Last Update 18 Jun 26

Fair value Increased 0.78%KYMR: Future Type 2 Milestones Will Support Oral Degrader Pipeline Potential

Kymera Therapeutics sees its analyst fair value estimate adjusted slightly higher to about $119 per share as analysts incorporate updated views on its discount rate, revenue trajectory, profitability assumptions, and a lower, still very large forward P/E multiple following recent research, including a refreshed price target cut from one firm and new bullish coverage from another.

Analyst Commentary

Recent Street research on Kymera Therapeutics highlights a mix of optimism around the company’s long term opportunity and caution around execution risks and valuation assumptions embedded in the new fair value estimate.

Bullish Takeaways

- Bullish analysts initiating coverage point to a thesis that supports the higher fair value estimate, suggesting confidence that Kymera Therapeutics can support a premium P/E multiple relative to current levels used in recent research.

- Supportive commentary emphasizes the company’s potential to convert its current pipeline into future revenue, which underpins assumptions used in updated revenue trajectories within fair value work.

- Positive views also highlight management’s ability to execute against development milestones, which bullish analysts see as key to justifying the large forward P/E framework applied in their models.

- New bullish coverage is framed around Kymera Therapeutics having enough optionality in its business to support long term growth assumptions that feed into the refreshed fair value estimate.

Bearish Takeaways

- The recent price target cut, including the US$4 reduction from Morgan Stanley, reflects a more cautious stance on how quickly Kymera Therapeutics can deliver on the revenue and profitability path embedded in earlier models.

- More conservative analysts question whether the still very large forward P/E multiple, even after being trimmed, leaves limited margin for error if clinical or commercial execution falls short of expectations.

- Some commentary highlights that valuation remains sensitive to discount rate assumptions and timing of potential cash flows, which could pressure the fair value estimate if inputs are revised again.

- Bearish analysts also flag that any delay in achieving targeted profitability could weigh on sentiment, given the reliance on future earnings in justifying current long term valuation frameworks for Kymera Therapeutics.

What’s in the News for Kymera Therapeutics

- Kymera Therapeutics reported encouraging preclinical data for KT-579 in lupus, showing disease modifying activity and reductions in key lupus biomarkers in multiple models, with the program now in a Phase 1 healthy volunteer trial and initial data planned for the second half of 2026 (source: EULAR, FOCIS, Brookline Capital Markets).

- New Phase 1 data in healthy Japanese adults for KT-621, Kymera Therapeutics’ oral STAT6 degrader, indicated safety and PK/PD results in line with earlier studies, supporting its ongoing global Phase 2b trials in atopic dermatitis and asthma (source: Japanese Dermatological Association Annual Meeting).

- Kymera Therapeutics began patient dosing in the first in human Phase 1 study of KT-485 for hidradenitis suppurativa under its collaboration with Sanofi, which triggered a US$20 million milestone payment to the company (source: KT-485 HS study announcement).

- The U.S. FDA granted Fast Track designation to KT-621 for moderate to severe eosinophilic asthma, aligning with ongoing Phase 2b trials in asthma and atopic dermatitis that are intended to inform later stage studies (source: FDA Fast Track announcement).

- Gilead Sciences exercised its option to exclusively license KT-200, a first in class oral CDK2 molecular glue degrader from Kymera Therapeutics, resulting in a US$45 million milestone payment and potential for up to US$750 million in total payments plus tiered royalties under the collaboration (source: Gilead option exercise announcement).

Valuation Changes for Kymera Therapeutics Stock

- Fair Value: Analyst fair value estimate has risen slightly from $118.27 to about $119.19 per share.

- Discount Rate: Discount rate has fallen slightly from 7.16% to about 7.13%, indicating a modestly lower required return in updated models.

- Revenue Growth: Long term revenue growth assumption reflects a smaller decline, shifting from an 8.82% decline to a 7.35% decline.

- Net Profit Margin: Assumed net profit margin is effectively unchanged, moving fractionally from 19.04% to about 18.98%.

- Future P/E: Future P/E multiple used in the models remains very large but has been trimmed from about 1,959x to roughly 1,886x.

