Last Update 17 May 26

Fair value Decreased 8.44%DT: Activist Margin Push And AI Alliance Will Support Future Upside

Analysts have revised their fair value estimate for Dynatrace from about $47.84 to $43.80, reflecting updated assumptions that blend slightly higher expected revenue growth with a lower profit margin outlook and a more conservative future P/E of roughly 32.23 compared with 35.81 previously.

What's in the News

- Issued guidance for the first quarter of fiscal 2027, with expected total revenue between US$547 million and US$551 million. (Corporate guidance)

- Issued full fiscal 2027 guidance, with expected total revenue between US$2.317b and US$2.335b. (Corporate guidance)

- Reported an impairment of long-lived assets of US$18.525 million for the quarter ended March 31, 2026. (Impairment disclosure)

- Starboard Value LP disclosed a significant stake and is pushing for margin expansion, faster share buybacks, and openness to options aimed at maximizing shareholder value. (Activist communication)

- Expanded its alliance with Postman, making the Dynatrace Model Context Protocol Server available in the Postman API Network so developers can access real-time observability data directly in AI-assisted API workflows. (Client and product announcement)

Valuation Changes

- Fair Value: revised down from $47.84 to $43.80, a reduction of about 8% in the estimated intrinsic value per share.

- Discount Rate: nudged higher from 8.47% to 8.52%, implying a slightly higher required return for valuing future cash flows.

- Revenue Growth: adjusted up from 13.99% to 14.68%, reflecting a slightly stronger top line growth assumption in the model.

- Net Profit Margin: reduced from 17.52% to 15.69%, indicating a more cautious view on future profitability.

- Future P/E: brought down from 35.81x to 32.23x, pointing to a less generous valuation multiple applied to future earnings.

Key Takeaways

- AI-powered observability and a unified platform are deepening customer integration, driving product adoption, and supporting strong gross margins and recurring revenue.

- Targeted go-to-market changes and value-based pricing are generating a higher-quality sales pipeline, positioning for sustained revenue growth and improved customer retention.

- Competitive pressures, customer concentration, longer sales cycles, global risks, and dependence on continued AI innovation all threaten Dynatrace's growth, pricing, and market relevance.

Catalysts

About Dynatrace- Engages in the advancement of observability for digital businesses, which transforms the complexity of modern digital ecosystems in North America, Europe, the Middle East, Africa, the Asia Pacific, and Latin America.

- Dynatrace is well positioned to capture incremental share of the expanding addressable market created by enterprises accelerating digital transformation and cloud modernization initiatives, as evidenced by multi-million dollar, end-to-end observability deals and a pipeline heavily weighted toward large, strategic consolidations-catalyzing sustained revenue growth and increased average ARR per customer over time.

- Investments in AI-driven observability-including significant advancements in agentic AI and integration of predictive, causal, and generative AI-are increasing differentiation and embedding Dynatrace more deeply into enterprise IT operations, which enhances pricing power and supports gross margin stability.

- The company's unified platform approach, particularly the growing success of Grail-powered log management (over 100% YoY log consumption growth and targeting $100M in annualized consumption), is driving multi-product adoption and higher customer stickiness, which should improve net retention rates, recurring revenue, and long-term earnings predictability.

- Recent go-to-market strategy changes (focusing sales coverage on strategic, high-propensity-to-spend accounts and building out strike teams for key product areas) are yielding a substantially larger and higher quality expansion pipeline (pipeline for deals >$1M more than doubled YoY), positioning Dynatrace for accelerated revenue and earnings growth from existing customers.

- The ongoing shift in the industry toward value-based, consumption-driven pricing models-with Dynatrace's DPS contracts now accounting for 65% of ARR and driving higher platform adoption and faster consumption-supports higher long-term revenue growth, improved customer lifetime value, and the potential for margin expansion.

Dynatrace Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

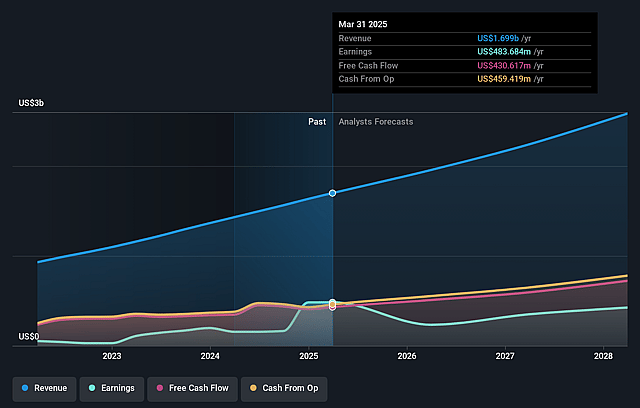

- Analysts are assuming Dynatrace's revenue will grow by 14.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.1% today to 15.7% in 3 years time.

- Analysts expect earnings to reach $477.7 million (and earnings per share of $1.59) by about May 2029, up from $162.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 32.2x on those 2029 earnings, down from 69.5x today. This future PE is greater than the current PE for the US Software industry at 28.3x.

- Analysts expect the number of shares outstanding to decline by 2.27% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.52%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition from both hyperscalers (like AWS, Azure, Google Cloud) and other best-of-breed observability vendors, along with the risk of commoditization of basic observability tools and the increasing adoption of open-source alternatives (such as OpenTelemetry and Prometheus), could pressure Dynatrace's pricing power, erode its market share, and negatively impact both revenue growth and net margins over time.

- Growing deal sizes and increasing reliance on large, strategic enterprise expansions focus the company on fewer, higher-value opportunities, introducing timing variability and customer concentration risk; delays or churn in these deals could lead to significant volatility in revenues and earnings.

- The shift towards integrated end-to-end observability platforms is creating larger, multi-faceted sales motions, which, while beneficial for account growth, also result in longer deal cycles and higher execution risk-if Dynatrace fails to close these deals at expected rates, or if customers defer or reduce IT spend due to macroeconomic uncertainty, revenue and ARR growth could be negatively impacted.

- Heavy weighting of expenses in euros and global operations expose Dynatrace to ongoing foreign exchange headwinds, geopolitical instability, and regulatory fragmentation (such as data sovereignty laws), all of which could limit the company's ability to scale efficiently across global markets and compress margins.

- While current traction in AI observability and log management is strong, the company's long-term success is highly dependent on continued rapid innovation in AI-driven automation and agentic AI; if Dynatrace cannot keep up with the fast pace of technological evolution or fails to broaden adoption as AI adoption patterns shift, product irrelevance or disintermediation could cause deterioration in revenues and future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $43.8 for Dynatrace based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $52.0, and the most bearish reporting a price target of just $36.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $3.0 billion, earnings will come to $477.7 million, and it would be trading on a PE ratio of 32.2x, assuming you use a discount rate of 8.5%.

- Given the current share price of $38.36, the analyst price target of $43.8 is 12.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Dynatrace?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.