Last Update 19 May 26

Fair value Decreased 37%CLNE: Supportive EPA Mandates And Expanding RNG Network Will Drive Future Upside

Analysts have reduced their price target on Clean Energy Fuels to $6.00, citing updated views on fair value, growth, margins, and a very large future P/E multiple, informed in part by recent EPA renewable fuel standard decisions that are viewed as supportive for the broader sector.

Analyst Commentary

Bullish analysts point to the recent EPA renewable fuel standard decision as an important policy signal for the sector, with volume mandates that are viewed as constructive for low-carbon fuels. For Clean Energy Fuels, this policy backdrop is being used to support valuation work that leans on a very large future P/E multiple, given expectations around how compliant fuels may fit into long term demand trends.

These views are feeding into higher conviction that the stock’s current price embeds a meaningful discount to what some analysts view as fair value under the updated regulatory framework. The trimmed US$6.00 price target still reflects confidence that the company can execute against this backdrop, even as assumptions around growth and margins are recalibrated.

Bullish Takeaways

- Bullish analysts see the EPA’s final renewable fuel standard volumes as supportive for companies exposed to low-carbon fuels, which in their view underpins the use of a very large future P/E multiple in valuation work for Clean Energy Fuels.

- Some bullish views emphasize that the updated fair value assessment, even with a reduced target of US$6.00, leaves room for upside if the company delivers on execution within the more supportive regulatory setting.

- Positive sentiment is tied to the idea that clearer policy signals around renewable fuel demand can give the company a more visible framework for planning, which bullish analysts see as helpful for both growth expectations and margin assumptions.

- Analysts with a constructive stance highlight that sector wide support from the EPA decision could help sustain investor interest in low-carbon fuel stocks, which they see as a potential catalyst for valuation re-rating over time if company level execution lines up with expectations.

What’s in the News

- Announced expansion of the renewable natural gas fueling network with six new stations along major U.S. freight routes, adding locations in California, New Jersey, Oklahoma, Michigan and Washington and extending a network of more than 600 stations across North America (Key Developments).

- Board appointed Clay Corbus as Chief Executive Officer, effective April 23, 2026, succeeding co founder Andrew Littlefair, who will shift to a non employee government relations consultant role. Corbus brings nearly two decades of experience at the company plus an investment banking background (Key Developments).

- Outlined multiple new and extended agreements with trucking, refuse and transit fleets for renewable natural gas fueling and station operations, including arrangements with Ecology Transportation Services, Recology, WM, Washington Metropolitan Area Transit Authority, ABM Facility Services, Arlington Transit, the City of Scottsdale, Nashville International Airport and the City of Fort Smith (Key Developments).

- Issued 2026 earnings guidance that points to an expected net loss attributable to the company of US$71,000,000 to US$66,000,000. Management highlighted that unrealized gains or losses on customer contracts and variations in Amazon warrant vesting could materially affect reported GAAP results (Key Developments).

- Reported completion of a prior share repurchase program, with 14,301,158 shares bought for US$31.33 million since the March 13, 2020 authorization, and no shares repurchased from October 1, 2025 to December 31, 2025 (Key Developments).

Valuation Changes

- Fair Value: The analyst fair value estimate has been reduced from $9.57 to $6.00, bringing it in line with the updated price target.

- Discount Rate: The discount rate assumption has risen slightly from 7.24% to 7.43%, implying a modestly higher required return in the valuation model.

- Revenue Growth: Revenue growth expectations have fallen from 8.64% to 3.67%, indicating a more cautious view on potential top line expansion.

- Net Profit Margin: The net profit margin assumption has declined from 13.15% to 0.75%, pointing to a much thinner projected earnings profile.

- Future P/E: The future P/E multiple has increased from 34.2x to 454.7x, highlighting a heavier reliance on more distant earnings in the updated valuation work.

Key Takeaways

- Clean Energy's unique infrastructure and fleet relationships position it to rapidly capture market share as heavy trucking shifts toward low-carbon fuel alternatives.

- Supportive policy changes, growing ESG mandates, and supply advantages could accelerate revenue growth, margin expansion, and strategic partnership opportunities over slower competitors.

- Clean Energy Fuels faces long-term risks from electrification, customer concentration, regulatory uncertainty, margin pressures, and high capital needs that threaten sustained revenue and earnings growth.

Catalysts

About Clean Energy Fuels- Offers natural gas as alternative fuels for vehicle fleets and related fueling solutions in the United States and Canada.

- Analyst consensus expects the X15N Cummins engine launch to gradually catalyze RNG adoption, but the narrative underappreciates Clean Energy's near-exclusive first-mover advantage: with established fueling infrastructure, deep fleet relationships, and accelerating cost-competitiveness-especially as incremental truck prices fall faster than expected-the company can capture a disproportionate share of the early and growing heavy trucking conversions, fueling step-change upside to recurring fuel volumes and revenue.

