Last Update 02 Jul 26

Fair value Increased 16%CMI: Data Center Power And Truck Demand Will Shape Measured Future Returns

The analyst fair value estimate for Cummins has been raised from $643.36 to $748.81. This change reflects higher Street price targets and updated assumptions around revenue growth, profit margins, and future P/E multiples that analysts link to strong demand trends in power, data center, truck, and infrastructure markets.

Analyst Commentary

Recent research on Cummins highlights a cluster of higher fair value and price targets, along with upgraded ratings, as analysts reassess the company against demand in power, data center, truck, and infrastructure markets. The commentary below distills what bullish analysts are focused on, along with areas where a more cautious reader may want to think about execution risk and earnings durability.

Bullish Takeaways

- Several bullish analysts have lifted price targets into the US$770 to US$901 range, tying their views to a larger addressable market for power solutions, ongoing infrastructure projects, and truck demand that supports their earnings assumptions.

- Research citing a US$20b total addressable market expansion from prime power awards points to Cummins' positioning in data center and high performance computing projects, with specific references to large engine products for West Texas facilities and potential follow-on opportunities in Canada.

- Analysts upgrading Cummins or reiterating positive views highlight the truck market backdrop and new engine platforms with higher content per unit, which they see as support for their earnings forecasts and the P/E multiples used in their valuation work.

- Some reports reference factors such as the relative cost of refined fuel versus natural gas, environmental regulations in the U.S. and overseas, and infrastructure development in emerging markets as structural supports for Cummins' power and engine businesses within their long term models.

Bearish Takeaways

- While targets and ratings have moved higher, bullish analysts are still relying on assumptions that demand trends in power, data centers, trucks, and infrastructure continue to support their revenue and margin forecasts. This leaves room for disappointment if those markets soften versus expectations.

- References to beatable 2026 margin assumptions signal that some models build in operational improvement and cost execution that is not yet visible in reported numbers. This could pressure valuation if the company falls short of those targets.

- Several research notes point to upside versus prior long term revenue outlooks and to consensus estimates that are viewed as conservative. This raises the bar for future earnings announcements and increases the risk of sentiment changing if Cummins does not track those more optimistic scenarios.

What’s in the News for Cummins

- Cummins agreed to supply about 2 gigawatts of high efficiency natural gas generator sets to Circe Energy between 2026 and 2030 for a behind the meter microgrid at Circe’s West Texas high performance computing and AI data center campus, using Cummins HSK78 and QSK60 platforms, according to Circe and Cummins announcements.

- The Circe partnership positions Cummins as a power provider to a large AI infrastructure project in the Permian Basin. The microgrid structure is designed to support data center power needs without relying on the regional grid, based on client announcement details.

- Cummins updated full year 2026 earnings guidance, stating that revenue is expected to be up 8% to 11% due to demand across several markets, particularly North America on highway and power generation.

- The company updated its 2030 outlook, stating that expected revenue is in a range of US$45b to US$50b, compared with a prior range of US$43b to US$48b.

- Cummins is involved in ongoing legal matters, including a jury verdict in Delaware finding misappropriation of C3 AI trade secrets and reference to a previously announced US$1.675b Clean Air Act settlement with the U.S. Department of Justice, according to C3 AI’s description of the case.

Valuation Changes for Cummins

- Fair Value: Raised from $643.36 to $748.81, which is an increase of roughly 16% in the analyst fair value estimate for Cummins.

- Discount Rate: Adjusted slightly higher from 8.54% to 8.60%, which implies a modestly higher required return in the updated model.

- Revenue Growth: Assumption lifted from 7.64% to 9.29%, which indicates a higher projected dollar revenue growth rate in the new forecast set.

- Profit Margin: Expected net profit margin refined from 11.44% to 12.04%, which points to a slightly stronger dollar earnings profile in the projections.

- Future P/E: Target future P/E multiple moved from 23.80x to 24.85x, which reflects a higher valuation multiple applied to Cummins earnings in the updated analysis.

Key Takeaways

- Diversified growth in power systems and clean energy investments is offsetting weakness in traditional truck markets, supporting stronger margins and resilience.

- Regulatory changes and new product launches are fueling pricing power and future revenue growth, as the company manages costs and expands production capacity.

- Cummins faces cyclical demand risks, regulatory and tariff uncertainty, weak alternative powertrain growth, rising competition, and vulnerability in key international markets.

