Last Update 21 Jul 26

Fair value Increased 13%ICHR: AI And Memory Upswing Will Later Test Fair Valuation

Analyst price targets for Ichor Holdings have moved higher, with the updated fair value estimate rising from $81.71 to $92.29 as analysts factor in higher projected revenue growth, a slightly adjusted discount rate, and ongoing sector commentary around AI related demand and capacity expansion.

Analyst Commentary

Recent Street research on Ichor Holdings points to a cluster of higher price targets and a generally constructive tone around the company, with analysts tying their views to AI related equipment demand, expectations around memory spending, and updated financial models ahead of earnings.

Bullish Takeaways

- Bullish analysts are lifting Ichor Holdings price targets into a US$115 to US$125 range. This is presented as greater conviction in the company’s ability to convert its opportunity set into earnings and cash flow over time.

- Research commentary highlights AI driven demand and capacity constraints in semiconductor equipment, suggesting Ichor could benefit if major equipment makers exercise stronger pricing power and continue to rely on Ichor for key subsystems.

- Some bullish analysts highlight expected support from leading edge foundry investment and what is described as an early stage, multi year DRAM and NAND capacity expansion cycle, which they see as a potential volume driver for Ichor’s larger customers.

- Model updates ahead of earnings indicate that at least some on the Street are revisiting revenue, margin, and cash flow assumptions, which feeds directly into higher fair value estimates for Ichor Holdings.

Bearish Takeaways

- While targets are moving higher, the research cited is tied closely to expectations for AI related demand and memory sector catalysts. This introduces execution risk if customer spending or capacity plans do not match these projections.

- The reliance on major customers like Applied Materials and Lam Research means Ichor’s growth and valuation are exposed to any change in those customers’ order patterns, product roadmaps, or capital spending priorities.

- Higher valuation targets based on multi year capacity expansion assumptions could leave less room for error if margins, pricing, or utilization come in below the levels implied by these models.

- The concentration of commentary around similar positive themes, such as AI demand and memory expansion, suggests that investor expectations may already be leaning optimistic, which can limit upside if execution or sector trends are more mixed than anticipated.

What’s in the News for Ichor Holdings

- Ichor Holdings filed a US$200 million at-the-market follow-on equity offering of ordinary shares, providing the company with the option to raise additional capital over time. Source: Key Developments

- The company issued new guidance for the second quarter of 2026, with expected revenue between US$290 million and US$310 million, and GAAP diluted EPS between US$0.10 and US$0.20. Source: Key Developments

- Ichor Holdings was added to several Russell growth-oriented benchmarks, including the Russell 2000 Growth, Russell Small Cap Comp Growth, Russell 3000E Growth, Russell 2500 Growth, and Russell 3000 Growth indices. Source: Key Developments

- At the same time, Ichor Holdings was removed from multiple Russell value and broader indices, such as the Russell Small Cap Comp Value, Russell Microcap Value, Russell 3000 Value, Russell 3000E Value, Russell Microcap, Russell 3000E, Russell 2500 Value, and Russell 2000 Value benchmarks. Source: Key Developments

Valuation Changes for Ichor Holdings

- Fair Value: The updated fair value estimate has risen, moving from $81.71 to $92.29 per share.

- Discount Rate: The discount rate has edged slightly higher from 11.26% to 11.27%.

- Revenue Growth: The forecast revenue growth rate has increased from 16.50% to 19.24%.

- Net Profit Margin: The assumed net profit margin has eased modestly from 2.41% to 2.25%.

- Future P/E: The forward valuation multiple has moved higher, with the future P/E rising from 110.70x to 125.05x.

Key Takeaways

- Secular demand growth and government incentives are expanding Ichor's market opportunity, supporting above-industry and more predictable long-term revenue growth.

- New proprietary product launches and vertical integration are set to boost margins and diversify revenue through higher content per tool and increased manufacturing efficiency.

- Hiring challenges, weak demand, operational issues, and leadership uncertainty are constraining Ichor's growth, margin expansion, and revenue predictability.

Catalysts

About Ichor Holdings- Engages in the design, engineering, and manufacture of fluid delivery subsystems and components for semiconductor capital equipment in the United States and internationally.

