Last Update 20 May 26

Fair value Increased 3.61%VLO: Higher Oil Assumptions And Mixed Ratings Will Shape But Limit Future Upside

Analyst fair value estimates for Valero Energy have shifted up by about $9 to $256, with the change framed around a higher assumed future P/E of roughly 15x, as well as recent rounds of price target increases across several firms, offset in part by a few new cautious ratings.

Analyst Commentary

Recent research on Valero Energy has been active, with several firms adjusting price targets and a few shifting ratings. The mix of views gives you a sense of where analysts see valuation support and where they see risks around execution and the operating backdrop.

Bullish Takeaways

- Bullish analysts have raised price targets multiple times over the recent period. This lines up with the higher assumed P/E of about 15x used in fair value work and suggests they see support for a richer earnings multiple than before.

- Some bullish analysts have tied higher targets to updated commodity price assumptions, including oil price outlooks. These feed directly into revenue and margin expectations for a refiner like Valero.

- Several research notes indicate that, even after earlier equity performance, bullish analysts still see room within their valuation models to lift targets. This points to confidence in the company’s ability to execute on its plan.

- Goldman Sachs raised its target into the low US$200s while keeping a positive rating. This signals that at least one large global firm still views the risk or reward balance as attractive at higher valuation levels.

Bearish Takeaways

- At the same time, some bearish analysts have either downgraded the stock or assigned more cautious ratings. This indicates concern that the share price already reflects much of the near term upside implied by recent target moves.

- One firm resumed coverage with a Sell rating, highlighting that not all analysts agree with the higher P/E and suggesting that, for more conservative models, current valuation leaves limited buffer against weaker refining margins or lower utilization.

- Removal of Valero from a major firm’s US Conviction List shows a shift in conviction level, even though that firm still maintains a Buy rating. You can read this as a more measured stance on execution and sector positioning.

- A handful of cautious ratings alongside higher targets underscore a key tension in the research. Valuation support relies heavily on commodity and margin assumptions that may not play out exactly as modeled.

What's in the News

- The European Union is preparing measures to address a jet fuel shortage linked to the Iran war, which could matter for Valero because jet fuel is a key refined product and any supply constraints or trade shifts can affect refining flows and pricing (Reuters).

- Arnold & Itkin LLP filed a lawsuit against Valero Energy in Jefferson County, Texas, on behalf of a worker injured after an explosion and fire at the Port Arthur refinery on March 23, 2026. The suit includes allegations of failure to provide a safe working environment and claims for punitive damages tied to alleged gross negligence.

- From October 1, 2025 to December 31, 2025, Valero repurchased 6,247,449 shares for US$1,061.5m, representing 2.05% of its shares. This brought total buybacks under the program announced on September 15, 2023 to 36,938,538 shares, or 11.57%, for US$5,629.68m.

Valuation Changes

- Fair Value: Updated estimate has risen from $247.33 to $256.26, an increase of about 3.6%.

- Discount Rate: Assumed discount rate has edged up from 6.98% to 7.11%, indicating a slightly higher required return in the model.

- Revenue Growth: Long term revenue growth assumption has shifted from a mild decline of about 2.02% to a steeper decline of about 141.95%, implying a much more conservative view on future dollar revenue levels.

- Net Profit Margin: Net profit margin input has eased from roughly 4.93% to 4.77%, a small reduction in expected profitability per dollar of revenue.

- Future P/E: Assumed future P/E has increased from about 13.79x to 15.13x, indicating a higher earnings multiple used in the updated valuation work.

Key Takeaways

- Strategic investments and a strong balance sheet may boost future earnings through growth and higher-value product yields.

- Shareholder returns could improve from increased dividends and buybacks, while renewable diesel segment earnings benefit from market factors.

- Asset impairments, renewable segment struggles, operational cost pressures, and regulatory uncertainties threaten Valero's financial stability and profitability.

Catalysts

About Valero Energy- Manufactures, markets, and sells petroleum-based and low-carbon liquid transportation fuels and petrochemical products in the United States, Canada, the United Kingdom, Ireland, Latin America, Mexico, Peru, and internationally.

- The SEC unit optimization project at St. Charles, expected to start up in 2026, is projected to increase the yield of high-value products, potentially boosting future revenues and earnings.

- Anticipated tight product supply and demand balances, with low product inventories, are expected to support refining fundamentals during the driving season, possibly enhancing refining margins and revenues.

- A strong balance sheet and $5.3 billion of available liquidity provide Valero with operational and financial flexibility to invest in growth and optimization projects, potentially improving future earnings.

- The potential for higher D4 RIN prices and an increase in the RIN obligation could positively impact the renewable diesel segment's earnings by improving margins.

- Continued commitment to capital discipline and shareholder returns, such as the 6% increase in the quarterly cash dividend, could support per-share earnings growth through ongoing share buybacks.

Valero Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

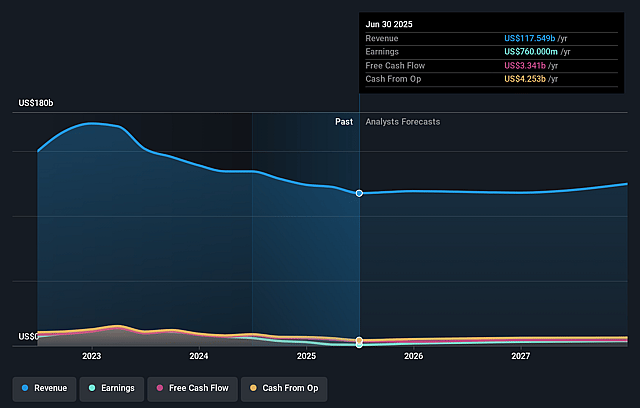

- Analysts are assuming Valero Energy's revenue will decrease by 1.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.6% today to 4.8% in 3 years time.

- Analysts expect earnings to reach $5.4 billion (and earnings per share of $22.51) by about May 2029, up from $4.2 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $7.1 billion in earnings, and the most bearish expecting $4.0 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.1x on those 2029 earnings, down from 18.6x today. This future PE is greater than the current PE for the US Oil and Gas industry at 15.0x.

- Analysts expect the number of shares outstanding to decline by 4.42% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- A significant net loss attributed to asset impairments, particularly related to West Coast operations, could negatively impact future earnings and financial health.

- The renewable diesel segment struggled with high operating losses, reflecting challenges in maintaining profitability amidst shifting regulatory and market dynamics, thereby affecting net margins.

- With the intent to close the Benicia refinery due to stringent regulations, there could be substantial costs related to plant closure, negatively affecting cash flow and future earnings.

- Uncertainty around policy changes, such as potential increases to RIN obligations and California LCFS adjustments, introduces risk to revenue stability in the renewable segment.

- High operational cost pressures, particularly from maintenance and potential fluctuations in natural gas prices, may constrain margin improvements, thus impacting overall profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $256.26 for Valero Energy based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $300.0, and the most bearish reporting a price target of just $181.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $112.9 billion, earnings will come to $5.4 billion, and it would be trading on a PE ratio of 15.1x, assuming you use a discount rate of 7.1%.

- Given the current share price of $262.62, the analyst price target of $256.26 is 2.5% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Valero Energy?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.