Last Update 25 Jun 26

Fair value Increased 0.51%ADM: Policy Support And Margins Will Likely Keep Shares Fairly Valued

Archer-Daniels-Midland’s analyst price target has been adjusted modestly higher to about $74.60, with analysts pointing to updated fair value estimates, slightly revised revenue growth and profit margin assumptions, and refreshed P/E expectations following a series of recent price target increases across major firms.

Analyst Commentary

Recent Street research on Archer-Daniels-Midland centers on a cluster of price target revisions and regulatory developments, giving investors a clearer picture of how analysts are thinking about valuation, growth prospects, and execution risk around the stock.

Bullish Takeaways

- Bullish analysts have raised price targets across multiple research shops, which signals growing confidence that Archer-Daniels-Midland’s current valuation may not fully reflect their updated fair value estimates.

- Several of the new targets, including the larger upward revisions cited by firms such as UBS and Jefferies, point to a view that Archer-Daniels-Midland can support higher P/E assumptions than previously modeled, based on refreshed expectations for the business mix.

- Street commentary linking the EPA’s final RFS volume mandates to Archer-Daniels-Midland suggests that policy support for renewable fuels is being treated as a positive factor in revenue and margin frameworks for the company’s biofuels and related operations.

- Incremental increases in targets from major banks like JPMorgan are being interpreted by bullish analysts as validation that Archer-Daniels-Midland is executing well enough for them to revisit prior, more conservative scenarios in their models.

Bearish Takeaways

- Even as targets move higher, some bearish analysts remain cautious that the updated price levels could already embed optimistic assumptions on execution, leaving less room for upside if Archer-Daniels-Midland falls short of revised expectations.

- The reliance on regulatory support, such as the EPA’s RFS volume mandates, introduces a policy risk that more conservative analysts flag as a constraint on valuation, since future rule changes could affect revenue and margin trajectories.

- Smaller step ups in price targets from certain firms indicate that not all analysts are comfortable assigning materially higher P/E multiples to Archer-Daniels-Midland, which can limit how far they are willing to move their fair value estimates.

- Bears also point out that a wave of target increases in a short period can reflect model recalibration more than new fundamental information, which may reduce the signal value of the revisions for long term investors focused on sustained execution.

What’s in the News for Archer-Daniels-Midland

- Archer-Daniels-Midland stock reached a 52 week high of $83.20 after the company reported Q1 2026 adjusted EPS of $0.71, which was above analyst expectations, while revenue was below forecasts, according to Zacks.

- The company raised its full year adjusted EPS guidance, citing operational performance and margin conditions in Carbohydrate Solutions and Nutrition that offset challenges in Ag Services & Oilseeds. Zacks noted roughly 12% upward revisions in earnings estimates over the past quarter.

- Zacks reported that Archer-Daniels-Midland holds a Zacks Rank #2 (Buy) and a top EPS Revision Grade of A+ in its sector, with year to date stock return of about 39.2% compared with its Consumer Staples peers.

- UBS increased its Archer-Daniels-Midland price target to $95. Some valuation concerns have been raised around insider selling of about $8.4 million and an elevated P/E ratio, as highlighted by GF Value, according to the Zacks coverage.

- Illinois Governor J.B. Pritzker announced that Archer-Daniels-Midland plans to invest $103 million to modernize its Decatur, Illinois operations. The project is expected to create 50 new full time jobs, retain over 1,000 existing jobs, and upgrade soybean plants and the corn wet mill with new control technology.

- Archer-Daniels-Midland filed an answer with the Federal Energy Regulatory Commission in the Northern Natural Gas Company proceeding, seeking confirmation that its earlier Notice to Withdraw opposition to a settlement was effective as of June 6, 2026, and requesting that it no longer be listed as a contesting party.

Valuation Changes for Archer-Daniels-Midland

- Fair Value: Updated slightly higher from $74.22 to about $74.60, reflecting a modest upward adjustment in the central valuation estimate.

- Discount Rate: Held effectively steady at about 7.11%, indicating no meaningful change in the rate used to discount Archer-Daniels-Midland cash flow assumptions.

- Revenue Growth: Trimmed marginally from about 3.77% to roughly 3.76%, signaling a very small downward tweak to long term growth assumptions.

- Profit Margin: Raised slightly from about 2.59% to roughly 2.60%, pointing to a modestly more optimistic view on Archer-Daniels-Midland long run profitability.

- Future P/E: Adjusted fractionally higher from about 19.02x to roughly 19.03x, suggesting only a minimal change in the projected earnings multiple applied in the valuation work.

Key Takeaways

- Policy and regulatory support for biofuels and ramping up production facilities will directly improve margins and profitability across ADM's key business segments.

