Last Update 11 Jun 26

Fair value Increased 6.64%DRH: Elevated Lodging Sector Hype Will Pressure Future P/E Repricing

Analysts have nudged the DiamondRock Hospitality price target higher, with the updated fair value estimate moving from about $9.50 to roughly $10.13 per share. This change reflects recent upward revisions to Street targets around stronger year to date operating performance and refreshed lodging REIT models.

Analyst Commentary

Recent research points to a generally constructive stance on DiamondRock Hospitality, with several firms lifting their price targets following year to date operating updates and refreshed lodging REIT models. At the high end of the published figures, one firm set a US$12.25 target, while others referenced US$12 and US$11.25 levels, alongside Hold, Equal Weight, and Buy ratings.

Even with these higher targets, research notes highlight that much of the discussion still centers on valuation discipline and how current trading levels compare with the underlying earnings stream. In particular, the lodging sector's recent relative performance is described as moving too far, too fast versus fundamentals, which introduces a more cautious tone around how much upside may remain if earnings do not keep pace.

Across the updates, analysts also anchor their views to recent model adjustments following Q1 results and broader sector work on lodging REITs. For readers, the key takeaway is that while price targets cited in the research are higher than previous levels, the commentary still weighs execution risks and sector level positioning rather than treating the recent strength as an all clear.

Bearish Takeaways

- Bearish analysts describe the lodging sector's recent relative outperformance as moving too far, too fast versus the earnings stream, which can limit upside if fundamentals do not catch up.

- Equal Weight and Hold ratings alongside higher targets suggest some bearish analysts see valuation as full, with less conviction that the stock can significantly outperform sector peers.

- Cautious commentary links revised targets to model updates after Q1 results, signaling that part of the move reflects housekeeping in forecasts rather than a clear shift in long term growth expectations.

- References to being incrementally cautious on valuation flag the risk that any slowdown in operating trends or execution missteps could lead to renewed pressure on the stock's multiple.

What's in the News

- The Board of Directors authorized a share repurchase plan on April 28, 2026, according to company disclosures.

- The company announced a share repurchase program of up to US$300 million, indicating capacity for ongoing buybacks. Source: Buyback Transaction Announcements.

- From January 1, 2026 to April 28, 2026, the company repurchased 136,364 shares for US$1.28 million, completing a total of 8,049,182 shares bought back for US$64.35 million under the August 1, 2024 authorization. Source: Buyback Tranche Update.

- Management issued full-year 2026 earnings guidance and stated an expected net income range of US$103.2 million to US$116.2 million. Source: Corporate Guidance.

- A subsequent guidance update for full-year 2026 indicated an expected net income range of US$106.85 million to US$119.85 million. Source: Corporate Guidance.

Valuation Changes

- Fair Value: The model fair value estimate increased from $9.50 to about $10.13 per share, a shift of roughly 6.7%.

- Discount Rate: The required return assumption rose slightly from 8.07% to about 8.32%.

- Revenue Growth: The long-term revenue growth input moved modestly from roughly 2.08% to about 2.15%.

- Net Profit Margin: The assumed net margin increased from about 10.77% to roughly 11.20%.

- Future P/E: The forward P/E multiple used in the model rose from about 18.30x to roughly 19.48x.

Key Takeaways

- Reliance on leisure and resort markets heightens vulnerability to economic shocks, discretionary spending slowdowns, and competitive threats from short-term rental platforms.

- Rising labor costs, renovation needs, and supply chain risks pressure operating margins and limit financial flexibility for investments or dividends.

- Strategic reinvestment in high-barrier urban properties, supported by strong demand and disciplined capital allocation, positions the company for sustained profitability and long-term shareholder value.

Catalysts

About DiamondRock Hospitality- A self-advised real estate investment trust (REIT) that is an owner of a leading portfolio of geographically diversified hotels concentrated in leisure destinations and top gateway markets.

- The acceleration of remote and hybrid work models continues to weaken business travel growth, creating persistent risk to DiamondRock’s future occupancy rates and revenue, particularly as first-quarter business transient demand improvement is unlikely to offset this long-term structural decline.

