Last Update 26 Mar 26

Fair value Increased 4.08%ONDS: Epic Fury Counter Drone Demand Will Drive Capital Deployment Success

Narrative Update on Ondas

The analyst price target for Ondas has moved from $18.38 to $19.13 as analysts factor in higher modeled revenue growth, slightly stronger profit margins, and a lower future P/E multiple, while highlighting Ondas as a direct beneficiary of rising demand for low-cost, scalable counter-drone solutions.

Analyst Commentary

Recent research coverage around Ondas is split between enthusiasm for its positioning in counter drone markets and caution about execution and capital use, especially around the latest capital raise and upcoming earnings calls.

Bullish Takeaways

- Bullish analysts point to the recent US$1b registered direct offering as a sign that institutional investors are willing to commit fresh capital at a valuation these analysts view as supportive of higher price targets.

- Several bullish analysts have raised price targets in quick succession, which they link to updated models that assume stronger revenue potential, firmer margin assumptions and a lower modeled P/E, all of which feed into a higher implied equity value.

- Analysts highlighting the impact of Operation Epic Fury see Ondas as a direct beneficiary of growing demand for low cost, scalable counter drone solutions, which they factor into higher long term growth assumptions in their models.

- Some bullish views frame the recent capital raise as feeding a "value generating flywheel." In this framing, the company gains more funding capacity at a valuation level these analysts see as supportive of further business development and possible scale benefits.

Bearish Takeaways

- More cautious analysts stress that several unknowns remain ahead of upcoming calls, including how efficiently the US$1b of new capital will be deployed and how quickly it could translate into revenue and margin performance.

- There is concern that while geopolitical events highlight the need for counter drone solutions, converting this into contracted business and predictable cash flows is not guaranteed, which creates execution risk relative to the higher price targets.

- Some bearish analysts worry that frequent upward adjustments to price targets may run ahead of what is currently visible in financial results, which could leave the stock sensitive to any disappointment on orders, deployment timelines or profitability.

- The larger balance sheet after the capital raise also introduces questions around potential dilution and return on invested capital, with cautious analysts looking for clearer evidence that the increased share count is matched by value creation for existing holders.

What's in the News

- The U.S. Department of Commerce withdrew plans to restrict Chinese made drones, keeping current rules in place for U.S. drone players such as Ondas, AeroVironment and Unusual Machines. (Reuters)

- Ondas, Heidelberg and HD Advanced Technologies formed ONBERG Autonomous Systems, a joint venture aimed at supplying autonomous drone defense and security systems across Germany and Ukraine, with ambitions to serve broader European critical infrastructure and national security needs.

- Palantir, Ondas and World View entered a partnership to develop AI enabled multi domain ISR capabilities, linking stratospheric, aerial and land based autonomous systems using Palantir’s Artificial Intelligence Platform across production, mission planning and edge operations.

- Ondas changed its corporate name from Ondas Holdings Inc. to Ondas Inc. and updated bylaws, equity plans and governance documents to reflect the new name.

- Ondas issued 303,250 Series B Convertible Preferred shares at US$27.70 per share for gross proceeds of US$8,400,025, with dividends accruing at 8% of the original issue price, payable in cash or additional preferred shares when declared.

Valuation Changes

- Fair Value: Updated analyst fair value has risen slightly from $18.38 to $19.13 per share.

- Discount Rate: The modeled discount rate has edged up from 8.07% to 8.10%, implying a modestly higher required return in the valuation model.

- Revenue Growth: Revenue growth assumptions have been marked higher from 173.26% to 185.96%, indicating analysts are now modeling stronger top line expansion.

- Net Profit Margin: The modeled net profit margin has moved from 9.93% to 10.44%, reflecting a small uplift in expected profitability.

- Future P/E: The future P/E multiple has fallen from 208.57x to 90.91x, which reduces the valuation reliance on very high earnings multiples in later years.