- Cost management, network optimization, and innovation in Nutrition are lowering the cost base and enabling stable, higher-margin growth aligned with global demand trends.

- ADM faces ongoing earnings volatility and margin pressure from regulatory uncertainty, declining demand, operational headwinds, and heightened compliance and reputational risks.

Catalysts

About Archer-Daniels-Midland- Engages in the procurement, transportation, storage, processing, and merchandising of agricultural commodities, ingredients, flavors, and solutions in the United States, Switzerland, the Cayman Islands, Brazil, Mexico, Canada, the United Kingdom, and internationally.

- Policy clarity and ongoing government support for biofuels-including the extension of the 45Z tax credit, favorable RVOs, and domestic feedstock incentives-are expected to drive increased soybean oil demand and improved crush margins, directly supporting ADM's revenue and net margins from late 2025 into 2026.

- ADM's ramp-up of key production facilities, notably the Decatur East plant, will eliminate significant cost headwinds experienced in prior quarters and restore higher-margin specialty ingredient capacity, enhancing overall Nutrition segment profitability and net margins moving forward.

- Strategic network optimizations, cost management initiatives (targeted $500–$750 million savings over 3–5 years), and focus on portfolio simplification are structurally lowering ADM's cost base and setting up for sustained improvements in operating earnings and return on invested capital.

- Growth in the Nutrition segment-driven by geographic expansion, innovation in probiotics and flavors, and the shift to higher-margin specialty and health ingredients-aligns with changing consumer preferences for processed and convenience foods, providing ADM with a path to higher revenue growth and greater margin stability.

- ADM's integrated model and strong balance sheet position it to capitalize on global demand growth, especially across Asia and Africa, as population and income trends drive higher consumption; this supports long-term volume gains and earnings expansion.

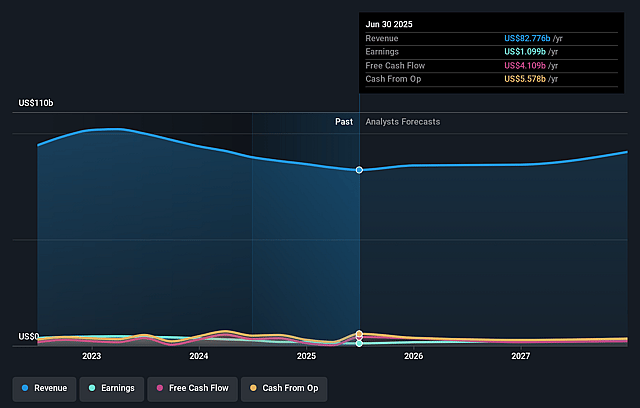

Archer-Daniels-Midland Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Archer-Daniels-Midland's revenue will grow by 3.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.3% today to 2.6% in 3 years time.

- Analysts expect earnings to reach $2.3 billion (and earnings per share of $4.86) by about June 2029, up from $1.1 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 19.1x on those 2029 earnings, down from 33.5x today. This future PE is greater than the current PE for the US Food industry at 15.9x.

- Analysts expect the number of shares outstanding to grow by 0.31% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent uncertainty and frequent changes in biofuel policy and regulatory clarity, including timing issues with Renewable Volume Obligations (RVOs) and biofuel tax credits, may continue to cause earnings volatility and limit ADM's ability to fully capitalize on uplifted margins, impacting long-term margin stability and earnings growth.

- Declining margins and volumes in core Ag Services & Oilseeds (AS&O) and Carbohydrate Solutions segments, driven by trade policy uncertainty, lower global commodity prices, currency fluctuations, and reduced demand for traditional agricultural commodities, represent structural risks to ADM's revenue base and net margins.

- Climate

- and crop-related challenges-such as ongoing corn quality issues in EMEA and greater input cost volatility-threaten reliable supply chains and margin performance, leading to potential headwinds for revenue and increased operational costs.

- Shifting consumer preferences and softening demand in key end markets, such as high fructose corn syrup and certain paper/starch applications, coupled with strategic exits from "non-core" facilities, may reduce ADM's scale advantages and long-term revenue prospects in traditional lines.

- Residual risks from recent internal control material weaknesses and past regulatory scrutiny increase the likelihood of elevated compliance costs or reputational impacts, potentially weighing on net earnings and investor confidence over the longer term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $74.6 for Archer-Daniels-Midland based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $95.0, and the most bearish reporting a price target of just $58.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $90.0 billion, earnings will come to $2.3 billion, and it would be trading on a PE ratio of 19.1x, assuming you use a discount rate of 7.1%.

- Given the current share price of $75.08, the analyst price target of $74.6 is 0.6% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Archer-Daniels-Midland?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.