Last Update 21 Jul 26

Fair value Increased 3.06%RMBS: AI Memory Bandwidth And DOJ Probe Will Shape Future Expectations

Analysts have raised the Rambus fair value estimate to $149.00 from $144.57, citing a slightly lower discount rate, modest adjustments to revenue growth and profit margin assumptions, and updated future P/E expectations following a series of recent price target increases and new coverage.

Analyst Commentary

Recent Street research around Rambus reflects a generally constructive view on the stock, with several bullish analysts lifting price targets and one bearish analyst taking a more cautious stance. Together, these moves help frame how the market is thinking about Rambus valuation, execution risk, and growth potential.

Bullish Takeaways

- Bullish analysts point to Rambus exposure to electronic design automation and related tools as attractive. They highlight a mix of high growth potential and high margins as key drivers in their price target work.

- Several bullish analysts have set or reaffirmed price targets in the US$150 to US$165 range. This suggests they see room between current trading levels and their assessment of where Rambus could be valued based on their models.

- Rambus technology is described by bullish analysts as an important enabler in addressing memory bottlenecks in data centers. They view this as an important factor for long term growth assumptions and for justifying premium P/E expectations.

- Supportive commentary emphasizes the perceived pricing power of Rambus solutions within semiconductor and electronics system design workflows. Analysts view this as helpful for sustaining profitability assumptions in their forecasts.

Bearish Takeaways

- The recent downgrade from a bearish analyst signals concern that Rambus current share price may already reflect optimistic scenarios embedded in recent price target increases. This raises questions about the balance between risk and reward.

- Bearish analysts may see execution risk around capturing the full benefit of Rambus role in solving data center memory bottlenecks. This can affect how much credit they are willing to give the company in valuation models.

- The combination of higher valuation targets and elevated expectations for margins and growth can leave less room for error. Bearish analysts flag this as a source of potential downside if Rambus underperforms those assumptions.

- Some cautious views implicitly highlight that, while sector traits like high margins and strong pricing power are attractive, they can also encourage more competition. This could pressure Rambus growth trajectory if not managed well.

What’s in the News for Rambus

- Rambus introduced a DDR5 9600 Server RDIMM chipset built around its 6th Generation Registering Clock Driver. This is a complete solution aimed at next generation CPU based data center platforms handling AI, high performance computing, and other data intensive workloads. (Source: Company product announcement)

- The company announced a DDR5 9600 Client Memory Module Chipset for CUDIMM, CQDIMM, and CSODIMM modules in future AI PCs, targeting bandwidth of up to 9600 MT/s to support higher performance desktops, notebooks, and workstations. (Source: Company product announcement)

- Rambus launched a SOCAMM2 chipset for LPDDR5X based memory modules in AI server platforms, designed to support JEDEC standard SOCAMM2 modules with LPDDR based server memory operating at up to 9.6 Gb/s. (Source: Company product announcement)

- The company added PCIe 7.0 Switch IP with Time Division Multiplexing to its interconnect portfolio, designed for AI, cloud, and high performance computing systems that require higher bandwidth density, traffic management, and scalability. (Source: Company product announcement)

- Rambus was added to the Russell 1000 Index, Russell 1000 Growth Benchmark, Russell 1000 Dynamic Index, Russell Midcap Index, and Russell Midcap Growth Benchmark, and was removed from several Russell 2000 based indices. This reflects index provider reclassification of the stock. (Source: Index constituent changes)

Valuation Changes for Rambus

- Fair Value: Raised slightly to $149.00 from $144.57, reflecting modest updates to the valuation model.

- Discount Rate: Trimmed slightly to 11.02% from 11.10%, indicating a small adjustment to the risk assumptions used in the Rambus cash flow analysis.

- Revenue Growth: Tweaked slightly to 17.00% from 17.41%, suggesting a marginally more conservative revenue growth assumption in the forecast period.

- Net Profit Margin: Adjusted fractionally to 36.20% from 36.22%, leaving the Rambus profitability profile effectively unchanged in the model.

- Future P/E: Increased moderately to 53.15x from 51.12x, implying a somewhat higher valuation multiple being applied to expected earnings.

Key Takeaways

- Surging AI and data center demand, along with industry shifts like MRDIMM adoption, are expected to drive robust, multi-year growth across Rambus's memory-focused products.

- Strategic expansion into companion chips and a core focus on licensing and semiconductor solutions are enhancing revenue diversification and profit margins.