- DiamondRock's substantial exposure to leisure-oriented and drive-to resort markets heightens vulnerability to downturns in discretionary spending and deepens exposure to economic shocks, threatening both revenue and EBITDA margin stability as macroeconomic anxiety persists and disposable incomes stagnate for the middle class.

- The company faces ongoing labor scarcity and rising wage pressures, with wage and benefit growth already tracking at three to three and a half percent for the year ahead, pressuring operating costs and compressing net margins even as DiamondRock’s ability to find additional cost reductions diminishes post-pandemic.

- Competition from short-term rental platforms like Airbnb and VRBO continues to draw away both leisure and group demand, leading to increased pricing pressure, lower average daily rates, and eroding RevPAR growth for hotel REITs such as DiamondRock, directly impacting revenue and profitability.

- The ongoing necessity to renovate and reposition aging properties, compounded by supply chain risks and potential tariff hikes on imported furnishings, threatens to inflate capital expenditures and asset maintenance costs, thereby constraining free cash flow available for dividends or reinvestment and increasing risk of future asset write-downs.

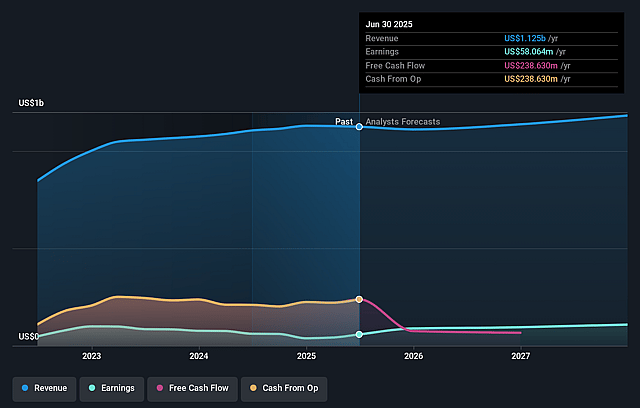

DiamondRock Hospitality Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on DiamondRock Hospitality compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming DiamondRock Hospitality's revenue will grow by 2.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 8.6% today to 11.2% in 3 years time.

- The bearish analysts expect earnings to reach $134.2 million (and earnings per share of $0.58) by about June 2029, up from $96.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 19.5x on those 2029 earnings, down from 24.6x today. This future PE is lower than the current PE for the US Hotel and Resort REITs industry at 25.5x.

- The bearish analysts expect the number of shares outstanding to decline by 0.23% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.32%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Sustained RevPAR growth in the urban portfolio, highlighted by a 5% year-over-year increase and steady improvements in group and transient business demand, suggests underlying revenue momentum that could buoy long-term revenues and profitability.

- Successful property renovations and repositioning, as seen with the Westin San Diego Bayview and Bourbon Orleans, are generating substantial post-renovation lifts in RevPAR and net operating income, indicating that capital reinvestment may continue to drive earnings and margin expansion.

- The company’s focus on high-barrier-to-entry urban and resort markets with minimal competitive supply growth provides long-term protection against oversupply, supporting room rates, occupancy, and net cash flow stability in future periods.

- Active and accretive share repurchases, along with disciplined capital recycling and a flexible balance sheet, enhance per-share earnings and return on equity, which could underpin share price appreciation and investor returns.

- Resilient leisure and group demand, supported by broader secular travel trends and a diversified portfolio strategy, positions DiamondRock to benefit from ongoing growth in domestic travel and consumer experience spending, aiding sustained revenue and adjusted EBITDA growth over time.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for DiamondRock Hospitality is $10.13, which represents up to two standard deviations below the consensus price target of $11.87. This valuation is based on what can be assumed as the expectations of DiamondRock Hospitality's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $13.0, and the most bearish reporting a price target of just $9.6.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $1.2 billion, earnings will come to $134.2 million, and it would be trading on a PE ratio of 19.5x, assuming you use a discount rate of 8.3%.

- Given the current share price of $11.64, the analyst price target of $10.13 is 14.9% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on DiamondRock Hospitality?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.