Last Update 30 Jun 26

Fair value Increased 7.03%FBIN: New Leadership And Portfolio Review Will Shape Future Shareholder Returns

Analysts have raised the fair value estimate for Fortune Brands to $49.92 from $46.64, citing a lower discount rate, a slightly higher assumed future P/E multiple of 16.32, and recent research pointing to potential portfolio changes under the new CEO as key drivers of the higher price target range.

Analyst Commentary

Recent Street research on Fortune Brands shows a mix of optimism around the leadership change and caution around execution and capital allocation, which feeds directly into how analysts frame valuation and risk.

Bullish Takeaways

- Bullish analysts highlight the appointment of Jesse Singh as CEO as a potential turning point for Fortune Brands, with one upgrade tied directly to the perceived turnaround potential under the new leadership.

- There is specific optimism around the ability to improve core brands such as Moen and Therma-Tru, which some analysts see as key assets that could support a stronger earnings profile over time if execution improves.

- Some bullish views factor in the possibility of portfolio actions affecting as much as two thirds of EBITDA, suggesting room to refine the business mix and potentially support higher valuation multiples if those actions are well executed.

- The move by at least one bullish analyst to substantially increase a price target, while shifting to a more positive rating, reflects a more constructive stance on the risk and reward balance for Fortune Brands under the new CEO.

Bearish Takeaways

- Bearish analysts and those taking a more cautious stance have trimmed price targets, including JPMorgan, which lowered its target to $39 and kept a Neutral rating, signaling limited conviction in near term upside.

- Multiple firms have reduced their price targets, which points to ongoing concerns about execution, capital allocation, and the time and effort required for any turnaround to be reflected in the stock price.

- The cluster of target cuts suggests some analysts remain focused on operational challenges and risk to earnings quality, which may cap how far they are willing to move valuation assumptions, even with a new CEO in place.

- For now, cautious analysts appear to be waiting for clearer evidence of improved performance and portfolio decisions at Fortune Brands before revisiting more constructive P/E or cash flow assumptions.

What’s in the News for Fortune Brands

- Fortune Brands appointed Jesse G. Singh as Chief Executive Officer and member of the Board, effective June 29, 2026. Interim CEO David Barry will move into the Executive Vice President and Chief Operating Officer role. Source, company announcement and regulatory filing.

- Shares of Fortune Brands moved sharply higher after both chambers of Congress passed the bipartisan 21st Century ROAD to Housing Act, legislation designed to cut red tape, streamline environmental reviews, and update manufactured housing rules to support housing supply and builder volumes. Source, recent news report.

- Management, together with the Board, launched a formal strategic review of the Fiberon composite decking business, evaluating multiple alternatives and stating the intent to focus resources on higher return opportunities. Source, company communication.

- Fortune Brands reported that from December 28, 2025 to March 28, 2026, it repurchased 913,091 shares, or 0.76% of shares, for US$43.46 million. This brought total buybacks under the February 6, 2025 program to 3,857,831 shares, or 3.18%, for US$216.22 million. Source, buyback update.

- At the May 5, 2026 annual meeting, shareholders approved an Amended and Restated Certificate of Incorporation that will phase out the classified Board structure over three years. The company also updated full year 2026 guidance, indicating net sales are expected to be down low single digits compared with prior guidance of flat to 2.0%. Source, annual meeting results and guidance update.

Valuation Changes for Fortune Brands

- Fair value was revised to $49.92 from $46.64, indicating a modest uplift in the assessed worth of Fortune Brands shares.

- The discount rate was adjusted slightly lower to 9.70% from 10.21%, reflecting a somewhat reduced required return in the updated model.

- Revenue growth was held essentially steady at 2.56% in both the prior and updated assumptions, suggesting no material change to top line expectations.

- The net profit margin was kept effectively unchanged at about 9.86% in the refreshed estimates, implying a similar earnings efficiency outlook.

- The future P/E moved higher to 16.32x from 15.46x, indicating a somewhat richer multiple assumption applied to Fortune Brands earnings in the updated valuation work.

Key Takeaways

- Tech-enabled product focus and strategic digital investments are driving margin expansion, recurring revenue, and earnings growth.

- Portfolio diversification, brand strength, and operational improvements are positioning the company for sustainable, above-market growth and financial flexibility.