Key Takeaways

- Strategic partnerships and expanding defense contracts in various sectors are driving significant revenue growth and market diversification for Ondas Holdings.

- Advancements in autonomous systems and private network technologies are set to enhance operational efficiency, potentially improving margins and financial performance.

- High operating expenses and debt reliance are challenges, with conservative revenue expectations and volatile margins posing risks to future profitability and growth.

Catalysts

About Ondas Holdings- Provides private wireless, drone, and automated data solutions in the United States and internationally.

- Ondas anticipates record revenue growth in 2025, primarily driven by Ondas Autonomous Systems (OAS), due to significant backlog and expanding programs with Optimus and Iron Drone systems in defense and homeland security sectors. This will directly impact revenue.

- The strategic partnership with Palantir Technologies aims to leverage advanced AI capabilities to enhance operational efficiencies and scale OAS’s operations, which is expected to support the revenue ramp and broaden their customer base, influencing earnings and margins through improved operational scale.

- The expansion of OAS’s market presence, with increased customer engagement and government contracts in defense sectors in Israel and the UAE, is set to secure additional military customers, suggesting potential revenue growth and improved market diversification.

- Expected improvements in operating leverage as revenues grow, particularly at OAS, are set to recover gross margins, which could reach 50% or better in the second half of 2025, impacting net margins positively.

- Continued strategic value building at Ondas Networks and progress in private wireless network technologies for rail operations, which includes 900-megahertz network rollouts and new product opportunities, aims to unlock further revenue streams and bolster financial performance.

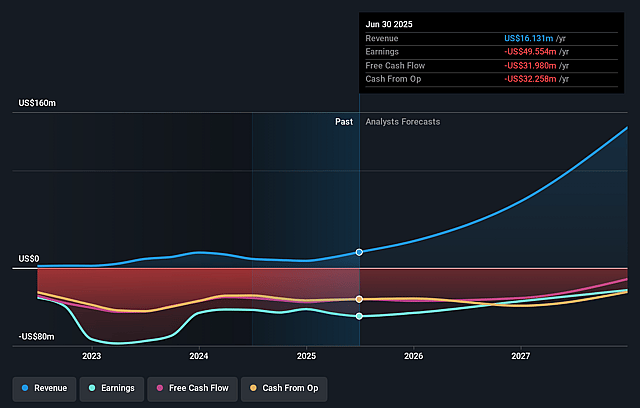

Ondas Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Ondas's revenue will grow by 186.0% annually over the next 3 years.

- Analysts are not forecasting that Ondas will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Ondas's profit margin will increase from -270.4% to the average US Communications industry of 10.4% in 3 years.

- If Ondas's profit margin were to converge on the industry average, you could expect earnings to reach $123.8 million (and earnings per share of $0.27) by about March 2029, up from -$137.2 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 91.0x on those 2029 earnings, up from -35.1x today. This future PE is greater than the current PE for the US Communications industry at 43.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.1%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ondas Holdings faced challenges in 2024, such as extending timelines at Ondas Networks and disruptions due to military activity in Israel, which could impede future revenue growth if similar issues recur.

- The company's revenue expectations for 2025 remain conservative at $25 million, with uncertainties related to Ondas Networks affecting the potential for revenue expansion.

- Gross margins are expected to be volatile due to the early stages of platform adoption and shifts in revenue mix, which may impact net margins and profitability.

- As of 2024, Ondas Holdings reported high operating expenses and adjusted EBITDA loss, with existing revenues not covering these expenses, posing a risk to future earnings if revenue growth does not accelerate as projected.

- The $52 million in debt outstanding and reliance on raising additional funds or extending debt terms might impact the company's financial health and its ability to invest in growth initiatives.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $19.12 for Ondas based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $25.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.2 billion, earnings will come to $123.8 million, and it would be trading on a PE ratio of 91.0x, assuming you use a discount rate of 8.1%.

- Given the current share price of $10.31, the analyst price target of $19.12 is 46.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Ondas?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.