected in 2025, with more over time) and discontinued dividend/share buyback signal operational and financial strain, which may deter long-term investors and reduce per-share earnings power unless offset by successful turnarounds in new markets or aggressive cost containment.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $18.26 for Jack in the Box based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $55.0, and the most bearish reporting a price target of just $12.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.0 billion, earnings will come to $146.2 million, and it would be trading on a PE ratio of 3.5x, assuming you use a discount rate of 12.5%.

- Given the current share price of $10.87, the analyst price target of $18.26 is 40.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Jack in the Box?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.