Last Update 25 Jun 26

Fair value Increased 0.26%TMHC: Berkshire Cash Offer And Housing Headwinds Will Guide Future P E Multiple

The analyst price target for Taylor Morrison Home has been fine-tuned in light of the agreed $72.50 per share cash offer from Berkshire Hathaway, with analysts broadly aligning fair value closer to the deal terms as they highlight the high likelihood of completion and the limited scope for a competing bid.

Analyst Commentary

Recent commentary on Taylor Morrison Home centers on how closely the current share price tracks the agreed US$72.50 per share cash offer, with most research now focused on deal terms, valuation and the remaining execution risk rather than standalone growth potential.

Bullish Takeaways

- Bullish analysts describe the US$72.50 per share offer as a solid outcome for Taylor Morrison shareholders, pointing to upfront cash and clarity on value in what has been described as a challenging housing macro backdrop.

- The agreed price represents a reported 24% premium to the pre-deal level. Bullish analysts view this as attractive given current sector conditions and the shift in focus from fundamentals to deal completion.

- Some comment that the transaction values Taylor Morrison at about 1.1x P/B, which they see as a supportive reference point for homebuilder valuations, with the deal helping to establish a floor for group multiples.

- Several research notes highlight a high probability that the Berkshire Hathaway transaction closes as agreed. They see this as reducing uncertainty around the ultimate takeout value for existing shareholders.

Bearish Takeaways

- Bearish analysts have moved ratings to Hold, Sector Perform, Market Perform or No Rating, reflecting the view that with Taylor Morrison now trading primarily on deal terms, there is limited upside beyond the agreed cash price.

- Some commentary indicates surprise that the premium to book value was not larger, suggesting that on a P/B basis the consideration is viewed by these analysts as fair rather than generous.

- While a few acknowledge a slight possibility of a higher bid from private equity, international buyers or larger domestic builders, they broadly describe a competing offer as highly unlikely. This limits speculative upside.

- With fundamental coverage effectively on hold and the stock seen as driven by timing and completion risk, bearish analysts see less reason to focus on Taylor Morrison for investors seeking exposure to ongoing homebuilder growth or re rating potential.

What’s in the News for Taylor Morrison Home

- Berkshire Hathaway agreed to acquire Taylor Morrison Home in an all cash deal valuing the company at about US$8.5b in enterprise value, or US$72.50 per share, a 24% premium to the prior closing price. Taylor Morrison’s board unanimously recommended that shareholders approve the transaction. (Source: Berkshire Hathaway to Acquire Taylor Morrison Home Corporation for $8.5 Billion in All Cash Deal; Key Developments)

- Under the merger agreement, Taylor Morrison would become a private company and its stock would be delisted from the New York Stock Exchange once the deal closes. The closing is subject to shareholder and regulatory approvals that are targeted for the second half of 2026. (Source: Berkshire Hathaway to Acquire Taylor Morrison Home Corporation for $8.5 Billion in All Cash Deal; Key Developments)

- The merger terms include a US$221.6 million termination fee payable to Berkshire Hathaway if Taylor Morrison accepts a superior proposal or if the board changes its recommendation in specified circumstances, according to the definitive agreement. (Source: Key Developments)

- Taylor Morrison recently reported first quarter results that included a 29.7% year over year revenue decline and a 3.2% annual decline in earnings per share over the past two years. The company also reported a 33.2% two year backlog decline and an estimated 12.9% sales decline expected over the next 12 months, while highlighting strong liquidity of US$1.6b and plans to open more than 125 new communities in 2026. (Source: Taylor Morrison Home Reports Q1 Earnings Amid Strategic Expansion and Market Challenges; Taylor Morrison Faces Declining Sales and Backlog Amid Market Challenges)

- Operational updates include ongoing expansion of Taylor Morrison’s Esplanade resort brand and new community developments. These include the planned Braxton Ridge community near Greenville and Spartanburg, South Carolina, and large scale projects in Port St. Lucie, Florida that together are expected to bring more than 1,750 homes to that area. (Source: Key Developments)

Valuation Changes for Taylor Morrison Home

- Fair Value: Updated to $66.60 per share, up slightly from $66.43, keeping implied standalone value close to the agreed deal price.

- Discount Rate: Adjusted marginally higher to 9.22% from 9.20%, a small change in the risk assumption used for Taylor Morrison Home.

- Revenue Growth: Now reflects a smaller expected decline of 5.82%, compared with the previous 6.28% decline assumption.

- Net Profit Margin: Trimmed to 6.51% from 7.07%, indicating a more cautious view on future profitability levels for Taylor Morrison Home.