Catalysts

About Cummins- Offers various power solutions worldwide.

- Cummins is experiencing strong and steadily growing demand for power generation equipment, especially from the data center sector, driven by increasing urbanization, digital infrastructure expansion, and the global shift toward cleaner, efficient energy solutions; this diversification is lifting revenue and supporting higher EBITDA margins, offsetting softness in the traditional truck markets.

- The company's two-year-plus backlog and continued capacity expansions in Power Systems position it to sustain elevated sales growth and margins, especially as additional production capacity comes online in 2026, directly benefiting future revenue and margin expansion.

- Tightening global emissions regulations and anticipated adoption of new product platforms (such as EPA27-compliant engines) create an opportunity for pricing power and market share stabilization as fleets upgrade, supporting future revenue growth and premium product margins as regulatory clarity emerges.

- Cummins' disciplined cost management, operational improvements, and ability to mitigate tariff headwinds-even as North American truck volumes decline-demonstrate resilient net earnings and margin protection, highlighting underlying operating leverage when cyclical markets recover.

- Ongoing investments in electrification, hydrogen, and stationary energy storage broaden Cummins' long-term addressable market; as secular decarbonization trends accelerate, these initiatives can unlock new revenue streams and recurring income (aftersales, services), ultimately supporting long-term earnings growth.

Cummins Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

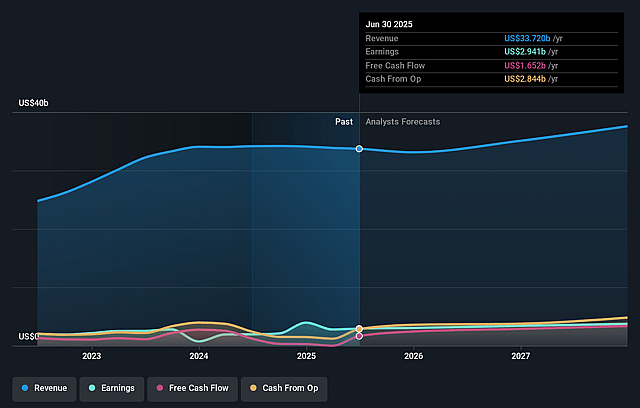

- Analysts are assuming Cummins's revenue will grow by 9.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.9% today to 12.0% in 3 years time.

- Analysts expect earnings to reach $5.3 billion (and earnings per share of $38.46) by about July 2029, up from $2.7 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $6.1 billion in earnings, and the most bearish expecting $4.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 25.0x on those 2029 earnings, down from 35.2x today. This future PE is lower than the current PE for the US Machinery industry at 27.9x.

- Analysts expect the number of shares outstanding to grow by 0.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.6%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent and worsening weakness in North American heavy

- and medium-duty truck demand (with order rates at multiyear lows and OEMs cutting production) exposes Cummins to large cyclical declines in core engine and component revenues and puts significant pressure on segment margins and earnings, especially if an economic or regulatory recovery is delayed.

- Regulatory and tariff uncertainty, with no clarity on the timeline or details of EPA27 emissions standards and ongoing unpredictable international tariff changes, is elevating costs, disrupting investment planning, and forcing duplicative engineering/development work; this increases SG&A and R&D expenses and could compress net margins until the policy environment stabilizes.

- Slowing growth and sustained EBITDA losses in Accelera (alternative powertrains and electrolyzers) indicate that Cummins is not yet capturing significant share or profitability in key zero-emission technologies, risking long-term revenue and market share erosion as the industry migrates away from legacy diesel platforms.

- Increasing competitive intensity from both traditional peers and new entrants in electrification, hydrogen, and backup power/microgrid solutions may lead to price compression, reduced pricing power, and margin pressure-particularly as pure-play EV and hydrogen firms ramp up offerings, threatening Cummins' ability to maintain its historical premium and long-term gross margins.

- International market strength (notably China and data center-driven power systems) currently underpins earnings, but these are vulnerable to de-globalization, shifting government incentives, macroeconomic slowdown, and increased local competition-any reversal in these secular demand tailwinds would negatively impact diversified revenue streams and consolidated profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $748.81 for Cummins based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $875.0, and the most bearish reporting a price target of just $520.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $44.2 billion, earnings will come to $5.3 billion, and it would be trading on a PE ratio of 25.0x, assuming you use a discount rate of 8.6%.

- Given the current share price of $682.32, the analyst price target of $748.81 is 8.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Cummins?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.