Last Update 17 Jun 26

NWE: Merger Progress And Infrastructure Pipeline Will Shape Future Risk Reward

Analysts have adjusted their price target on NorthWestern Energy Group, citing a roughly unchanged fair value estimate around $71.42. This reflects perceived benefits from the planned all stock merger with Black Hills, including increased scale, a stronger balance sheet, a broader jurisdictional spread, and a larger long term infrastructure project pipeline.

Analyst Commentary

Recent research commentary around NorthWestern Energy Group centers on the planned all stock merger with Black Hills and how that could shape the combined company's value, balance sheet, and long term project pipeline. While not all reports provide full detail, the themes that do emerge highlight both potential upside and areas where execution will matter for shareholders.

Bullish Takeaways

- Bullish analysts see the all stock merger with Black Hills as adding meaningful scale for NorthWestern Energy Group. They view this scale as supportive of the current fair value framework.

- Commentary points to a stronger combined balance sheet. Bullish analysts link this to improved financial flexibility for funding the long term infrastructure project pipeline.

- The broader jurisdictional spread across multiple service territories is seen as a positive for risk diversification. Some analysts connect this to support for valuation multiples.

- The larger project runway in areas such as data centers, transmission, generation, and gas is viewed as an important source of potential long duration investment. Bullish analysts frame this as helpful for supporting earnings visibility over time.

Bearish Takeaways

- Some cautious analysts focus on integration risk around the all stock merger. They note that execution missteps could affect both cost outcomes and the timing of any expected benefits.

- There is ongoing uncertainty around regulatory outcomes across a broader set of jurisdictions. Bearish analysts view this as a possible constraint on how quickly the combined infrastructure pipeline can be put into the rate base.

- A few cautious views point out that the merger consideration is all stock. This structure may increase sensitivity to share price moves if sentiment weakens ahead of closing.

- Analysts with a more guarded stance highlight that scale and project runway are positives, but they still depend on effective capital allocation and disciplined project execution to justify current fair value estimates for NorthWestern Energy Group.

What’s in the News for NorthWestern Energy Group

- NorthWestern Energy Group reaffirmed its 2026 non GAAP earnings per diluted share guidance range of $3.68 to $3.83. This outlook is supported by a planned $3.2b capital expenditure program over 2026 to 2030 and ongoing progress on the pending all stock merger with Black Hills Corporation, source: company news reports dated June 2, 2026.

- The planned merger with Black Hills Corporation continues to move through approvals. Regulatory clearances have already been obtained in some areas and state hearings are underway, with the transaction aiming to form a combined utility serving over 2.1 million customers with a rate base of about $11b, source: company transaction updates.

- NorthWestern Energy Group, through NorthWestern Corporation, entered into a $225m secured term loan with a bank syndicate and issued related first mortgage bonds. The company is using the proceeds to refinance part of a $425m unsecured revolving credit facility, which increases secured debt while supporting liquidity and refinancing efforts, source: company financing disclosures.

- Federal Energy Regulatory Commission correspondence and delegated orders in early 2026 acknowledged multiple NorthWestern Energy Group dam safety filings on the Missouri Madison Project. These included approvals to proceed with specific construction phases and confirmation that reviewed dams are considered safe for continued operation, source: FERC regulatory filings.

- NorthWestern Energy Group submitted several filings to the Federal Energy Regulatory Commission on transmission tariffs, rate templates, and network service agreements in Montana. The Commission accepted revised tariff records and updated depreciation rates effective January 1, 2026, and granted requested waivers, source: FERC tariff and compliance orders.

Valuation Changes for NorthWestern Energy Group

- Fair Value: The fair value estimate remains unchanged at $71.42, indicating no revision to the central valuation level for NorthWestern Energy Group stock in this update.

- Discount Rate: The discount rate is effectively stable at 7.11%, with only an immaterial rounding difference from the prior figure.

- Revenue Growth: The modeled long term revenue growth assumption is steady at about 4.63%, reflecting no meaningful change in the expected top line growth rate.

- Net Profit Margin: The projected net profit margin remains essentially unchanged at about 14.22%, with only a very small numerical adjustment.

- Future P/E: The future P/E assumption is stable at roughly 20.02x, showing no material shift in the valuation multiple applied to NorthWestern Energy Group earnings.

Key Takeaways

- Accelerating data center demand and legislative reforms are driving strong growth prospects, reduced risks, and greater earnings stability for the company.

- Population growth and regulatory advantages provide a stable, expanding customer base and improved margins through proactive capital investment and flexible service strategies.