- Ongoing digital transformation in industries such as automotive, healthcare, and industrial automation is driving secular demand growth for advanced semiconductor manufacturing; this is expected to support sustained long-term order growth for Ichor's fluid delivery subsystems, positioning the company for above-industry revenue growth as these trends accelerate.

- The company is making material progress with the qualification and commercialization of new proprietary products like flow controllers and valves, which expand Ichor's addressable market and increase content per tool, providing a foundation for diversified and higher-margin revenues in future quarters as production ramps.

- Vertical integration and ramping of internal manufacturing capacity for critical components are expected to significantly enhance gross margins once hiring and retention issues are resolved-this operational inflection can drive meaningful net margin expansion as new products shift from qualification to scaled commercial production.

- Stronger partnerships and increased direct qualifications with wafer fab equipment OEMs and end device manufacturers are improving recurring order visibility and share of wallet, which should lead to greater earnings predictability in future periods.

- Government incentives for domestic semiconductor production (e.g., US CHIPS Act) continue to underwrite new fab investments and equipment demand in the US, expanding Ichor's customer base and serving as a catalyst for longer-term top line revenue growth.

Ichor Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Ichor Holdings's revenue will grow by 19.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from -5.3% today to 2.3% in 3 years time.

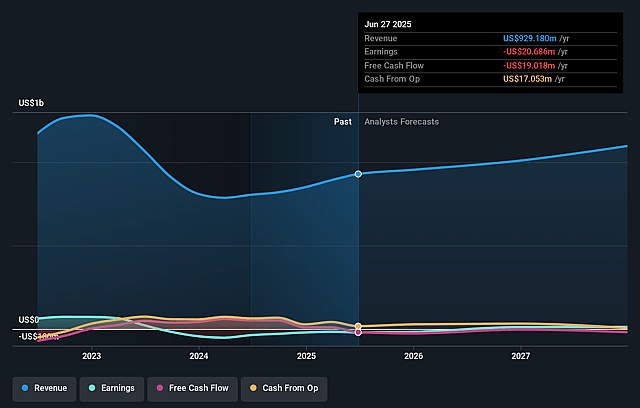

- Analysts expect earnings to reach $36.6 million (and earnings per share of $0.95) by about July 2029, up from -$50.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 125.2x on those 2029 earnings, up from -57.6x today. This future PE is greater than the current PE for the US Semiconductor industry at 57.6x.

- Analysts expect the number of shares outstanding to grow by 1.23% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.27%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent hiring and retention challenges in Ichor's U.S. operations, especially in specialized post-machining and clean room roles, are limiting production capacity and constraining the ramp of internal component supply, restricting both current and potential future revenue growth and delaying needed gross margin expansion.

- Revenue growth momentum has recently stalled below the targeted $250 million quarterly run rate due to external factors such as a slowing EUV build, delayed CapEx investments by a major U.S. semiconductor manufacturer, and ongoing weak demand in nontraditional markets like silicon carbide-which could signal customer and end-market concentration risks resulting in revenue volatility.

- Despite internal progress with new product qualifications (valves and flow control), the timeline for these proprietary, higher-margin products to significantly improve gross margins is unclear and highly dependent on end-customer production ramps and volume adoption, leaving net margins at risk if these transitions are delayed or underwhelming.

- Ichor continues to face thin gross margins (Q2 gross margin at just 12.5%) primarily due to operational execution issues and ongoing external sourcing, with management only cautiously guiding for incremental margin improvement-a condition that exposes the company to heightened downside risk from any further operational, pricing, or cost pressures that could compress net earnings.

- With CEO succession underway and a period of leadership uncertainty, the company may experience execution risk or strategic drift at a critical time when scaling internal supply, securing new product wins, and managing external market slowdowns are all essential, potentially impacting both the predictability of future earnings and investor confidence.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $92.29 for Ichor Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $125.0, and the most bearish reporting a price target of just $60.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.6 billion, earnings will come to $36.6 million, and it would be trading on a PE ratio of 125.2x, assuming you use a discount rate of 11.3%.

- Given the current share price of $83.69, the analyst price target of $92.29 is 9.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Ichor Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.