Last Update 06 May 26

Fair value Increased 15%GRNT: Higher Fair Value Will Rely On Stronger 2026 Production Outlook

Analysts now see fair value for Granite Ridge Resources at $7.30 per share, up from $6.38, citing updated assumptions for discount rate, revenue growth, profit margin and future P/E, which together point to a higher justified price target.

What's in the News

- Granite Ridge issued new production guidance for 2026, targeting approximately 34,000 to 36,000 Boe per day, with the midpoint described as about 9% above the 2025 level (corporate guidance).

- The company reported fourth quarter 2025 oil production of 1,578 MBbl and natural gas production of 9,918 MMcf, with total net production of 3,231 MBoe and average daily production of 35,120 Boe for the period (announcement of operating results).

- For full year 2025, Granite Ridge reported oil production of 5,855 MBbl and natural gas production of 34,912 MMcf, with total net production of 11,674 MBoe and average daily production of 31,984 Boe (announcement of operating results).

- Kyle Kettler was appointed Chief Financial Officer effective 9 February 2026, while former CFO Kim Weimer continues as Chief Accounting Officer, with Kettler taking responsibility for financial operations and business strategy (executive changes).

Valuation Changes

- Fair Value: Updated analyst fair value has risen from $6.38 to $7.30 per share, reflecting a higher assessed worth for the stock.

- Discount Rate: The assumed discount rate has edged up slightly from 7.04% to 7.13%, implying a marginally higher required return for the valuation model.

- Revenue Growth: Forecast revenue growth has been reduced from 15.14% to 10.35%, pointing to more moderate expectations for future top line expansion in the model.

- Net Profit Margin: The assumed net profit margin has increased from 20.73% to 22.61%, indicating higher expected profitability on each dollar of revenue.

- Future P/E: The future P/E multiple has moved up from 8.0x to 9.1x, signaling a higher valuation multiple being applied to expected earnings.

Key Takeaways

- Strategic acquisitions and a diversified, flexible operating model support sustained growth, resilient cash flow, and high margins amid a favorable U.S. energy market backdrop.

- Focus on disciplined capital allocation and strong liquidity enables growth opportunities while maintaining shareholder returns and reducing structural revenue risk.

- Aggressive acquisition-driven growth and concentration in key basins heighten financial, operational, and regulatory risks amid volatile commodity prices and evolving energy market trends.

Catalysts

About Granite Ridge Resources- Operates as a non-operated oil and natural gas exploration and production company.

- Granite Ridge is actively acquiring high-quality, long-duration inventory at attractive entry prices due to a lack of private equity capital in the upstream oil and gas sector and the increased focus of remaining private capital on larger transactions; this positions the company to capture value from constrained asset supply and will likely support sustained production and revenue growth over the coming years.

- The company's diversified asset base and flexible, non-operating model across multiple premier U.S. basins enables efficient scaling of output with lower operational risk and capital intensity, supporting higher net margins and more resilient free cash flow, particularly as investments in both operated and non-operated partnerships continue to accelerate.

- Ongoing U.S. economic growth, coupled with global energy security concerns and the reshoring of manufacturing, is increasing the value of reliable domestic oil and gas supply-Granite Ridge's U.S.-centric portfolio is well-positioned to benefit from stable demand and potentially favorable pricing, supporting both long-term revenue and asset values.

- Limited progress in commercializing renewables in hard-to-abate industrial sectors means oil and gas will remain a crucial part of the global energy mix for the foreseeable future; this underpins baseline demand for Granite Ridge's products and reduces the risk of structural revenue declines.

- The company's disciplined capital allocation-emphasizing returns over production targets and returning capital via dividends-together with a strong balance sheet and increasing liquidity, provides Granite Ridge with flexibility to pursue growth while protecting net margins and free cash flow, setting the stage for long-term earnings upside as new acquisitions are brought online.

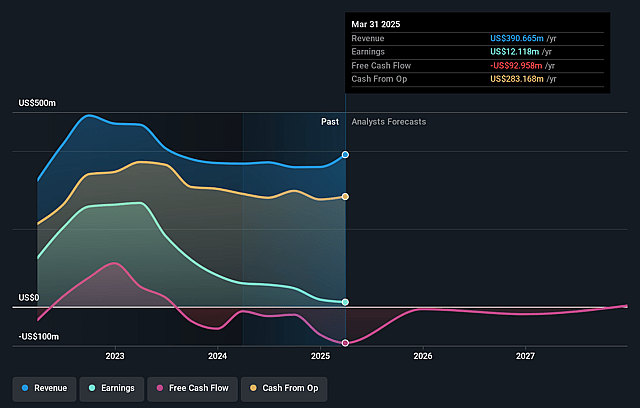

Granite Ridge Resources Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Granite Ridge Resources's revenue will grow by 10.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.8% today to 22.6% in 3 years time.

- Analysts expect earnings to reach $130.0 million (and earnings per share of $1.0) by about May 2029, up from $24.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 9.2x on those 2029 earnings, down from 32.7x today. This future PE is lower than the current PE for the US Oil and Gas industry at 14.7x.

- Analysts expect the number of shares outstanding to grow by 0.27% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.13%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Granite Ridge's significant increase in capital expenditures-outspending operating cash flow and raising leverage to fund acquisitions-introduces heightened balance sheet risk, which, if commodity prices weaken or capital availability tightens, could squeeze free cash flow and limit the company's flexibility to invest for growth or return capital to shareholders.

- Growing reliance on asset acquisitions and operated partnership teams exposes Granite Ridge to concentration risks in key U.S. basins (primarily the Permian and Appalachian), making the company vulnerable to basin-specific regulatory changes, local development challenges, or production declines, all of which could impact long-term revenue and earnings stability.

- As a non-operating and investment-focused energy company, Granite Ridge's production results and operational efficiency are dependent on third-party operating partners; delays, underperformance, or misalignment of incentives with these partners may lead to inconsistent production outcomes, higher costs, and margin pressure over time.

- While management is taking advantage of a constructive acquisition market now, the text acknowledges persistent oil and gas price volatility and recent declines in commodity prices-if these price headwinds persist or worsen, there could be downward pressure on realized prices, revenue growth, and overall profitability.

- The company's bullish approach is predicated on the current scarcity of private capital in upstream oil & gas; however, long-term secular trends-such as the shift to renewables, increased ESG-focused capital restrictions, and potential for stricter environmental regulation-could eventually return capital costs to structurally higher levels or erode hydrocarbon demand, compressing margins and placing downward pressure on share price.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $7.3 for Granite Ridge Resources based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $12.0, and the most bearish reporting a price target of just $5.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $575.0 million, earnings will come to $130.0 million, and it would be trading on a PE ratio of 9.2x, assuming you use a discount rate of 7.1%.

- Given the current share price of $6.11, the analyst price target of $7.3 is 16.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Granite Ridge Resources?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.