Last Update 05 Jun 26

Fair value Increased 6.11%WT: Private Asset ETFs And AI Automation ETFs Will Shape Future Returns

Analysts have raised their price target on WisdomTree by about $1.15 per share to around $20. This change reflects updated assumptions for revenue growth, profit margins, the discount rate and future P/E multiples.

What's in the News

- CEO Jonathan Steinberg outlined plans to expand into ETFs tied to private assets, including a commodities ETF with exposure to WisdomTree farmland holdings and an equity ETF with venture capital exposure targeted for early 2027. He also urged advisors to be cautious about evergreen fund structures due to liquidity and fee concerns. [Source: CEO interview]

- WisdomTree launched the Physical AI, Humanoids, and Drones Fund (WDRN), an ETF tracking the WisdomTree Physical AI, Humanoids, and Drones Index, providing exposure to global companies involved in robotics, drones, smart manufacturing, logistics automation, and other physical AI applications. [Source: company announcements]

- The company reported Q1 results with revenue growth of 47.5% year on year, nearly US$6b in net inflows across asset classes and regions, and a 13.2% share price gain following the earnings release. [Source: earnings reports]

- WisdomTree is expanding its capital efficient ETF suite with new funds such as the Efficient Rare Earth Plus Strategic Metals Fund (WDIG), the Efficient U.S. Plus International Equity Fund (NTSD), and adaptive moving average ETFs WAMA and WIMA. These products blend equities with futures or Treasury bills using rules based approaches. [Source: company announcements]

- Partnerships with Stable Sea and Halo Investing are broadening WisdomTree’s footprint in tokenized money market funds and structured income SMA strategies, giving businesses and advisors more ways to access tokenized treasuries and defined outcome income products within established platforms. [Source: company and partner announcements]

Valuation Changes

- Fair Value: revised from $18.82 to $19.97, a modest upward adjustment to the estimate per share.

- Discount Rate: reduced slightly from 8.74% to 8.59%, reflecting a small change in the required return used in the model.

- Revenue Growth: assumption increased from 15.99% to 18.42%, indicating a higher expected growth rate for revenue in the forecast period.

- Net Profit Margin: assumption raised from 27.13% to 33.48%, pointing to a higher projected level of profitability on future earnings.

- Future P/E: terminal P/E multiple adjusted from 14.01x to 14.43x, a slight increase in the valuation multiple applied to later year earnings.

Key Takeaways

- Growth is driven by expansion into private assets, international markets, digital finance, and alternative investment products, supporting revenue diversification and margin improvement.

- Innovative offerings in blockchain, tokenized assets, and wealth management position the company to capture emerging opportunities and deepen distribution channels.

- Rising competition, fee compression, and regulatory risks threaten WisdomTree's growth, revenue predictability, and profitability across both traditional and digital asset segments.

Catalysts

About WisdomTree- Through its subsidiaries, operates as an exchange-traded funds (ETFs) sponsor and asset manager.

- The acquisition of Ceres Partners positions WisdomTree to capitalize on growing investor demand for private market and alternative asset exposures, particularly in underpenetrated, income-generating sectors like U.S. farmland, supporting future AUM and fee revenue growth.

- WisdomTree's early investments in blockchain, tokenization, and stablecoin-powered digital asset infrastructure are enabling new product and revenue streams (such as tokenized funds and scalable net interest income), aligning them with the expanding adoption of digital finance, which is likely to boost both top line and margin expansion.

- The continued global shift from active to passive investing remains a powerful driver for WisdomTree's core ETF business, as evidenced by broad-based net inflows, growing international scale, and record AUM, which should translate to higher revenue and improved operating leverage.

- Successful international expansion, particularly in Europe, is driving strong organic growth via differentiated products (like the European Defense Fund), boosting cross-regional flows and deepening the company's distribution reach, supporting sustained earnings growth and improvement in net margins.

- Robust model portfolio and direct indexing initiatives (including the Quorus partnership) demonstrate the firm's capacity to capture new wealth management trends and distribution channels, likely further diversifying revenue streams and stabilizing or expanding net margins.

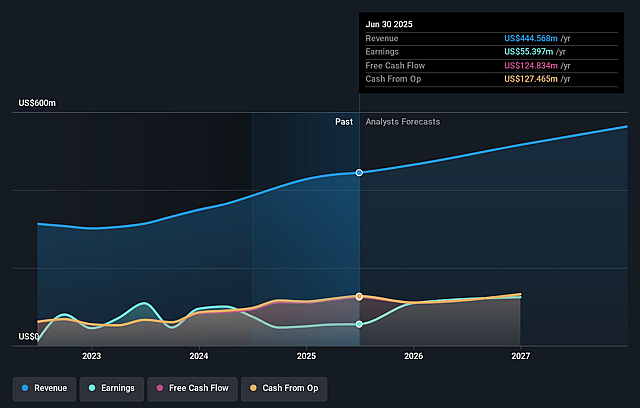

WisdomTree Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming WisdomTree's revenue will grow by 18.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.1% today to 33.5% in 3 years time.

- Analysts expect earnings to reach $303.1 million (and earnings per share of $1.4) by about June 2029, up from $60.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.5x on those 2029 earnings, down from 46.9x today. This future PE is lower than the current PE for the US Capital Markets industry at 39.1x.

- Analysts expect the number of shares outstanding to grow by 4.64% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.59%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Farmland as an asset class may face long-term headwinds from rising investor preference for more liquid or scalable private market alternatives (such as private credit or infrastructure) and increasing competition as other asset managers enter the space, potentially slowing WisdomTree's AUM growth and diversification benefits, which could limit future revenue and fee expansion.

- Heavy reliance on performance fees from the farmland fund exposes WisdomTree to volatility in agricultural land pricing, unpredictable mark-to-market events, and macroeconomic risks (such as changing commodity prices, climate impact, or interest rate changes), which could negatively impact the predictability of future revenues and net earnings.

- Ongoing industry-wide fee compression, driven by the proliferation of ultra low-cost or zero-fee investment products and increasing transparency around investment costs, threatens WisdomTree's revenue per asset managed and long-term net margins-especially as ETF and model portfolio markets become more commoditized.

- Significant investment and optimism around digital assets and stablecoin initiatives may carry execution and regulatory risk; if demand for tokenized assets or stablecoins fails to scale, or if tough new regulations emerge, WisdomTree could face subpar returns on invested capital and lower or negative contribution to earnings from these segments.

- Potential for industry consolidation or increased competition from larger global asset managers-who may eventually enter or scale-up in both farmland and digital asset markets-threatens WisdomTree's market share, pricing power, and ability to maintain above-average revenue growth, putting longer-term pressure on both top-line and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $19.97 for WisdomTree based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.0, and the most bearish reporting a price target of just $16.8.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $905.2 million, earnings will come to $303.1 million, and it would be trading on a PE ratio of 14.5x, assuming you use a discount rate of 8.6%.

- Given the current share price of $18.97, the analyst price target of $19.97 is 5.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on WisdomTree?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.