Key Takeaways

- Advancing clinical programs and strategic partnerships could increase market share and positively impact future revenue and earnings.

- Solid cash runway supports focused R&D investments, potentially boosting long-term growth without immediate financing pressures.

- High R&D expenses and reliance on partnerships pose risks to Kymera's long-term financial health and ability to maintain a leadership position in their sector.

Catalysts

About Kymera Therapeutics- Together with its subsidiary, a clinical-stage biopharmaceutical company, focuses on discovering and developing small molecule therapeutics that selectively degrade disease-causing proteins by harnessing the body’s own natural protein degradation system.

- Kymera Therapeutics plans to advance its STAT6 and TYK2 programs into several clinical stages, which could potentially increase future revenue due to the expansion into new treatment markets and therapeutic areas.

- The anticipated Phase II and III trials for their immunology pipeline aim to deliver biologics-like efficacy in oral form, which could enhance net margins by reducing manufacturing costs associated with biologics and potentially capturing a larger market share.

- The collaboration with Sanofi on the IRAK4 program, with expanded Phase II trials, positions Kymera to fast-track toward pivotal trials, potentially accelerating time-to-market and impacting future earnings positively.

- The company's strategy to introduce at least one new IND per year could expand their pipeline steadily, offering opportunities for revenue growth from licensing deals or partnerships.

- With a significant cash runway extending into mid-2027, Kymera can support its R&D activities without immediate pressure for additional financing, allowing focused investment in high-potential programs that could drive long-term earnings growth.

Kymera Therapeutics Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Kymera Therapeutics's revenue will decrease by 7.4% annually over the next 3 years.

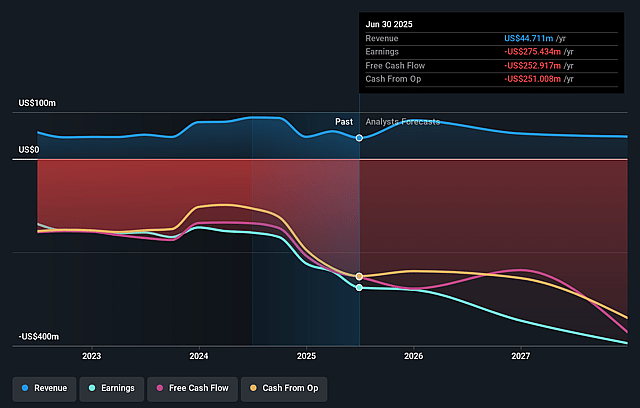

- Analysts are not forecasting that Kymera Therapeutics will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Kymera Therapeutics's profit margin will increase from -611.9% to the average US Biotechs industry of 19.0% in 3 years.

- If Kymera Therapeutics's profit margin were to converge on the industry average, you could expect earnings to reach $7.8 million (and earnings per share of $0.08) by about June 2029, up from -$315.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 1900.2x on those 2029 earnings, up from -23.5x today. This future PE is greater than the current PE for the US Biotechs industry at 16.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.13%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The transition to a video format for financial updates may not significantly impact investor perception or the company’s market value, and does not directly address any operational or financial performance issues.

- Competition in the STAT6 space has increased, which may impact Kymera's ability to maintain its leadership position and could affect future revenue streams.

- Although significant progress is being made with partners like Sanofi, reliance on partnerships exposes Kymera to risks if partners face challenges in advancing clinical trials, potentially impacting future earnings.

- The financial performance shows high R&D expenses with $71.8 million spent in the fourth quarter alone, which could strain resources and impact net margins if new drugs don't reach successful commercialization.

- Despite a significant cash balance, the projected cash runway into mid-2027 suggests that sustained high operational costs could pose a risk to long-term financial health if projected clinical milestones or revenue targets are not met.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $119.19 for Kymera Therapeutics based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $140.0, and the most bearish reporting a price target of just $97.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $40.9 million, earnings will come to $7.8 million, and it would be trading on a PE ratio of 1900.2x, assuming you use a discount rate of 7.1%.

- Given the current share price of $89.9, the analyst price target of $119.19 is 24.6% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Kymera Therapeutics?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.