- Future P/E: Raised to 16.35x from 15.22x, implying a slightly higher valuation multiple on expected earnings.

Key Takeaways

- Lower buyer demand and increased reliance on spec home sales are pressuring margins and could constrain future revenue and earnings growth.

- Slower land acquisition and conservative expansion signal the company is prioritizing efficiency over aggressive growth, limiting potential upside.

- Pricing power, product diversification, tech-driven efficiency, strong financial flexibility, and demographic demand trends position the company for stable growth and resilient profitability.

Catalysts

About Taylor Morrison Home- Operates as a land developer and homebuilder in the United States.

- The company's current backlog is down ~30% year-over-year and order activity (net orders) is down 12%, reflecting softening buyer demand despite favorable demographic trends; if this persists, future revenues and earnings growth could fall short of expectations even as current deliveries are supported by high spec inventory.

- An accelerated shift toward spec home sales (71% of Q2 sales, up from 59% YoY) is being driven by consumer desire for discounts in a competitive market; since specs yield lower gross margins than to-be-built homes and require higher incentives, sustained high spec penetration will compress margins and limit future earnings leverage.

- While persistent U.S. housing supply constraints should benefit the industry longer term, Taylor Morrison faces rising cancellations and more selective homebuyer behavior due to macroeconomic uncertainty-suggesting that expected demand "catch-up" from demographic trends may materialize slower than investors anticipate, weighing on top-line growth.

- Company guidance acknowledges that sequential margin moderation is expected into Q3 and likely Q4, and that the cadence of gross margins could remain pressured by continued incentive offers and spec mix, which could undermine consensus expectations for stable or rising profitability.

- The company is prioritizing capital efficiency and returns over volume growth for the near term and plans a slower pace of land acquisition and new community starts-even as it invests in technological tools and digitalization-indicating that operational expansion driven by secular housing demand may be capped, limiting upside to revenue and earnings growth.

Taylor Morrison Home Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

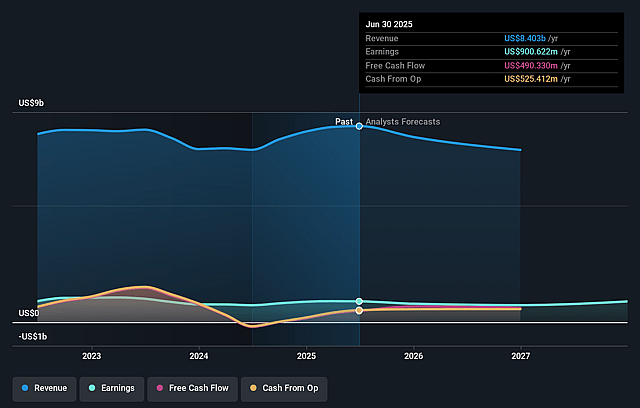

- Analysts are assuming Taylor Morrison Home's revenue will decrease by 5.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 8.8% today to 6.5% in 3 years time.

- Analysts expect earnings to reach $414.1 million (and earnings per share of $5.3) by about June 2029, down from $667.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 16.5x on those 2029 earnings, up from 10.1x today. This future PE is greater than the current PE for the US Consumer Durables industry at 14.3x.

- Analysts expect the number of shares outstanding to decline by 5.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.22%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Taylor Morrison's resilient gross margin performance, which has stayed in the 23–25% range for over two years and is expected to remain in the low-mid 20% range even through elevated incentives and mix shifts, indicates pricing power and operational efficiency that could sustain net margins and earnings.

- The company's well-diversified product portfolio (entry-level, move-up, resort lifestyle/Esplanade, and build-to-rent), focused in core submarkets, positions it to capitalize on broad consumer trends and migration/demographic shifts, supporting stable or growing revenue streams.

- Significant investment in digital sales environments, cost controls, and operational/data analytics is driving SG&A leverage and reducing costs, supporting continued improvement in profit margins and return on equity over time.

- The newly secured $3 billion finance facility with Kennedy Lewis increases financial flexibility, improves balance sheet optionality, and enables Taylor Morrison to optimize returns, hedging against industry cyclicality and supporting long-term earnings growth.

- Underlying housing demand remains fundamentally supported by migration patterns, persistent supply shortages, and favorable demographics (including affluent active adult buyers), suggesting the revenue base and buyer pool are likely to remain robust as confidence returns.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $66.6 for Taylor Morrison Home based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $72.5, and the most bearish reporting a price target of just $49.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $6.4 billion, earnings will come to $414.1 million, and it would be trading on a PE ratio of 16.5x, assuming you use a discount rate of 9.2%.

- Given the current share price of $71.93, the analyst price target of $66.6 is 8.0% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Taylor Morrison Home?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.