- Reliance on key memory products, slow diversification, delayed new tech adoption, rising competition, and end-market volatility pose risks to Rambus's revenue growth and profit stability.

Catalysts

About Rambus- Manufactures and sells semiconductor products in the United States, South Korea, Singapore, and internationally.

- Ongoing rapid growth in AI and data center workloads is accelerating the industry's need for high-speed memory interfaces and connectivity, driving demand for Rambus's DDR5, HBM4, and PCIe 7.0 solutions-this positions the company for sustained top-line revenue growth as new design wins and customer qualifications convert into production orders.

- Expansion of Rambus's product portfolio into companion chips (such as power management and client clock drivers) for high-end PCs and next-gen platforms is opening up incremental markets; while initial contributions are modest, management expects revenue from these new products to grow into 2026 and beyond, underpinning future product revenue growth.

- The upcoming industry transition to MRDIMM technology, slated for full-scale adoption beginning in the second half of 2026, will significantly increase the silicon content per module-Rambus is well-positioned to benefit from this shift, which could materially expand its addressable market and drive multi-year revenue growth.

- The company's sharpened focus on a core IP licensing and semiconductor business model is creating more diversified and recurring revenue streams, while supporting structurally higher net margins due to the scalable nature of licensing and improved product mix.

- Strong customer engagement in cutting-edge ASIC and XPU development for AI/ML workloads is boosting demand for customized and off-the-shelf silicon IP, with licensing deals recognized 12–24 months ahead of chip launches; this supports robust medium-term earnings visibility as the next wave of AI accelerators come to market.

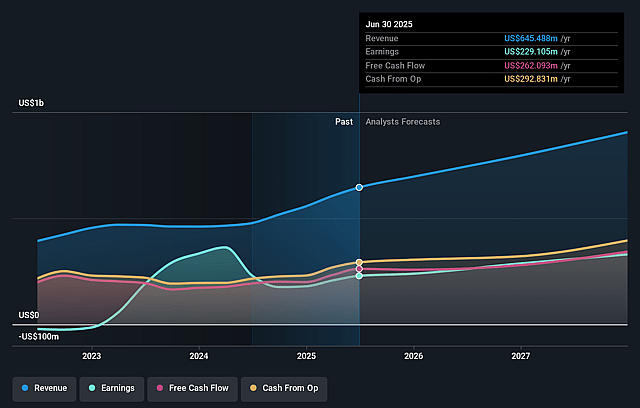

Rambus Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Rambus's revenue will grow by 17.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 31.9% today to 36.2% in 3 years time.

- Analysts expect earnings to reach $418.1 million (and earnings per share of $3.52) by about July 2029, up from $230.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $489.4 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 53.5x on those 2029 earnings, up from 47.4x today. This future PE is lower than the current PE for the US Semiconductor industry at 57.6x.

- Analysts expect the number of shares outstanding to grow by 0.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.02%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy reliance on DDR5 and related high-margin RCD product lines creates concentration risk; if technology transitions stall or alternative memory architectures (like CXL or chiplet-based systems) gain less adoption than expected, Rambus's revenue growth and margins could stagnate or decline.

- Late-stage and still-modest contributions from new companion and power management chips suggest Rambus's transition into diversified product offerings is unproven; if adoption is slower or customer acceptance weaker than predicted, both top-line growth and long-term earnings expansion may fall short.

- Large anticipated market opportunities around MRDIMM and next-gen interfaces such as HBM4 may materialize later than forecasted (2026+), while delayed platform deployments (e.g., CXL 3.0 and client-side PMICs) risk creating gaps in growth and elevating near-to-medium term revenue volatility.

- Increasing market competition-from in-house development by customers, start-ups, and traditional DRAM vendors-could pressure pricing on high-value IP, reduce licensing revenues, and erode Rambus's net margins as more buyers seek alternatives to proprietary memory interface solutions.

- Significant exposure to cyclical end markets (AI, data center, and PC) and dependence on successful execution of multiple new technology ramps makes Rambus vulnerable to industry slowdowns, customer inventory corrections, or shifts in computing architectures, all of which risk lower revenue visibility and potential negative impacts on future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $149.0 for Rambus based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $180.0, and the most bearish reporting a price target of just $100.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.2 billion, earnings will come to $418.1 million, and it would be trading on a PE ratio of 53.5x, assuming you use a discount rate of 11.0%.

- Given the current share price of $100.85, the analyst price target of $149.0 is 32.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Rambus?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.