- Heavy reliance on North American housing, slow smart home adoption, and rising costs expose margins to structural risks and limit growth diversification.

Catalysts

About Fortune Brands Innovations- Engages in the provision of home and security products for residential home repair, remodeling, new construction, and security applications in the United States and internationally.

- Fortune Brands is positioned to capture significant growth from increased demand for home renovation and remodeling driven by the aging U.S. housing stock and historically high home equity, supporting long-term revenue expansion as pent-up demand is released.

- The company's strategic investments in digital products-such as connected water management, smart locks, and a new subscription-based recurring revenue model-are enabling a transition toward higher-margin, tech-enabled solutions, driving both improved net margins and earnings growth.

- Robust market share gains and long-term contracts in Water (notably with major builders and retail partners), coupled with strong brand recognition among professional users, are laying the groundwork for sustainable above-market revenue and share growth.

- Portfolio optimization, bolt-on acquisitions (like Yale and Emtek), and diversification into premium luxury and outdoor categories position the company to benefit from urbanization, Sun Belt migration, and increased DIY activity, supporting top-line growth and margin synergies.

- Ongoing operational transformation-moving to an integrated, agile HQ with enhanced supply chain resilience, cost controls, and targeted SG&A savings-is expected to deliver sustained improvement in operating margins and free cash flow, supporting financial flexibility for reinvestment and buybacks.

Fortune Brands Innovations Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Fortune Brands Innovations's revenue will grow by 2.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.1% today to 9.9% in 3 years time.

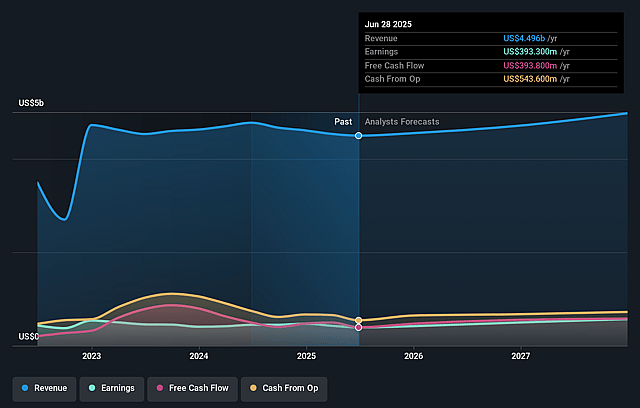

- Analysts expect earnings to reach $472.5 million (and earnings per share of $4.26) by about June 2029, up from $271.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 16.3x on those 2029 earnings, down from 24.1x today. This future PE is lower than the current PE for the US Building industry at 22.7x.

- Analysts expect the number of shares outstanding to decline by 0.62% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.7%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Continued weakness in U.S. housing and remodeling activity presents a structural risk to revenue growth, as management projects flat to declining net sales and notes homebuyers and owners remain hesitant to invest-undermining the view that aging housing or pent-up demand alone will drive meaningful long-term expansion.

- Persistent dependence on North American residential markets makes the company vulnerable to regional housing downturns or macro shocks, which could significantly impact both revenue and earnings; there is little evidence of substantial international diversification to offset this exposure.

- Despite progress in digital/connected business, the connected products run rate is behind initial expectations and described as progressing "broader and a little bit slower," creating uncertainty around Fortune Brands' ability to innovate quickly enough in smart home areas needed to defend or expand margins long-term.

- Margin pressure remains a risk from commodity input costs (e.g., "higher cost inventory," and tariff mitigation relying heavily on supply chain and pricing actions); inability to fully offset future commodity swings or tariff changes may erode gross and operating margins.

- Industry consolidation among large retailers and distributors (e.g., Home Depot, Lowe's, Amazon) could squeeze supplier margins further, and the earnings call suggests that while promotional discipline is a focus, overall pricing power is not guaranteed, especially as the company seeks to balance cost mitigation with volume and channel partner relationships-potentially impacting net margins and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $49.92 for Fortune Brands Innovations based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $70.0, and the most bearish reporting a price target of just $37.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $4.8 billion, earnings will come to $472.5 million, and it would be trading on a PE ratio of 16.3x, assuming you use a discount rate of 9.7%.

- Given the current share price of $54.9, the analyst price target of $49.92 is 10.0% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Fortune Brands Innovations?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.