- Reliance on coal, regulatory and infrastructure risks, limited diversification, and potential disruption from distributed energy threaten earnings growth and stable returns.

Catalysts

About NorthWestern Energy Group- NorthWestern Energy Group, Inc., doing business as NorthWestern Energy, provides electricity and natural gas to residential, commercial, and various industrial customers.

- NorthWestern is poised to benefit from outsized load growth driven by accelerating data center demand in Montana and South Dakota, which is likely to support above-trend revenue and earnings growth as long-term electrification of industry and digital infrastructure unfolds.

- Recent legislative reform (Montana wildfire liability law and streamlined transmission approvals) meaningfully reduces operational risk and regulatory uncertainty, positioning the company to invest aggressively in grid modernization and transmission upgrades-supporting long-term capital deployment and earnings stability.

- Population growth and migration to the company's service territories (rural and secondary markets) provides a stable and potentially expanding customer base, undergirding consistent cash flow and reducing downside volatility in revenues.

- Near-term resolution of pending rate cases and the ability to retroactively recover certain costs (e.g., Montana rate review impacts, Colstrip facility acquisition filings) are set to improve margins and earnings visibility over the next several years.

- NorthWestern's flexible approach to serving large loads-including FERC-regulated options and utility-owned generation investments-allows for incremental growth opportunities as electrification and power demand for data centers continues to accelerate, supporting both rate base expansion and net margin improvement.

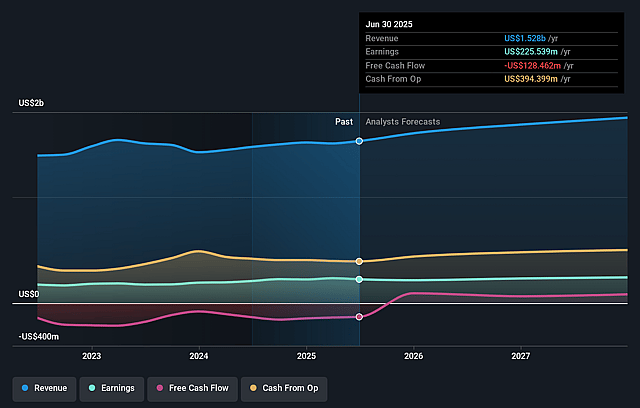

NorthWestern Energy Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming NorthWestern Energy Group's revenue will grow by 4.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.2% today to 14.2% in 3 years time.

- Analysts expect earnings to reach $267.3 million (and earnings per share of $4.28) by about June 2029, up from $167.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 20.3x on those 2029 earnings, down from 25.9x today. This future PE is lower than the current PE for the US Integrated Utilities industry at 20.8x.

- Analysts expect the number of shares outstanding to grow by 0.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- NorthWestern's continued reliance on the Colstrip coal plant and recent acquisitions increasing its coal-fired generation exposure run counter to accelerating state and federal decarbonization policies, which could lead to future regulatory compliance costs, asset impairment risk, or stranded asset scenarios, negatively impacting net margins and long-term earnings.

- The recent decline in quarterly earnings and cash flows compared to prior periods, which management attributes to delayed rate recovery, exposes a vulnerability to regulatory lag and reliance on favorable rate case outcomes-if future state regulatory decisions (particularly for Colstrip cost recovery) are unfavorable, revenue and earnings growth could be significantly curtailed.

- Heavy capital expenditure requirements to modernize aging infrastructure and meet evolving load (including data centers) place sustained pressure on free cash flow and may necessitate higher debt levels, thus increasing interest expense and potentially constraining dividend growth or eroding returns on equity.

- NorthWestern's limited customer and geographic diversification, with key earnings driven by regulatory outcomes in Montana and South Dakota, heightens risk from localized economic downturns, policy changes (such as new Montana property tax legislation), or region-specific operational disruptions, leading to potential volatility in revenue streams and top-line stability.

- Dependence on centralized, utility-owned generation and transmission assets may be undercut over time by broadening adoption of distributed generation, customer-owned renewables, and energy storage, which could gradually reduce monopoly customer load and revenue base, challenging the traditional rate base growth model and pressuring long-term profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $71.42 for NorthWestern Energy Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $78.5, and the most bearish reporting a price target of just $54.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.9 billion, earnings will come to $267.3 million, and it would be trading on a PE ratio of 20.3x, assuming you use a discount rate of 7.1%.

- Given the current share price of $70.56, the analyst price target of $71.42 is 1.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on NorthWestern Energy Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.