- Whereas analysts broadly expect "supportive" state and federal RNG policies, potential finalization of 45Z tax credits, restoration of AFTC, and improved LCFS program clarity could create a compounding effect, driving rapid margin expansion as Clean Energy converts low-value gallons to high-margin RNG, with upside from meaningful retroactive credits and tailwinds from bipartisan rural development incentives.

- The accelerating pushback on full-scale electrification of heavy-duty vehicles-noted by key customers and reflected in public policy rollbacks-positions RNG as the only commercially viable, immediately scalable decarbonization pathway; Clean Energy can become the primary beneficiary as trucking fleets and regulators pivot rapidly toward practical, shovel-ready low-carbon solutions, supporting multi-year outperformance in fuel volumes and station utilization.

- Rising global ESG and decarbonization mandates are likely to result in major oil and gas companies, logistics providers, and retailers fast-tracking RNG adoption to hit near-term climate targets, potentially spurring additional strategic partnerships, fixed-volume off-take agreements, and even joint ventures, driving durable upside to contracted revenue, stronger pricing power, and premium valuations relative to slower-adapting peers.

- Clean Energy's privileged position at the "nozzle tip" and tightness in the RNG dispensing market provide leverage over upstream RNG suppliers, enabling improved pricing, supply optionality, and negotiating advantage which could structurally raise delivered fuel margins and non-fuel services EBITDA as RNG demand consistently outpaces available dispensing capacity.

Clean Energy Fuels Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Clean Energy Fuels compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Clean Energy Fuels's revenue will grow by 3.7% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -22.7% today to 0.7% in 3 years time.

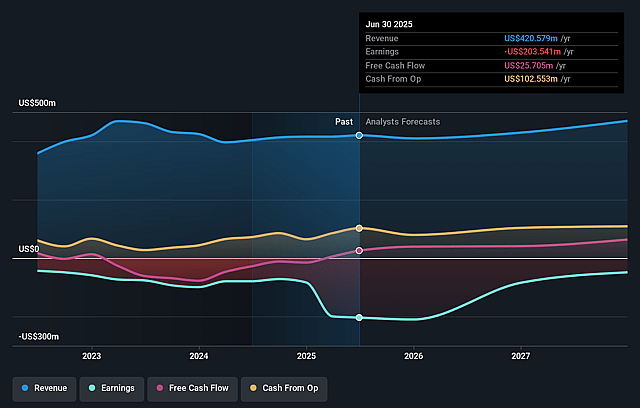

- The bullish analysts expect earnings to reach $3.6 million (and earnings per share of $0.01) by about May 2029, up from -$99.5 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $-51.2 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 454.8x on those 2029 earnings, up from -4.5x today. This future PE is greater than the current PE for the US Oil and Gas industry at 14.9x.

- The bullish analysts expect the number of shares outstanding to grow by 0.43% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.43%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Rapid electrification of transportation, combined with increasing global regulatory and subsidy support for zero-emission vehicles such as battery electric and hydrogen, poses a significant long-term threat to the addressable market for Clean Energy Fuels, which could suppress future revenue growth as demand for RNG in transportation diminishes.

- High customer concentration risk, as reflected in the company's reliance on large fleet partners like Amazon and major waste management firms, exposes Clean Energy to the risk that the loss or reduction of business from one or more key customers could negatively impact topline revenue stability and hinder consistent long-term growth.

- Policy uncertainty and an unfavorable long-term regulatory environment-particularly debates over the permanence of supportive programs like the Low Carbon Fuel Standard in California, the possibility that RNG may be deprioritized versus zero-emission alternatives, and the pending status of federal incentives such as 45Z-introduce earnings volatility that could undermine both margins and profitability if credits and subsidies are reduced or revoked.

- Margin compression remains a persistent risk due to increased competition from both traditional oil majors entering the RNG and biofuels market and emerging electric and hydrogen fueling infrastructure, which is likely to pressure net margins as Clean Energy competes on pricing and infrastructure investment.

- Ongoing high capital expenditures required for new RNG production projects and fueling station buildouts-despite slow or unpredictable demand ramp-up and lengthy project timelines-can increase financial leverage and strain future earnings, especially if secular trends steer transportation away from RNG and toward all-electric or hydrogen platforms.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Clean Energy Fuels is $6.0, which represents up to two standard deviations above the consensus price target of $3.84. This valuation is based on what can be assumed as the expectations of Clean Energy Fuels's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $6.0, and the most bearish reporting a price target of just $2.3.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $488.7 million, earnings will come to $3.6 million, and it would be trading on a PE ratio of 454.8x, assuming you use a discount rate of 7.4%.

- Given the current share price of $2.04, the analyst price target of $6.0 is 66.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Clean Energy Fuels?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.